Mortgage advisor Jeff Kerwin has always been a big fan of the Government’s First Home Loan scheme. Kerwin is chief executive of Nest Home Loans, the biggest mortgage lender in the Waikato. And, as he says, what’s not to love about a Government-backed scheme offering first home buyers mortgages on a five percent deposit.

As house prices continue their crazy ride upwards, the biggest obstacle for many of his clients is finding the 10 to 20 percent deposit a commercial bank is going to ask for, Kerwin says. You’re talking $75,000-$150,000 on a bog standard ($750,000) Hamilton home.

A lot of people can service a loan that big, Kerwin and other mortgage advisors say. Young professionals a few years out of university, families with two income-earners, people back from overseas. But many just don’t have big savings. If you don’t have the bank of Mum and Dad (or Granny or Uncle Walter), you haven’t got a hope.

Which is what the 5 percent deposit First Home Loan – originally called the Welcome Home Loan and offering a 10 percent deposit – was set up for.

Not only does Kāinga Ora offer low deposits, it also allows borrowers to use gifted money (Mum and Dad/Granny/Uncle Walter) for that 5 percent deposit, when commercial banks expect at least 5 percent of so-called “real savings”. And because the loans are guaranteed by the Government, First Home Loans are excluded from the Reserve Bank’s restrictions on low-deposit lending – meaning banks in the scheme are confident to lend without getting themselves offside with RBNZ.

In the past, hundreds of Nest clients have been approved for a First Home Loan, Kerwin says.

Not any more. Over the past few months as house prices have continued to rise, the $500,000 price limit for a home to qualify under the FHL scheme has basically shut out all but the scummiest do-ups in Hamilton.

Oh, but of course do-ups don’t qualify either. Any house with a building report showing more than $5000 of remedial work needed, is automatically ineligible. Too risky for first home buyers.

No matter you might be a DIY expert, and that do-ups are a Kiwi tradition.

It’s not just Hamilton; it’s the same in New Zealand’s other sought after property markets. Auckland, Wellington, Napier, Queenstown, Tauranga.

In cities where apartments tend to be a big part of the more affordable end of the housing market, there’s another problem. Kāinga Ora is even more risk averse than the commercial banks when it comes to lending on apartments, mortgage brokers say. Particularly small (read cheaper) apartments. See Newsroom’s stories on this other crazy Catch 22 for first home buyers.

And as prices increase, it’s getting worse.

Nest has seen just a handful of the loans approved in the past year – almost nothing since January.

Same with other mortgage advisors. Janet Harris at Auckland’s Point Home Loans can hardly remember when she last got a First Home Loan through.

Rod Schubert, who worked as a mortgage manager at Kiwibank for eight years before starting his own financial advice business, based in Auckland and Queenstown, says he and his colleagues used to process a lot of First Home Loans. They were unwieldy and bureaucratic, with customers having to provide way more information than with a commercial bank loan.

But they got people into homes.

Now the price caps make First Home Loans “irrelevant”, Schubert says.

Invercargill-based SBS Bank has traditionally handled the lion’s share of the First Home Loans – 40-50 percent. Its customers were largely outside the big centres – small-town South Island, rural Hawkes Bay; places not too badly affected by the house price spikes.

SBS hasn’t seen its FHL loan business decline, says Mark McLean – general manager member experience. But as demand has disappeared from the big centres because of the price caps, SBS’s rural and small centre loans are making up a bigger percentage of the total.

McLean says the Kāinga Ora scheme can work if the price cap at least matches or beats the “lower quartile” house price, the cost of the bottom 25 percent of houses on the market.

But that’s increasingly rare in all but the least sought-after places.

“There is a strong need for this product – it really helps first home buyers. But in many regions, the caps are making it redundant.”

– Mark McLean, SBS

“In Christchurch, the cap is $500,000 and the lower quartile price is $425,000. There, the product works well. We are seeing good demand and good growth.

“But in other regions, even houses in the lower quartile aren’t going to fit under the Kāinga Ora price.”

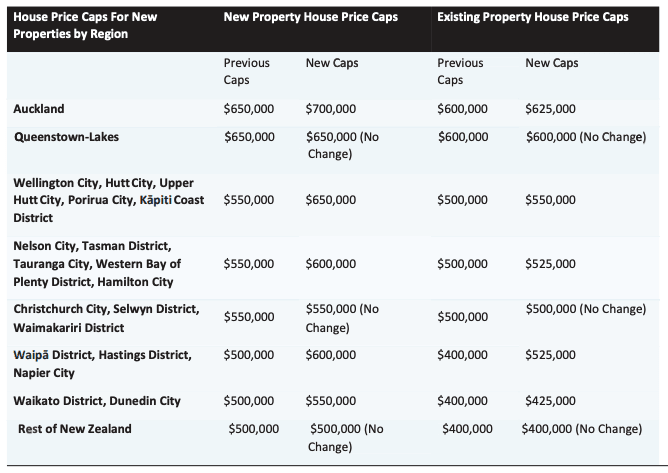

In Queenstown, for example, the cap is $600,000 and the lower quartile price is $820,000. That’s a crazy gap. In Hamilton, the lower quartile price is $563,000, the cap $525,000. In Dunedin, the cap is $425,000, the lower quartile price $460,000.

