By Jarrod Kerr*

“Give me a word. Give me a sign. Show me where to look. Tell me, what will I find?” Collective Soul

- 2022 will (hopefully) come with greater freedoms, and international travel. The Kiwi economy is well placed, well oiled, and well prepared for another year of solid growth.

- Inflation is the big risk for 2022, with surging costs domestically and rising wages.

- Businesses will have to contend with rising costs, rising interest rates and a rising Kiwi dollar.

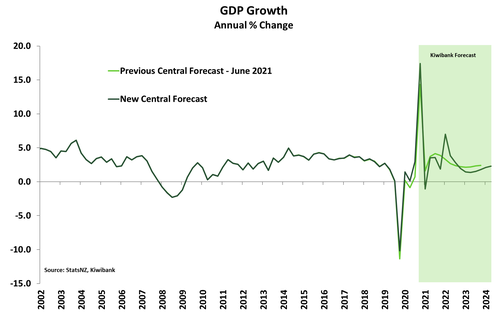

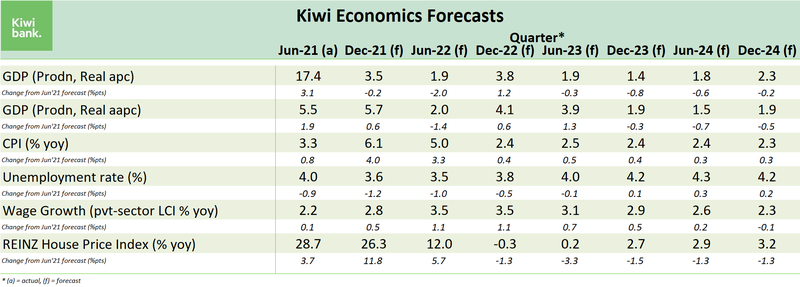

The Kiwi economy has been well-supported by rising house prices, resilient household consumption and robust demand for our exports. Economic activity has returned to pre-Covid levels. The latest lockdown will be a step-back, but only temporarily. Activity has picked up strongly, doing well to make up for weeks of thumb-twiddling. And demand has simply been deferred. Consumer spending rebounded once restrictions were relaxed. 2022 is also expected to be the year of international travel. The long-awaited revival of the tourism and education sectors should see a bigger contribution from these sectors next year. We expect the Kiwi economy to grow at a solid 4.1% over 2022.

However, there’s cause to be cautious. Covid and its yet-to-be-discovered mutations will continue to plague confidence. The emergence and outbreak of Omicron is a timely reminder that the pandemic is not yet over. However, Covid-related restrictions are proving to have a diminishing economic impact. Businesses and households have adapted and are better prepared. It would take a considerably worse disruption than what we’ve experienced to materially derail the economy.

Here’s our key economic considerations for 2022:

- Economic activity: will rebound strongly following the Delta disruption as underlying demand remains robust. But Covid is still the biggest headwind for the Kiwi economy. Rising interest rates and weaker real incomes also challenge the resilience of household consumption and business investment.

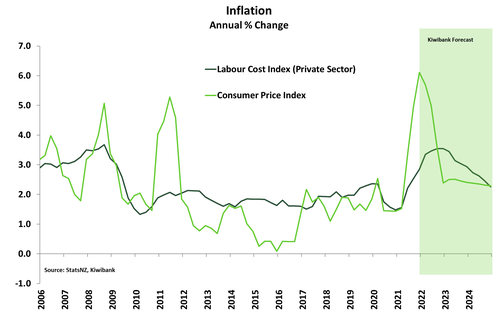

- Inflation: will rise further as cost pressures remain acute. Supply-driven inflation will eventually abate, as global supply chains are unclogged, but there’s growing concern over domestically generated inflation. Wages are on the rise with super-tight labour markets and high inflation.

