By Rodney Dickens*

The bank economists are competing to predict the largest Official Cash Rate (OCR) hikes without any consideration of the implications.

You don’t have to go back too far and the economists at the banks were predicting that inflation wouldn’t be a problem and interest rates would stay low for many years. And some were predicting the OCR would go negative. Having been wrong on these fronts they have done huge about faces. They are now running around like headless chooks because of the inflation they didn’t see coming, even aside from that related to Covid-19 and Russia’s invasion of Ukraine.

They are calling for even larger OCR hikes, as the ANZ and ASB economists did this week.

Aside from the evidence presented below that points to the increase in interest rates so far being more than is required to cool inflation, sane thinking about the scale of the increase in mortgage interest rates so far should be enough to caution against charging ahead with an even larger hike next month.

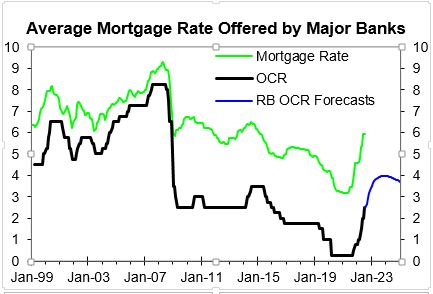

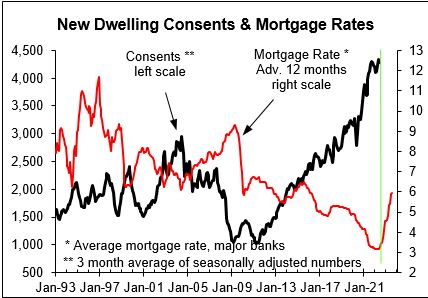

The green line in the chart below is the average of the various floating and fixed mortgage rates offered by the major four banks. It tends to front-run the OCR a bit. If the Reserve Bank hikes the OCR as it predicted in the May Monetary Policy Statement, the average mortgage rate could peak around 7%.

To put the increase in the average mortgage rate in perspective, during the Reserve Bank’s last battle with inflation from 2004 to 2008, it increased from a low of 6.1% in June 2003 to a peak of 9.3% in April 2008, a 3.2 percentage point increase in just under five years.

In the last 16 months the average rate has increased from a low of 3.2% to 5.9% currently, an increase of 2.7 percentage points. If the average rate increased to 7% it would be a 3.8 percentage point rise. But the increase this time around is dramatically larger than it seems from these numbers.

The starting point for the latest battle against inflation is dramatically lower at 3.2% versus 6.1% in 2003. In terms of interest costs faced by borrowers there has already been an 84% increase based on the average mortgage rate in just 16 months versus a 47% rise in almost five years during the last inflation battle. And if the average rate were to rise to 7%, it would be a 119% increase in mortgage interest costs.

In an extremely short period interest costs have risen dramatically more already than was needed to cool inflation last time. Considering this and it taking up to two years for changes in interest rates to impact on inflation, sound judgement points to a need to wait to see what impact the largest increase in interest costs on record will have rather than charge ahead with even more aggressive OCR hikes.

I cannot see any flaw in this logic, but it escapes the economists and is likely to escape the Reserve Bank until it sees the scale of the damage being done. A scale that is likely to fuel a market-led fall in interest rates.

The Reserve Bank and bank economists are way off the mark in assessing the fallout from the OCR hikes delivered already.

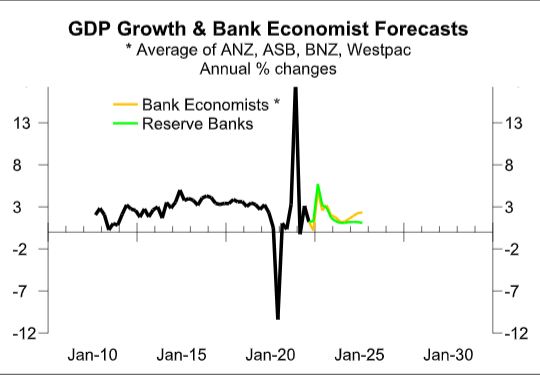

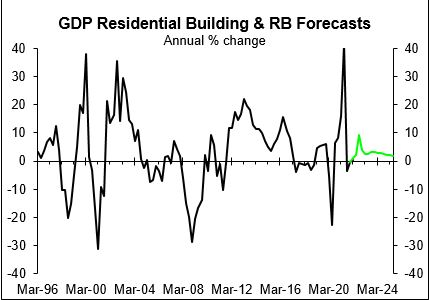

The first chart below shows what the Reserve Bank and four main bank economists predict for economic growth. The second chart shows what the Reserve Bank predicts for growth in residential building activity based on the GDP component. Residential building is important because it plays a pivotal role in economic growth. The bank economists’ forecasts are based on their latest forecasts as surveyed today and the Reserve Bank’s are from its May Monetary Policy Statement.