“There is a strong need for this product – it really helps first home buyers who struggle to save the deposit for a home. But in many regions, the caps are making it redundant,” McLean says.

“We lobbied Kāinga Ora and we were disappointed with the level of increase to the cap we saw in the most recent review.”

Kāinga Ora argues it only administers the first home loans – and its sister product, the first home grant. “The price and income caps and settings are signed off by Cabinet based on advice from the Ministry of Housing and Urban Development,” says a spokesperson. “For accuracy, that’s an important distinction.”

Maybe for Kāinga Ora. Not for wannabe first home buyers.

Prime Minister Jacinda Ardern did announce as part of her recent housing package that she was lifting the house price cap “to assist more New Zealanders to purchase a first home”.

“Paltry”, Kerwin says. Next to useless.

“The flagship tool they boast is the saviour to first home buyers, is completely redundant.”

Jeff Kerwin

He has crunched some numbers.

Five years ago the median house price in Hamilton was $500,000, the same as the price cap. The April 1 increases took the cap from $500,000 to $525,000 for Hamilton. That’s at a time when the median house price in the city is $750,000.

The cap has gone up 5 percent after a period when house prices have gone up 50 percent.

“What good is that to anyone?” Kerwin says. “The flagship tool they boast is the saviour to first home buyers, is completely redundant.”

Matt Taylor is co-founder and CEO of First Home Coach, an app-based tool helping potential first home buyers understand the housing market and where they are at on their journey.

“If we benchmarked the Auckland house price cap on median house price growth, we should have seen the cap increase to $850,000 for existing homes,” Taylor says. Instead it went to $700,000.

“And that’s not even taking into account where the market might move in the next 6-12 months, before first home buyers have a chance to use the Kāinga Ora products.”

The original Government target for the Welcome Home Loans was 5000 a year. Five thousand first home buyers being helped into a new home. Last year, 1170 loans were approved, according to Kāinga Ora; the year before it was 1050.

That’s a 33 percent drop from the 1577 loans given out in 2018, and a massive shortfall from the original 5000 target.

Same with First Home Grants (formerly the KiwiSaver HomeStart Grant), a sister Kāinga Ora product which allows first home buyers who have been making KiwiSaver contributions for 3-5 years to get up to $10,000 (for a single person, $20,000 for a couple) from the Government to help towards a deposit – if they (and more importantly the house they are buying) meet the criteria.

In 2014, then Housing Minister Nick Smith set targets for the First Home Grants of 20,000 a year, but the Kāinga Ora 2019-2020 annual report shows only 14,000 were given out in the year to June 2020. The agency told Newsroom that figure was 51,000 for the three years 2018-2020. The spokesperson denied there were any targets.

However, the number of grants is dropping.

It will fall further unless the Government boosts the cap to something more realistic, like $850,000 in Auckland, Taylor says.

The Government isn’t missing those original targets through lack of need in the market, he says.

“People are missing out because the eligibility criteria are so restrictive. It’s not even keeping pace with the market.”

He estimates boosting the cap would help an additional 8500 first home buyers onto the property ladder this year – and allow the Government to give out 20,000 grants “for potentially the first time ever”.

He reckons it would cost just $28 million more a year.

“It is expected the April 1 changes to the First Home Products will help increase the uptake of the scheme and support even more New Zealanders into homeownership,” a Kāinga Ora spokesperson told Newsroom, although he did not provide any evidence why that would be the case.

Kiwibank’s head of borrowing and saving Chris Greig is also positive about the loan scheme

Kiwibank has been involved in the scheme since its inception in 2003 and Greig says 17 percent of the bank’s first home buyer customers over the past 12 months have been part of the programme. That’s down from almost 30 percent in 2016, but up from 13 percent in 2018, after the Government reduced the deposit level from 10 to 5 percent in October 2019.

Greig is supportive of the most recent house price cap increases.

“It’s moving in the right direction.”

He also thinks the Government is right to put limits on the number of people eligible for a First Home Loan in such a hot market.

“Our role is making sure people can pay back their loans. Responsible lending is very important. It’s not just about handing out money. It’s about making sure customers can afford to service them.”