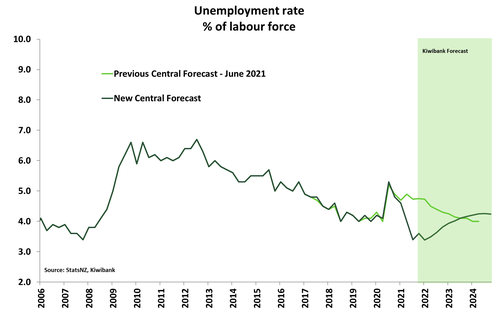

- Labour market: will remain tight by historical standards, with the unemployment rate starting 2022 at a record equalling 3.4%. Hiring intentions have intensified and job vacancies are well above pre-Covid levels. The reopening of the border might be a double-edged sword, with Kiwis leaving as migrants enter.

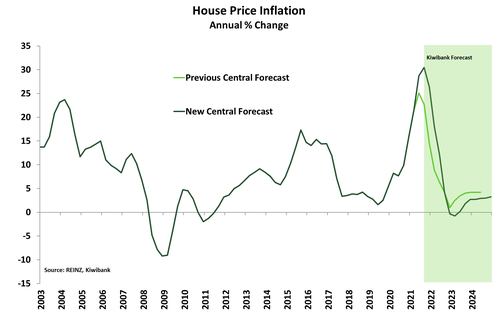

- Housing: is set for a period of consolidation. Rising mortgage rates, tighter LVRs, tax changes, tougher access to credit, and (most importantly) more housing supply coming to market – will weigh on prices. There’s material chance of a modest market correction – house price falls.

Given the state of the Kiwi economy, emergency settings of low interest rates are no longer needed. The RBNZ will continue to normalise monetary policy settings over 2022.

Here’s our thoughts on interest rates and the Kiwi over 2022:

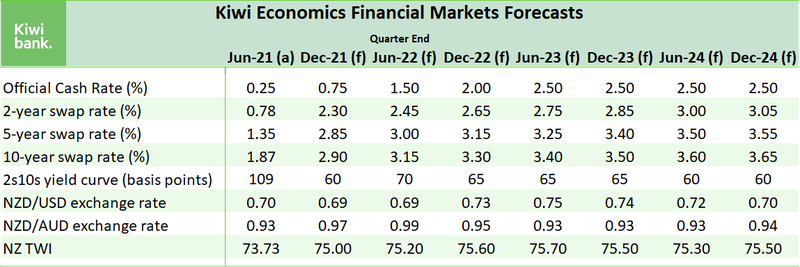

- Interest rates: will continue to rise. The current cash rate of 0.75% has at least another 175bps of hikes in the pipeline. The RBNZ has signalled a tightening path to at least 2.5%. All lending and savings rates will continue to push higher.

- Kiwi exchange rate: is undervalued. We expect to see a stronger Kiwi, with record high terms of trade and supportive interest rate differentials. Upside to the exchange rate however is capped, should other central banks follow in the RBNZ’s footsteps.

An economy stuck in overdrive

The Kiwi economy has been well-supported by rising house prices, resilient household consumption and robust demand for our exports. The latest lockdown will be a step-back, but only temporarily. We expect the economy to contract by around 4.5% in Q3 – far smaller than the 11% decline last year. Auckland, however, was still locked down in October, taking some of the shine off the Q4 rebound. We’re expecting a 3.6% quarterly jump in Q4. The rebound will continue in 2022. 2022 is expected to be the year of international travel. The long-awaited revival of the tourism and education sectors should provide a decent boost to activity next year. Tourists still want to cross NZ off their bucket list, and our universities are still world-ranking. We expect the Kiwi economy to grow 4.1% over 2022.

The Kiwi economy is running above its potential. And a positive output gap (the difference between what the economy can produce and what it does produce) means further upside to employment, inflation and wage growth.