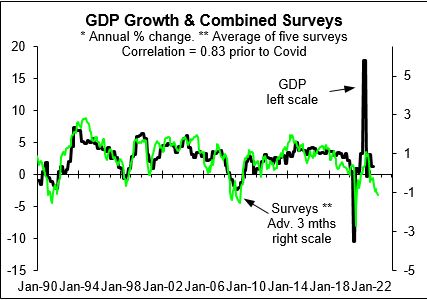

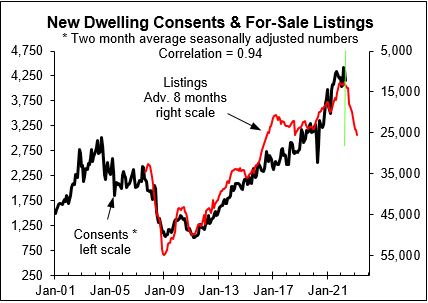

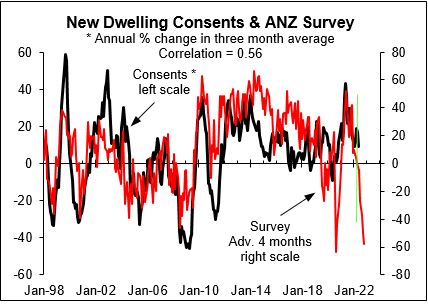

None of the bank economists predict anything close to a recession and the Reserve Bank predicts moderate growth in residential building activity despite it being highly sensitive to interest rates. By contrast, the first chart below shows a combined business and consumer survey that predicts an imminent recession or fall in GDP, and the second and third charts show leading indicators of new dwelling consents that predict an imminent and large fall.

It should be no wonder a large fall in residential building activity is coming considering interest rates are the major driver of new dwelling consents and take around 12 months to impact.

Just as the major fall in interest rates from 2019 to 2021 was the main driver of the huge increase in new dwelling consents since 2019, it should be no surprise the leading indicators point to a major fall in consents in response to the dramatic increase in interest rates in the last 16 months.

This is not rocket science, it is basic analysis the Reserve Bank and bank economists should do as a basis for their views on interest rates and more. For reasons I do not understand they have yet again failed to do such analysis or if they have done it, they have ignored it. The outlook for GDP growth is dramatically worse than the Reserve Bank and bank economists predict, as should be no surprise given the scale of the increase in interest rates so far. While the outlook for residential building is dramatically worse than the Reserve Bank predicts.

*Rodney Dickens runs Strategic Risk Analysis. His roles prior to that include Group Strategist and Head of Research at ASB, and roles at the Reserve Bank including being a member of the Monetary Policy Committee.

166 Comments

Great analysis. The spending or intent to spend pullback is well underway. The existing property bubble is popped and (per today's NZH article) new build sales are down 80%. People are now in survival mode. Increasing the OCR aggressively just because our stats are so slow to come through that the RBNZ still thinks the economy is overheating doesn't make sense.

My Japanese colleague said that early research there is showing the new variants impact the lungs more. Not as much as alpha and delta, but it's still serious. I think the "big sick" could roll on for the rest of the year.

Yes, great analysis, at long last. Thank you Rodney, I am glad you are finally commenting here. What you said has been on my mind for a long time. I am glad it has finally been put into an article, and with much more data support and depth than I could have ever come up with.

I do hope economic collapse in NZ can still be avoided at this point, by lowering the official cash rate or at the very least by keeping it stable. This should be in the interest of every New Zealander!

I've said this before, but the presence of Covid is actually inflationary, not deflationary. It means you need more inputs (workers, health and safety protocol) for the same level of output. It also contributes to labour shortages. Or maybe it would be more accurate to say stagflationary.

Give everyone who wants one the option of a fixed mortgage on 3% for the remainder of their term. Our problem in NZ (and Aus, UK etc) is that matching US Fed changes in interest rates has a much quicker and bigger impact on disposable incomes because mortgage payments go up quickly. In the US the vast majority of people are on 30-year fixed rate mortgages, so interest rate hikes only really impact people who are about to buy (which is why their house building industry gets hit hardest first)..

The RBNZ's targets include the employment rate. This, of course, is driven by the overall shape of the economy, for which building completion is an early indicator.

In contrast, interest rate raises take several months to take full effect. This is because fixed mortgage agreements roll over into maturity in a staggered way.

The RBNZ tends to oversteer heavily, both on the way down when they were lowering interest rates, and now with too fast and too sharp rate increases. Our economy is like a huge aircraft. Ask a pilot what can happen if you pull up too sharply - it is called stall. A stall can be followed by a crash, leading to disaster.