Matt Taylor doesn’t agree. With rents so high, many people aren’t paying much more in loan repayments than they are in rent; some would pay less – if they could afford the deposit on a house.

And that’s where both parts of the Kāinga Ora scheme – loans and grants – come into play. The majority of first home buyers using the First Home Coach app struggle with the deposit. They need both a low deposit rate for their loans, and additional cash to get to the magic deposit number.

“You need the best part of $130,000-$150,000 to get a 20 percent deposit on a lower quartile home in Auckland, and the average for the couples using the First Home Coach app is $50,000,” Taylor says. “For a single buyer it’s $38,000.

“And even that represents a lot of savings. There’s a lot of graft behind these numbers.”

Take Hamilton couple Jenny and Paul*. They are in their 30s, with two children; they both have reasonable salaries. But rent of $500 a week and the normal expenses of a family means they haven’t been able to save much.

They tried for a FHL in early 2020, but were turned down. Jeff Kerwin, their mortgage adviser, says Kāinga Ora needed letters from their employers to say their jobs were stable, but with Covid-19 picking up, few bosses were going to give that assurance.

“Incorrect,” says the Kāinga Ora spokesperson. “Kāinga Ora has never had such a requirement. This may have been a bank’s requirement.

“First Home Loan applications are made to participating lenders (not Kāinga Ora). Lenders assess those applications, and will only submit applications to Kāinga Ora if the lenders believe the application fulfils all criteria.”

No so, says Kerwin. “The banks apply their standard criteria whether it’s a standard loan or a First Home Loan. For a FHL, Kāinga Ora adds another layer of criteria on top of the bank standard criteria – a whole new set of hurdles into the process.

“It’s Kāinga Ora that is making the FHL more difficult, not the banks.”

Whichever it is, for Jenny and Paul, by the time things had settled down with the pandemic, house prices increases had taken away any hope of finding a place for the four of them under $500,000 – or even $525,000.

Jenny is in tears as she tells the story of looking further and further outside the city for a house that might cost less than the cap.

“Te Awamutu [half an hour’s drive from Hamilton, where they both work] was still at Hamilton prices. We would have had to go somewhere like Tokoroa or Te Aroha, that’s an hour away. It’s too far.”

Jenny and Paul don’t have the option of living with one of their parents to stash money away. There’s no Bank of Mum and Dad, which is how so many people get their deposits.

“It’s frustrating and heartbreaking,” Jenny says. “You do everything you can, but the caps are so unrealistic, there’s no way it’s going to happen. We’ve stopped looking.”

Time and again, Newsroom got the same story. Andrew, 34, talked about looking for a home with his wife and three-year-old daughter.

“I’ve been told there are a lot of people like me, with the money to service a mortgage, but without enough for a 10 percent deposit. But where am I going to find something in East Tamaki [Auckland] for less than $650,000?”

Or Sarah who finally had to borrow from a family member for a 20 percent deposit and get a mortgage through a commercial bank, after failing to find a property in Hamilton that would be safe enough for a single woman, within an hour of her work, and still under $500,000.

“I couldn’t even find anything to view.”

“It’s crazy,” says Rod Schubert. “Everyone wants first home buyers to get into a house, but it’s so hard to get a loan from Kāinga Ora. The paperwork is intense, apartments are off the table, and anything with $5000-worth of deferred maintenance.

The Government is always saying it wants to help, but it isn’t looking into this hard enough. It’s not talking to people at the coalface – people that can see what’s going on.”

* Not their real names

Following publication, Newsroom received this heart-warming story from a couple living on the West Coast of the South Island, where house prices are still low enough for it to be possible to get a place under the Government price cap. It shows the scheme working as it was intended.

“My husband and I and our two children have just moved into our brand new home in Westport.

“We received both the first home grant and had our loan granted through Kāinga Ora’s low deposit scheme.

“We only have one income (fairly average paying job) and had a very minor deposit (as well as some KiwiSaver). However we somehow managed to quite easily purchase a brand-new three bedroom, two bathroom family home here in Westport, only because of these schemes that were in place.

“Brand new homes for the price of 330,000 aren’t something you come by every day here and the market has picked up dramatically as of recent, so we are definitely the minority. However I do think in some areas of New Zealand there is huge opportunity for poeple like ourselves to utilize the opportunity presented.

“We feel extremely privileged and lucky to have had the chance to buy our first home and we really hope others who maybe don’t know about these schemes or opportunities to get the same outcome as we have.”

Are you a first home buyer trying to get into a home? Have you had any experience – good or bad – with a Kāinga Ora’s First Home Loan or Grant? Newsroom is keen to hear from you. Email nikki.mandow@newsroom.co.nz