The Kiwi labour market has never been tighter. The unemployment rate has plunged to a record low of 3.4%, despite participation rising to a record high of 71.2%. Basically, if you want a job (within reason), there’s one for you. Leading indicators suggest that the labour market is set to tighten further. Hiring intentions have intensified, job vacancies are well above pre-Covid levels, and expected labour turnover has hit a 50-year high – all this despite the Delta outbreak. However, we do expect to see some, but limited, fallout on the labour market from the latest lockdown. We forecast the unemployment rate to lift modestly to 3.6% in the Dec-21 quarter, with restrictions having dragged on in Auckland – 30% of our workforce. Beyond Q4, the unemployment rate is expected to fall back to the record equally low of 3.4%. The current skills mismatch however means the unemployment rate might struggle to sustain a rate in the low 3s.

Given the closed border, the pool of available workers is limited to homegrown talent. And with employment already above its maximum sustainable level, that pool is quickly drying up. Acute labour and skill shortages means employers are having to pay up to attract and retain workers. High labour turnover suggests employees are leveraging their improved bargaining power to switch jobs for bigger paychecks. Wage growth is already up 2.5% compared to Q3 last year – the fastest rate in over a decade. Also underpinning rising wage growth is the expectation inflation will remain elevated. Inflation has spiked to a 10-year high. Consumer prices are up almost 5% over last year, and the price gains have been broad-based. Annual inflation is expected to peak in Q4 at just over 6%, and remain above the RB’s target band for most of 2022. The costs pressures brought on by disrupted global supply chains will see repeated large price gains in the Dec-21 and Mar-21 quarters. The recent surge in energy and other commodity prices is also yet to feed into the consumer level. However, the rampant rise in shipping costs looks to have ended, and shipping costs are actually falling now. We should see broad-based inflation pull back over 2022.

Rising inflation means the cost of living has and will become even more expensive. And workers will demand compensation. With inflation at 5%, it’ll take a bigger pay rise for households to feel better off. Wage inflation is forecast to continue rising and peak at over 3.5% in the middle of next year before easing in line with general inflation. From a price stability perspective, alarm bells at the Reserve Bank will start to ring if higher inflation becomes embedded in wage-price setting behaviour. Medium-term (5-year ahead) inflation expectations will be closely watched and have already risen to 2.17% from 2.03%.

The housing market has a substantial influence on the economy. Housing is our largest asset class. And the effect of rising housing wealth stimulates consumption. When house prices are rising, households feel more inclined to spend. Moreover, households are more inclined to invest in their largest source of wealth. In a high-demand environment, developers also see an opportunity to profit, boosting construction activity too. Since the start of the pandemic, housing wealth, at least on paper, has risen by many hundreds of billions of dollars.

Cautious consolidation

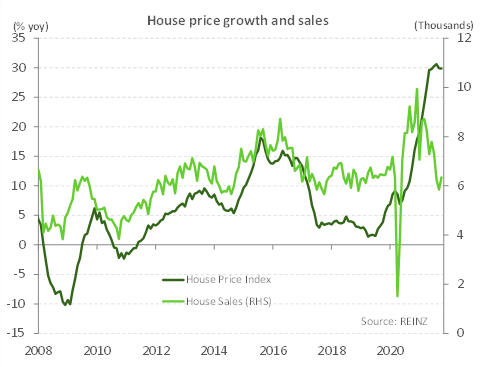

After a year of unsustainable price growth, the housing market is set for a period of consolidation. And consolidation means a strong likelihood of house price falls – albeit modest. The housing market has been propelled by a heady mix of rocket fuelled cheap borrowing costs, a significant housing shortage, and solid employment growth. According to the REINZ house price index (HPI), house price growth peaked at an all-time high of 30.5% in the September quarter. However, this rocket fuel is now running dry. From here, we expect to see house price growth falling fast as an increasing list of headwinds pound the market.

Mortgage rates have risen rapidly since the middle of the year. And mortgage rates have further to rise (see the financial markets section below). Finding a carded 2-year fixed mortgage rate below 4% is now nigh on impossible. At the start of the year, with the prospect of a negative cash rate, a 2-year rate in the low 2s was common. Increasing mortgage rates have driven up the cost of servicing a mortgage. Disposable incomes will be reduced as mortgage holders roll off record low mortgage rates. More importantly, rising mortgage rates reduce the amount that households can borrow, lowering their potential bids. For sellers, a quick sale may mean lowering their price expectation. Rising mortgage rates are a clear coolant on housing demand.