In contrast, interest rate raises take several months to take full effect.

Rodney states in the article that they take 12 months to take effect. 12 months ago the OCR was 0.25% so the effects we are feeling today must be as a result of that, right? Hmm, why are we crying about dwelling completions right now then? If it isn't related to the most acommodative monetary policy we've ever seen, could it possibly be because of something else?

Mortgage rate increases start impacting straight away as fixed term rates expire - with the impact growing as more fixed terms expire. Last month bank yields on residential loans notched up to 3.36% from 3.21% the month before. That's an extra million dollars a month in interest paid by mortgagors. The data is here - you can see the escalating impact very clearly... https://www.rbnz.govt.nz/statistics/series/exchange-and-interest-rates/…

Yes. I don't get people who complain about the potential correction from moving back to more normalised settings.

It's not rocket science, just take a look at basic sp500 and money supply charts. It needs to correct and it will without any major social disruption (job losses etc) as the gains were just candy fluff to start off with.

The rates were way to low enabling huge amount of people to borrow ridiculous amounts of money buying properties at over valued prices now rates have just started to rise the cost of borrowing so much is going to put a lot of pressure on the people who purchased property over last few years some have already seen deposit disappear and will soon be in negative equity the banks should of testing these people’s financial positions so hopefully will be able to keep up payments. Many people were fooled into believing house prices can only go up borrow as much as you can rates will stay low forever unfortunately this is just a fairytale and the people who pushed this narrative sold quickly end of last year and now sit on cash waiting to buy after crash is complete, don’t be fooled again rates are going up because someone has to pay and it’s going to be all the people holding the property bought over last few years.

House prices weren't included in the CPI inflation calculation for the years prior to this year. If they were, inflation would have come out higher than near zero as it was. You could argue that this a driver that caused the rbnz to lower the OCR a bit too low as it allowed people to pour too much wealth into houses without consequence.

So in the interest of stability house prices must remain excluded until inflation is bought under control.

Bolger and Shipley removed the cost of land, the cost of existing houses, and the cost of servicing a mortgage from the CPI in the 90s.

The housing components left in the CPI are the cost of a new build and the cost of renting.

About 5 years ago these made up 4% and 9% of the weightings, so 13% in total which means the cost of accommodation has been way understated for 30 years which means CPI is understated, measured inflation lower than reality, interest rates lower than they should be, so house prices can rise exponentially without a corresponding increase in interest rates.

So house price increases and M3 money supply doubling every 10 years are a policy decision. That is why we face a crisis now.

In addition, blue collar wage increases are generally tied to CPI. So real wages have been going backwards for 30 years.

The housing component of the CPI is now around 20%, as the cost of a new build and rent has increased so much.

The question is when will that component be reduced or removed so house prices can boom again.

Alas house mouse you have a point! It looks like our monetary policy has contradictory objectives? In that to satisfy the CPI mandate you have to ignore the employment and vice versa. Don't know how our quixote reserve bank governor Mr Orr will get him self out of this one? Maybe he will start using astrology to decide on CPI movements....this would probably be an improvement to be fair.

And financial stability, I grant you, but still not the housing market per se. The conclusion may be right (that the RBNZ is going to overshoot), but I don't agree that the current analysis shows that conclusively in any way. Yes construction is a major sector, and a downturn there is in some ways indicative, but it's only one sector. Yes the surveys are dire, but so have they been many times in the last two years. And I certainly don't agree that the tightening cycle just before the GFC is a good guide to the current one.

The RBNZ need to have inflation between 1-3% over the medium to long term. But that doesn't mean they should yank the OCR lever all over the place depending on what the 3 month old CPI data says.

I think the point is that in Rodney's eyes (and mine too) it is likely that inflation will come down soon. If the RBNZ keeps increasing the OCR they may cause a recession. Sure its not really in their remit to not cause a recession (although I suspect that is why full employment was added to the remit), but if they did unnecessarily cause a recession because they slammed on the brakes way too hard its not exactly a gold star on their CV.

At the moment their foot is so hard on the brake they have almost pushed the pedal through the floor, and they want to push it even harder because their speedo is still showing the speed from April.

Financial stability is the RBNZ's first remit, pretty sure, and considering the epic overvaluing of the retail property market, the size our debt linked to that market, and that employment (which is the only tent leg still standing) looks good for the same reasons as the leaning tower or pizza, I think this article is somewhat off kilter.