Another coolant on demand has been numerous housing-specific policy changes introduced this year. The Government announced back in March, tax changes targeting investors. The changes included tightening the bright-line test and removing the tax deductibility of interest expenses. The RBNZ got in behind the call to restrain investor exuberance by tightening investor loan-to-value ratio (LVR) restrictions. The share of lending going to investors fell soon after. Since then, LVRs have been tightened for owner-occupiers too. Finally, and perhaps somewhat unintentionally, recent changes to the Credit Contracts and Consumer Finance Act (CCCFA) will likely reduce credit availability. The legislative changes that came into effect from 1 December put increased onus on banks to demonstrate borrowers can afford a mortgage. Failure to comply comes with the threat of large fines. Lenders will probably err on the side of caution when it comes to riskier borrowers and deny credit.

Supply is also set to weigh on house prices over the year ahead. A record 47,715 new dwellings were consented in the 12 months to October – that’s up 26% on the year. The lift in housing supply has occurred at a time when a closed border has seen population growth plummet. Looking ahead, a cooling housing market combined with the capacity and labour constraints in the building industry will likely cap the rate of home building somewhat. We don’t see an immediate flood of properties if the new housing densification strategy is approved (see The future is brighter for the supply of housing).

A reasonable predictor of house price growth is sales activity. But since late last year, sales have fallen while house prices have sustained record highs. The reason why has to do with record low levels of listed property. A combination of the housing shortage, and the psychology of a bull property market. Selling in a market with limited supply risks not being able to buy back in. Sellers risk watching possible juicy capital gains slip away and, when re-entering the market, having to accept a lower rung on the property ladder. A similar psychology also drives eager first home buyers – so called “Fear of Missing Out” (FOMO).

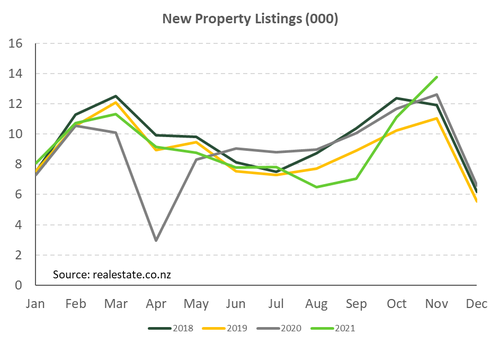

However, the dynamics in the market are starting to change. The number of new property listings are trending higher compared to recent years. And a lift in new listings is particularly noticeable in regions in the lower North Island such as Wellington, Whanganui/Manawatū, and the Hawke’s Bay – previous bastions of market enthusiasm. As the market fails to absorb the new listings, properties hang around for longer and the market becomes a buyers’ one. We are forecasting very modest house price falls this time next year. Somewhere in the order of -0.5-to -1%. More of a consolidation rather than a correction. Other forecasters, such as the RBNZ, see much larger falls ahead. However, looking at the past 30 years meaningful corrections typically occur when credit conditions tighten rapidly, and we have an unemployment rate rising fast. Looking ahead we certainly have tightening credit conditions and rising mortgage rates. Yet over our forecast period the labour market is a source of strength in the economy not weakness. The unemployment rate is expected to remain consistent with what would be considered consistent with full employment. We are reluctant to project sustained house price falls as a result.

A grand reopening of sorts

After almost two years of Covid-related restrictions, the NZ border is finally set to reopen. The doors aren’t being flung open though, just creaked open to start with. But it is a start. From mid-January, MIQ requirements will begin to be removed, starting with travel to and from Australia. Instead of an extended stay in MIQ on arrival, eligible vaccinated travellers will only need to self-isolate for seven days. And if arrivals pass the standard Covid tests they will be able to enter the community, assuming the Omicron strain of Covid doesn’t mess things up. The announcement provides a light at the end of a long tunnel for tourism.