On top of the aforementioned you have,

- The strengthening USD (now on par with Euro)

- The energy crisis looming in Europe (driving up imports further, among other stuff)

- The looming fertilizer/food crisis (Russia is near the most important supplier for fertilizer and wheat)

- The Chinese are BEGINNING QE ($220 bil just to start) while the world is trying QT

- The US FED has only JUST begun raising rates from near zero (and according to Atlanta FED has been in recession since Jan 2022)

- The US FED that was meant to started QT, actually adding to it's balance sheet again recently so technically still hasn't started

- The fact that the Chinese lockdown policy isn't going anywhere anytime soon

- The fact that Producer Prices indices (around the world) are still higher than CPI indices (ergo - even without rate hikes producer balance sheets are hurting, and yet to pass this cost on fully to consumers)

- And, and, and I'm meant to be working, and...

Then this article, much like everyone else over the last 2 years, is trying to say, "inflation be ok, gone go down, look at my excel spreadsheet of domestic variables", completely ignoring the catastrophic international scene, that while no one can guess the outcome, surely doesn't point to a normalisation in inflationary pressures any time soon.

Probably the worst bit is comparing this scenario to 2008 financial crisis, when this is not only a financial crisis, its an energy, food, health, geo-political crisis ASWELL as, doesn't take a genius to look back 100 years and consider what era was the more applicable to draw comparisons too.

If stability was defined by the content of the interest.co.nz comments then the world would be in complete turmoil 110% of the time.

It drains me how ridiculously over dramatic and downbeat many comments are here. So many seem to be drawn to the extreme negative outlook of the future. Completely unhinged as to how unlikely there outlooks are.

No, no one is saying that. That’s disingenuous.

What Rodney, and I, are saying is that the Rapid increase in interest rates is already starting to whack the economy, and demand, and the damage will increase without further OCR hikes.

There is clearly a lag between rising interest rates and demand destruction (and hence inflation quelling). The OCR rises over the last few months are starting to filter through and will continue to do so over the next 6 months, WITHOUT further OCR Hikes.

If the RBNZ keeps hiking over the balance of 2022, then those hikes will have lagging effects into mid 2023 - but by then the economy will be devastated and inflation will have fallen substantially, especially non-tradable inflation.

Anyway, I have said enough, most commenters on this website, with a few notable exceptions (JFoe, Te Kooti, Yvil, Independent Observer, JimboJones, and now Markus) don’t want to even TRY and contemplate this viewpoint. I am wasting my time.

Of course they lag, the question is are interest rates high enough now or not? Really no on actually knows you can make up graphs as much want. People will probably decide on what they think is hurting them the most, if they are scared they will not be able to pay their mortgage the will agree, if they want term deposit, or houses to fall more they won't.

HM, I don't thin you or Rodney are adequately considering the rapid devaluation of NZD against foreign currencies, such as USD. NZD/USD has declined >10% in 3 months.

This is also a major driver in the upward movement in rates. NZD/USD will not rebalance on its own as IMO USD is in a medium/long-term upward trend.

Of course, if we'd measured the inflation in houses and other assets properly, you'd understand interest rates have been far lower than they should have been for the last decade. The inflation has always been there - it was just ignored.

Suggesting that the increase is unjustified because it's a massive percentage increase from an absurdly low starting point is a fallacy.

The author has also conveniently omitted that the highest interest rate in his example period was ~3.9% p.a. - or just over half of the current rate.

It is indeed not rocket science. This reads as wishful thinking by someone who has "a unique advantage in helping clients profit from NZ economic and housing cycles" - a.k.a, makes their money from real estate speculation.

Yes but at the end of the day overly leveraged property investors have to get paid out on their bets. This will be done under the guise of protecting first home buyers. That is unfortunately how it works in this country. I think they will change the rules in the not to distant future.

Of course, such relief could easily be targeted at owner-occupiers, if the government dared; if they really wanted to up the ante and have a generational reset on property, but offer a FLP-style ZIRP product for owner-occupiers. Perhaps they could nuke the accommodation supplement to pay for it and let rents for a genuine equilibrium too.

Correct; rather than just bugger up the tax system, why not offer a chance for them to refinance at close to zero so they can get their unreasonable mortgages down faster, which are no longer underpinned by unreasonably priced assets? Perhaps, through, say a retail bank offering? Now if only the government had a bank they could use for such a purpose... perhaps even their own bank that they owned?

What a pity. Guess we'll just have to let them drown while investors cash out and make the problem even worse.

Good analysis on housing and construction economy, but I think we need to look into other aspects of our economy if we want to have a clear picture of how OCR goes in future, such as our exports. Yes, house and construction became one of our main industry, however, having booming house and construction industry right now won't solve our trade deficit issue at the moment, which is part of reason why we have a weak NZD, unless if we can export housing, but can we? GDP might fall or stay flat for a while, but that only bring us to stagflation, the inflation won't be gone for a while unless a severe recession happens. So RBNZ still see high inflation is the major threat to our economy, this won't change for a while.

Borders are coming back up and soon we will fire up the old factories that sell business diplomas to international students. Many of them go on to participate in the tourism sector, selling lattes for foreign dollars.

Let's all hope that the increased demand for imports from bringing more consumers into NZ can be offset with international tuition fees and tourism dollars.

It’s great to see an article from Rodney again after so long. This guy, in my opinion, is by far the best economist in the land. Far more in touch with on the ground realities.what he says totally aligns with what I have been saying for more than one year.

Both the RBNZ and bank economists have absolutely no clue. They are going to bring our economy to its knees.

+1 HM, he talks sense.

I just had a call from an organisation I'm involved with. Staff could absorb food and energy increases but rising interest rates have been a tipping point. They are getting pay rises, or leaving (several to Govt agencies ironically). Higher interest rates supress demand, but this is not demand led inflation - it's supply side including chain/Ukraine/border closures. Higher interest rates are going to magnify the inflation spike then we get the recession.

I notice Rodneys message is increasingly being heard in Australia as well. The current situation is unique and requires switched on central bankers, so I'm pretty gloomy on our prospects.

But the timeline doesn't make sense. Borders closed April 2020, yet inflation only took off late 2021, in fact when borders started to open up. Then it was February 2022 when Russia invaded Ukraine, but inflation was already well under way. Besides, supply and demand are opposite sides of the same coin - if supply is restricted, you do want to suppress demand to keep the balance.

You could say the central banks have been very slow in raising rates for this very reason, suspecting the economic downturn would in itself bring down inflation. But it's been nearly a year and I suspect the banks realise this isn't working. Inflation is creeping away from them.

I'm going to call a spade a spade.

What is going to bring this country to its collective knees is years of taking ever-increasing debt to swap houses amongst each other. If we hadn't been so stupid, the interest rate rises would not be the death knell to our economy that it looks to be.

Barring bankruptcies, all that debt will have to be paid eventually (or infinitely transferred into the future - but that depends on future generations being willing to pay it - hence why the FHBs I know are now sitting on their cash).

Sadly, many of those who will be affected by the fallout from this stupidity will have had no hand in its creation.

But the interest rate rises themselves are not the primary cause of this problem - and blaming the RBNZ because people made 'rational/irrational' (take your pick) but ultimately stupid financial decisions is just using it as a scapegoat for our own sins.

Assuming you are correct, the way to have dealt with house prices was via legislation and not Monetary Policy. Blame tax-free gains, blame no land tax, blame the lack of stamp duty. We actively encouraged investment in housing and are now punishing the wider community.

I agree. But saying the rapid reduction of the OCR was the wrong call does not also mean that raising the OCR aggressively isn’t the wrong call. In my opinion, it is the wrong call, as regular readers will well know :)

So no surprise that I think what Rodney is saying is spot on.

Why? If we are not happy with Rampent asset inflation, this is just next step, a required correction.

The weak will fail, strong business and households with cash reserves will survive and take advantage of the next phase.

Unless what we are after is growth for growths sake.

You are missing an important part of the equation - unemployment. At record lows of 3.2% we are getting massive wage inflation. Although they won't say it, unemployment needs to move back to the mid 4%'s before the heat comes out of the labour market. Basically we need to take a painful unemployment pill to help kill persistent built in inflation. Of course house price decreases help massively but the key thing is unemployment, until we get that, interest rates will keep going north.

Yes and as I have said elsewhere also architects, planners, engineers, RE agents etc.

a lot of employment is directly reliant on the health of the residential construction sector.

My pick is unemployment above 5% by early 2023. And above 6% by May 2023.

And Migration to Aus won’t offer much relief, as their economy is also in strife. In fact we might see quite a few kiwis returning to receive the dole here. Their residential construction sector is also facing massive headwinds.

"And Migration to Aus won’t offer much relief, as their economy is also in strife. In fact we might see quite a few kiwis returning to receive the dole here. "

In the short term yes, but expect the Chinese to come to the rescue again as the CCP panics in the face of the realisation that they are truly in the shit with all the problems that are coming home to roost now - which are being met with the traditional CCP response of, wait for it, more and massive, brainless infrastructural spending ! Yes indeed! Accelerate The North South Water Project, more high speed train lines with no prospect of never being able to pay for themselves. Look for rapid growth in the White Elephant population.

To whit, a recent paper by an upper level party policy organ proposes swallowing crow (losing face !) and resume importing Aussie coal. And of course, the massive new infrastructural spending will require more steel, coal etc., irrespective of the fact that they are just digging themselves deeper into the mire along term. But hey ! with the party congress in November hovering in the background, bank runs and mortgage payment revolts etc. in the critical real estate market right now who gives a . This of course coupled with the prospect of the long festering and bitter Xi - Jiang feud threatening to break out into the open. All in all, The Lucky Country, if not exactly bouncing back should survive the currently developing credit crunch and economic downturn. She'll be right mate.