Opening the border has two key influences on the economy. The first is on net migration, which is a key driver of NZ’s population growth, medium-term demand, and labour supply. And second, services exports such as tourism and education. The initial impact on net migration is uncertain. We may see an initial jump in long-term departures, as those itching to go on an OE will be comforted knowing they won’t be shut out of Aotearoa by a lottery of MIQ spots. However, over 2022 we expect to see net migration begin to lift as NZ’s overly tight labour market attracts people in to plug skills gaps. Our view throughout Covid has been that when net migration does recover, it’s unlikely to get back to the highs seen pre-Covid of an average of around 60,000 per annum. The Government has already signalled a tightening of immigration policy and we are picking a peak in net migration of around 30,000 over the medium term. A lower peak in net migration means the construction sector is better placed to meet the demand for housing.

For the tourism industry, the planned changes are unlikely to provide as much of a boost for tourism operators as might be hoped for. From 30 April anyone fully vaxxed can plan a trip to Aotearoa. However, NZ is a long (and expensive) way to travel to spend the first seven days stuck in a hotel. Self-isolation requirements will likely put off many. We should see more trans-Tasman tourists here visiting relations. Unfortunately, these visitors don’t tend to spend as much on seeing the sights. The focus tends to be more on spending time with friends and family. The education sector will likely fare better, as a seven-day isolation period is less of a disruption for someone studying toward a multi-year qualification.

The end of cheap money

Interest rates have risen around the world, but remain at very low levels. Given the spike in global inflation, interest rates are destined to rise swiftly next year. Over the last 15 years, inflation has consistently surprised on the low side. Ageing populations, forever cheaper technology, and ecommerce giants (like Amazon) have put downward pressure on prices. It was only prior to the 2008 GFC where we saw inflation running above central bank mandates. Yeah, that was short lived…

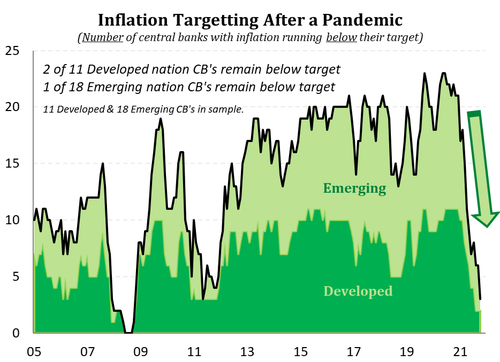

Just last year, all developed world central banks and most emerging world central banks had inflation running below target. 2020 was looking awful. One year on, and inflation has exploded. Of the 11 developed world central banks in our sample, 2 have inflation running below target (Switzerland and Japan). 9 have inflation running above their mandated targets (generally 2%). Most have yet to commence policy tightening, including the US Fed (inflation at 6%), the RBA, the ECB and BoE. And it is not just a developed world problem. Of the 18 emerging world central banks, only 1 has inflation running below target (Indonesia).

Most of the global inflation pressure can be put down to strong demand, disrupted supply and high commodity prices. The disrupted supply looks transitory. But the domestically generated inflation is on the rise also – with tightening labour markets and rising wages. Almost all central banks remain cautious. Almost all central banks are well behind the RBNZ. And almost all central banks will find themselves lifting interest rates next year.

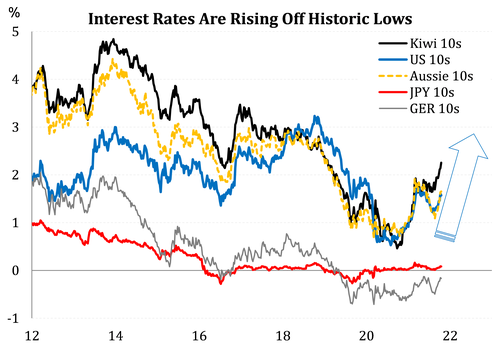

As central banks around the world start lifting their cash rates, to combat inflation and return policy to more normal settings, all interest rates will push higher. And global interest rate moves will put further upward pressure on Kiwi interest rates (beyond 5 years). The likely (upward) move in global interest rates comes at a time when the RBNZ is already in hot pursuit.