I argue the NZD is tanking BECAUSE of our steep OCR raises, which spells big trouble for our overindebted and housing-dependent economy. The currency markets can see recession/depression coming in NZ, and it is being priced in - effectively, they are 'writing off' our country as they can see things looming which many here cannot seem to see.

2020 buyers ruined? I bought late 2019, so nearly 2020, I don't consider myself ruined. We bought a 3 bedroom townhouse for 750K, at the peak of the frenzy last year it probably reached a value of a nudge over $1 mill. It's probably down to around 850K now. Yeah it might fall back to the purchase price of 750K by middle of next year, but that doesn't really bother me. It's not like we loaded up and bought lots of goodies on the back of that surge in equity.

I think it's some people who bought from early / mid 2021 who might face some challenges.

Well he said 2020, which could mean early 2020.

I think most people who bought in 2020 will generally be Ok, it’s more those who bought in 2021 who could be in strife.

People who bought in 2020 might only be in real strife if prices fall by more than 30%, which I think is quite unlikely.

2020 buyers ruined? I bought late 2019, so nearly 2020, I don't consider myself ruined.

I said "stressed or ruined", not just ruined. Obviously it was a generalisation - not every single buyer will be stressed or ruined. If HouseMouse is fine then I guess that's all good. As GV 27 noted, there's big difference between 2019 and much of 2020.

Many people think there's still a long way to the bottom so it might be too early to call yourself safe. Mostly my views are similar to yours - interest rates topping out soon, dropping again mid/late next year, house price recovery to follow in 2024. But the size and velocity of interest rate rises surprised me so I have to at least consider that there may be much more pain to come.

It’s not about me being fine and stuff everyone else. My point is I bought late 2019, those who also bought through much of 2020 should also be Ok for similar reasons, especially if they bought first half of 2020.

prices increased, what, 30-35% in 2021? That’s a fairly decent buffer for people bought in 2020 or earlier. Prices need to fall what circa 23-25% for that gain to evaporate. And given most people put down deposits of 10% of more, there’s still a bit more buffer before negative equity is reached.

certainly a significant number of people will be stressed by higher mortgage payments with increased interest rates.

I think we overestimate the ability of the RBNZ to control NZD value, excepting very drastic actions on their end.

The USD fluctuates as a kind of barometer of risk sentiment, with the NZD almost mechanically on the other end of the trade.

Sentiment has been poor, so the NZD has been weak.

That said, if the Fed raised rates substantially and we didn't, it would still weaken the NZD.

Agreed, also Keithwoodfordhad made some great comments about NZD value, our export, import and external current account deficit this morning, worth a read in my opinion.

Breakfast briefing; China's households prepare for tough times | interest.co.nz

The OCR rises to date have not even eradicated the wealth effect in housing that the effervescent cheap money enabled since Covid. Are we to believe that the RBNZ have a strategy so nuanced as to bring inflation back into target territory without contracting the economy. The whole point is to make us feel poorer, so we spend less and demand drops or am I missing something.

Let’s keep taking the easy options… and put off the hard. That’s what this article says.

Best way to eat a shit burger is fast..not nibble on it for hours

oh but think of the developers who paid $1.5m for a site in the arse end of papakura

yeah and wanted the customer to pay $950k for the finished build and be mortgaged for life, and hear every argument from his five neighbours five meters away…and every flush of the loo

Classic boomer economist!

The OCR being low has just enabled people to borrow huge amounts from banks just pushing house prices to a place where most of population can not purchase a property on annual income. If you are one of the people who thought rates would never go back up you really don’t understand finance. The RBNZ is just following FED so get used to higher rates because no way will they be at emergency levels again as the USD will lose its status as reserve currency.

Following the FED? Our economy is quite different from that of the U.S. In fact, we don't have much of an economy here, apart from property. This is a big problem for us.

Bretton Woods should be dissolved. The NZD should not be pegged to the USD. The FED is privately owned. What gives the FED the right to determine monetary supply for the entire world, issued with interest cost attached?

When inflation impacts then the ocr and thus mortgage rates will rise (perhaps a lot lot higher than now).

Its not just a local decision by rbnz either.. if the ocr is raised by the us fed we have follow suit.. to stop investment money leaving nz and damaging exchange rates causing more inflation.

This potential high rise in mortgage rates is the ever present risk associated with housing investment and one that individuals all take. Personally we chose not to invest in more properties because of it, so have little sympathy for those affected.

House prices rise and fall. Interest rates do the same. Its always been that way and the responsibility of the purchaser and their advisors to manage their individual risk. Black swan events like (but different in naturebto) ukraine war, resource wars, GFC and pandemics happen regularly as do oil related wars, so there is no telling for sure when gdp dips and inflation will happen.

Definitely house price fluctuations and the losses suffered by overleveraged investors should never be the lookout of the rbnz, as the profits were not considered when prices were on the way up.

The author also does not consider in any depth the massive benefit to the overwhelming number of kiwis in the medium to long term of affordable houses and rents, investment moving to innovative and productive asset classes and more money moving to the mid and lower classes (more doctors, teachers, nurses etc training and staying in nz).

My opinion is more kiwis will accept a short recession and large house price drop to try to kill inflation faster .. than those who wont. Most of us are sick and tired of the risks to the economy and climate and social adhesion of the property bubble. And long term it is a much better outcome for the next generations

Ps. Sorry for the length of this. But re the comments on reduced house building i remain to be convinced we really need as many more. If immigration is better managed (immigrants and developers were to pay for their required infrastructure directly in advance and all houses were occupied). The world is seeing a reduction in births so we should be wondering how to rid ourselves of old crap housing and lessen infrastructure.

" Its always been that way and the responsibility of the purchaser and their advisors to manage their individual risk."

Except it hasn't. It's been a huge grift underwritten by the taxpayer by people claiming to hold a property for incidental capital gain yet running it at a huge tax loss year after year, at the expense of younger Kiwis, while adding more and more people to ensure there was always upwards pressure on rents and supply constraints.

Now that's no longer a dead cert, it's apparently every man for itself? Sorry, not falling for that one again.

To my that's the problem the law on capital gain has always been reasonable if you where honest, if you in it for gain on the property value then you should be paying tax, if you where in it for making money on rent then you shouldn't. The problem is too many people lied, never intended make a profit and and got away with not paying tax. In my opinion the government should back audit these people and ask, what exactly was you business plan to make a profit without capital gain when every time you approached making a taxable profit you bought another house.

Sorry, but am I missing something here? The author claims that the last time the RBNZ did battle with inflation (2004-2008) it was a relatively modest (compared to now) rise in interest rates here that saw inflation off. I'm pretty sure that it was the deflationary bust of the 2007-2008 GFC that can take most of the credit for that, not what the RBNZ was or was not doing to interest rates. This makes his comparison to what is happening now very tenuous (at best).

It's worth looking closely at the 2006-2009 period closely in terms of what interest rates and house prices were doing. The rise in interest rates did successfully cut the legs out from under the housing market, and prices were beginning to fall quite steeply - the argument can be made that the GFC actually SAVED the housing market from further falls (by mid 2009 it had pretty much bottomed out), as the RBNZ was able to slash interest rates. You often read that the GFC caused the house price falls of that period - not so sure about that........pull up the RBNZ's graph of rates versus house prices and take a look at the actual sequence of events.

While I do agree mostly with Rodney, he does seem to have forgotten that the OCR was dropped to an emergency low not that long ago. So sure the OCR rise has been significant compared to the emergency setting, but compared to say 3 years ago it isn't that much at the moment. However because the RBNZ are predicting an OCR of around 4%, interest rates have already climbed well above 3 years ago.

I think the RBNZ need to at least soften their prediction, even just a simple statement like "imported inflation pressures may be easing and that could lead to a lower OCR peak" would encourage interest rates to be more in line with the OCR instead of being well above.

This doesn't sound very inflationary:

https://www.nzherald.co.nz/business/construction-slowdown-new-build-inq… Construction slowdown: New build inquiries drop by up to 80 per cent, more companies could go bust alongside job losses

Link is mangled, article is still there

https://www.nzherald.co.nz/business/construction-slowdown-new-build-inq…

Thanks, I'm not subscriber to nzherald. But reading by the title, it's the inquiries dropped by up to 80 percent. And it does not surprise me as the house sales are pretty low at the moment. I think we will need more data to come to any conclusion or prediction. The lower inquiries could be the pricing hasn't been meeting the current expectations.

As far as property goes, we are already in a recession. The RBNZ continues to make bad calls.

Also some of the other measures the Govt took to arrest the property boom, should be reconsidered. Things could get really ugly, in the next 18 months, for a lot of NZers.

I'd suggest that 2004-2008 is irrelevant for the purposes of comparison. The inflation was nowhere near as bad, and didn't have the same causes.

I'd also suggest that we're getting ahead of ourselves by fretting about a deflationary housing bust. Our housing 'boom' has been a social catastrophe, and even people who admit as much are seemingly desperate to rescue the bubble before it's even popped.

It hasn't happened yet. And the necessary psychological and political shift hasn't happened, either. If the RBNZ came out tomorrow and announced they're leaving rates where they are for the next year, we'd have another 20% p/a orgy of speculation in no time at all.