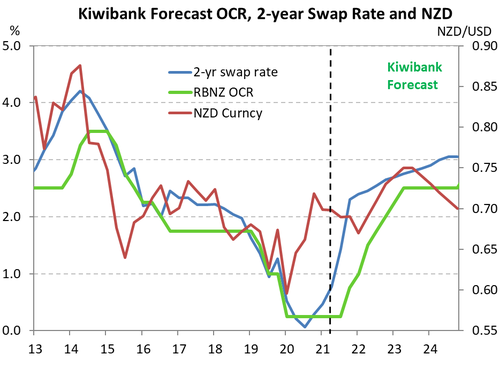

The record low interest rates of earlier in the year, even lower than the lows of the 1950s, are no more. The time of cheap money is over. The RBNZ is normalising policy, by taking interest rates back to more normal levels. Wholesale rates markets have factored in the higher rate path. And the wholesale funding costs for banks have risen sharply. Mortgage rates have risen in response, and we expect to see further hikes from here. The current cash rate of 0.75% has at least another 175bps of hikes in the pipeline. A cash rate of ~2% is considered neutral (neither tight, nor loose). The RBNZ’s OCR track implies, for the first time in a very long time, that the RBNZ will need to tighten policy through neutral to contain the economy, esp. housing. The RBNZ has signalled a tightening path to at least 2.5%.

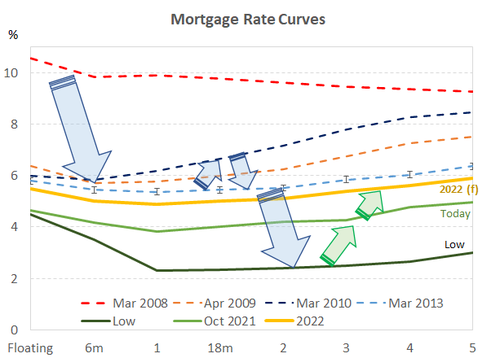

The Kiwi mortgage curve has moved a lot since 2008. Prior to the GFC of 2008, mortgage rates peaked above 10%. The carnage of the financial crisis saw mortgage rates slashed towards 6%. Mortgage rates then fluctuated for years but hit an air pocket with Covid. The Covid pandemic saw mortgage rates slashed further, down to the lowest levels in history. The emergency settings were designed to insulate an economy in lockdown. The economy proved to be far more resilient, however, and house prices rose an unsustainable 30% over the last year. There's no longer a need for emergency settings.

Now, mortgage rates are rising back to 'more normal' levels. The green line in the chart below shows the average mortgage rates currently on offer. And the yellow line shows our forecast for mortgage rates over the next year. Most fixed mortgage rates will be 2-2.5%pts higher than the record lows recorded earlier this year. These higher mortgage rates come at an awkward time.

70% of outstanding mortgages are due to roll over in the next year. 70% of mortgagees will potentially face much higher mortgage rates as their loan rolls over. Because mortgage rates have since lifted considerably, and are likely to continue rising from here.

The impact on discretionary spending will need monitoring, with higher debt levels and higher interest rates. Households have taken on more debt and will be more sensitive to rate rises.

Kiwi currency still looks strong

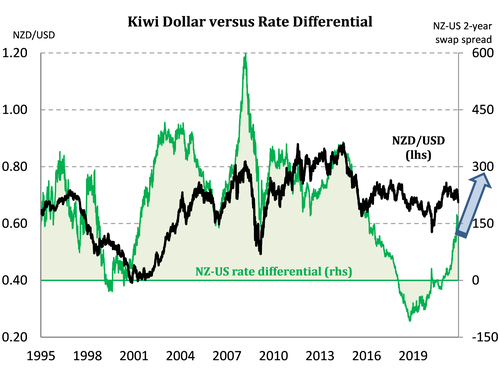

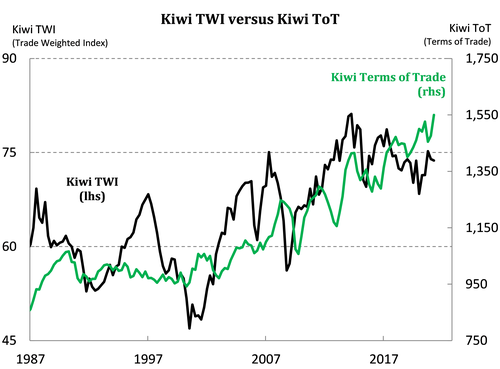

There are two key drivers of our Kiwi dollar forecast, the terms of trade (export prices relative to import prices) and interest rate differentials. NZ’s terms of trade is at record highs, suggesting our currency is undervalued. We do, however, expect the terms of trade to wane a little over 2022. The softer trajectory suggests a lower peak in the NZD. We have lowered our forecast for the NZD accordingly.

When it comes to interest rate differentials, the RBNZ is well ahead. We continue to see our interest rates rising at a faster clip than those offshore. The wider differential continues to point to a stronger Kiwi dollar.

Our forecast for the Kiwi looks for some near-term weakness, as the RBNZ does not come back into play until February, and the Omicron variant poses risks. But over the year ahead, we forecast the Kiwi to regain some strength. We forecast the Kiwi dollar to hit 0.73c next year and peak possibly as high as 75c into 2023. The Kiwi flyer’s ascent however is capped, should the Fed tighten policy more aggressively. In November, Fed Chair Powell said that rate hikes in 2022 were “extremely unlikely”. However, US inflation is running at 6%, with further upside. And Powell has since relocated from camp “transitory” to camp “persistent”. Rate hikes in 2022 are no longer “extremely unlikely”. There’s downside risk to the Kiwi exchange rate with central banks (inevitably) following the RBNZ’s footsteps.

We note that predicting the volatile Kiwi currency is fraught with danger. We expect to see a wide range in the Kiwi between a low of around 63c and a high of as much as 75c. That’s our way of saying (again), we have great unconviction in our Kiwi forecast.

*Jarrod Kerr is Kiwibank's Chief Economist. This article first appeared here and is used with permission.

113 Comments

...consolidation means a strong likelihood of house price falls.

Same forecast as last time then? https://www.newsroom.co.nz/bernard-and-jarrod-how-far-might-house-price…

This isn't how real-estate bubbles work, they either self re-enforce existing behaviour or they collapse rapidly. Consolidation and moderation just don't happen at extreme valuations.

Is that a 'sarc' comment?

By historic standards interest rates are certainly low, but that's of limited relevance.

The market in 2022 will be ultra sensitive to interest rate rises. That's because the raises are on debt (mortgages) that are much higher than they have ever been.

Going from a very low to a low-medium rate on a 300k mortgage would not matter so much. Doing the same on a 600-800k+++ mortgage does.

The current context is much different than it's ever been.

Also the construction sector will crash as demand falls away. There's a big article in the Herald today, no doubt the first of many as problems build.

You seem to be missing the point. If interest rates rise, that debt needs to be serviced. The "bank of mum and dad" might have equity, but the buyer still needs to service that debt. The majority of the boost in house prices over the past 18 months was caused by a drop in interest rates and those rates are likely to completely unwind.

That seems a doomsday scenario to me. The commercial construction will adjust their time fram. Instead of having an order book over a year or two it'll reduce. Residential housing is another animal. but in a similar position. Instead of saying next year it'll be maybe in six months.

The only departure I can see to the doom facing housing and construction is anyone who was genuinely ready to buy a house now wanting to do so and lock in before rates rise further. Hopefully they'll get the opportunity to negotiate a better price on more listings at an interest rate that's cheaper than what it will be later in the year.