The Funding for Lending Programme (FLP) is one of the monetary policy tools we are using to maintain low and stable inflation and support full employment.

Then a couple lines further down

The FLP works by lowering interest rates and encouraging households and businesses to spend and invest.

How can encouraging spending lead to low & stable inflation???

As banks will be less reliant on more expensive deposits and wholesale borrowing, the programme lowers their overall funding costs. Banks can then pass these reductions on to their customers through lower mortgage and business lending rates.

This should read "Banks must then pass the reductions on to their customers". Otherwise, it's just another subsidy for the banking industry (of Australia).

I have the realisation that the incumbents are doing everything to prop up overseas businesses with our hard earned money :(

You are bang on the money. We are seeing a perfect storm for the property market and a complete lack of awareness by RBNZ that this is now the main driver of the NZ economy.

Rate rises are already pushing people who bought last year into selling homes they won't be able to or can't afford to finance. Homeowners will not be upgrading their homes when values are reducing. Gone too are the property flippers as falling values preclude a decent margin on the buy and renovate trade.

With building costs still rising through a combination of the supply chain issues and a weak NZD, there will be little margin for homebuilders to make a turn on new builds.

All this points to a significant downturn in residential construction work across NZ, probably kicking in severely, when the current order book runs dry in six to nine months.

Recession is just a matter of time without further rate rises.

Now there is a propery investor if ever I heard one. We didn't have due care and attention when they lowered rates.... Crash the market. It is NZs societal cancer and needs surgery. Do it with interest rates, do it with punitive taxes on excessive property holding... But fix the problem. Today's immigration announcement hoping to bring in the next round of property cannon fodder so NZs capitalled class can pass on their rentals, is just plain dumb.

This reads like a property investors perspective. OR a person who makes their money out of a positive property market. The whole of NZ has just taken A 7 percent pay cut because interest rates have been too low for too long and were dropped way too fast. Double them and let's get through the pain and out the other side. This reads as if we shouldn't do anything because someone might lose a few bucks....This society has lost way more over the past 10 years than anyone can calculate.

Take the NZs sacred cows, the housing market, Fletchers etc and have a ceremonial slaughter and feast on the carcasses. Tax any foreign owner to the point that owning any rental property to offshore profits is not attractive. Let the banks go under and then bring them back onshore nationalized if needs be. Lastly do forensic audits on all leaders for the past 20 years, and find, out why our sovereignty was so freely traded offshore.. it will be brutal,,, but getting back your sovereignty often is. Ask Sri Lanka.

Doesn't this guy make his money from offering economic analysis predictions to clients on how to profit from housing cycles?

When people start giving away that advice for free it's always worth taking it with a pinch of salt. Their livelihood depends on being able to say how things are going to pan out. Once they start talking about how things "should" rather than "will" pan out it, it sets of my hidden agenda alarm bells as they are trying to influence rather than describe the situation.

Anyone know what he's been predicting up until now?

The real issue is not the rates, it's the potentially crushing weight of debt as rates revert to norm. We need an asset reset. Less rent and less mortgage burden. Everyone should resist govt support for any bailout.

Let the speculative get crushed by their own greed.

Ps great quote above, " NZs societal cancer and needs surgery"

Collateral on the way up was people in cars, crippling levels of employment (no staff available), hopelessness and meth use on the rise, crime being ignored and insufficient police, and now crippling inflation and the wage and price spiral burning down employers.

What additional collateral are you referring to?

I haven’t said there wasn’t collateral on the way up. I agree. I have been talking about the major problems with booming house prices on this website for…..many many years.

But there will also be collateral on the way down.

Why does the discussion have to be so binary? Almost everyone is framing it that way. But it’s a lot more nuanced that that.

we should be trying to avoid BOTH boom and bust. They both come with big issues.

Yep there will always be collateral. But in a market where so few have got so much at the expense of so many, and generally paid very little tax on it, some justice is required. If they can engineer a downturn that only affects the top 2% of property owners, I am all for it. But, our political classes have neither the intellect nor the intestinal fortitude to make it happen, and in the absence of that I would like to see an almighty reckoning that so tars and feathers our politicians that it never happens again.

This has all been avoidable but a lot of politicocrats have got very wealthy making it happen, and perhaps only being forced to flee in the dead of night can bring about a new future that brings hope for all.

A great analysis RD, GDP projections by RB & banks are indeed laughable.

I'll say it again, the problem is the lag between the rising (or falling) interest rates and the resulting effect on... housing, GDP, inflation, eployment etc... That's the main reason why the RBNZ overshoots its response in both directions.

We welcome your comments below. If you are not already registered, please register to comment.

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.