"....they either self re-enforce existing behaviour or they collapse rapidly. Consolidation and moderation just don't happen at extreme valuations."

This are characteristic of any pyramid ponzi.

Only difference this is supported by parliament and reserve bank of the country so unfortunately can use their power to delay for vested biased interest.

Yes as a home owner/investor I find myself in both camps, disagreeing with myself. Why blow billions more steadying the ship when we had 80 percent plus vaccinations. While "long term renters" such as yourself (which I find hard to believe btw) end up paying the price. Stay resilient!

"If the multi-billion dollar wage subsidy had sat in peoples' banks, then it wouldn't have achieved its purpose."

No it wouldnt have....of course it could have been more widely distributed...however you miss the point(s)

The housing market was a consequence, not the saviour....

and its temporary (or "transitory" if you prefer)

What seems to regularly lost in this commentary is the elastic nature of construction activity to hoise prices, and the significance of the construction sector to our overall economy (16% was it?)

Less confidence in housing = less confidence to start or continue construction activity = less confidence overall.

Yes he and most other economists don't get it and can't see it. The only one that is talking about a significant fall away is residential construction is Tony Alexander.

There's a very clear relationship between rising interest rates, reduction in house price growth and reduction in construction activity, and economists should know this. Then throw in the curveball of massive building cost increases from covid-generated supply chain problems.

Right after the lockdown, it's evident that the car parks at all the shopping centres are filled to the brim. This will just mean a RECORD HIGH quarterly retails sales data print in the economic data soon and at a time, when inflation is rising. When there's so many negative economic views out there, it leads to most people being underprepared when prices for everything go up for everything in the new year amongst the global supply chain disruptions particularly if inventory is exhausted.

My household has been part of that manic shopping behaviour but I can safely say that it is a one off. If anything because of our spending spree our retail expenditure is likely to be significantly less than normal in 2022.

Part of the reason was that we genuinely needed to get quite a few things, another part of it was a feeling that further price rises will come and FOMO - that appliance (which we don't *have* to get now but do within a year) in the shop today mightn't be available tomorrow or next year. And if it is, the price might be higher.

I bet this behaviour is being quite widely replicated.

Exactly the reason we replaced our 13 yo fridge last month & bought a new (ex demo) car replacing our 16 yo one at the beginning of the year. Also why I could sell my 10 yo NZ built boat inside a week for the same as the new boat price (new boat build lead time had also increased from 2 to 12 months).

family’s that have borrowed 1 million for house once interest raise too say 6% over 30 mortgage cost would be around $6000 a month. Net average income $4000 if you have 2 people say $8000 , leaves 2000 a month once food power rates car water petrol any credit cards or loans I would think these people would just be existing is this what the government and people want a country where average kiwi are just existing.

Answered your own question there.

Due to our pathetic low wage, low productivity economy, thousands have always just existed. It's the kiwi way. That's why so many leave. So yes, this is what the govt want, esp so they can dangle a carrot and complain about those evil capitalists so as to elicit more votes for their socialist policies.

Inflation is here, the central banks have pumped up asset prices and consumer demand. They are too slow to reduce money supply and increase rates. Some options:

- inflation gets imbedded as its driven by demand not supply problems. All problems are demand side. We are seeing this in commodity prices as free money speculates in the markets. Central banks are too slow (you need to preempt it not react to it)

- central banks move harder and bring down inflation. Unlikely.

- omicron causes a large demand reduction (unlikely) deferring demand and giving central banks and government some breathing room. They will be wishing for this but it's unlikely given the data that's coming through.

- there is a hidden bomb somewhere in the markets that explodes (such as China housing?) And removes demand like happened in 2008. Central banks get off the hook again and turn on the printing prices and asset prices continue to grow.

Which option would you like? Long term we need to kick the money printing cheap money asset inflation to touch. It's disproportionately benefiting the asset rich.

So to sumerise.

Inflation up 5%

Wages up 3%

Growth 4%

Interest rates up 30%

This is all positive because........ housing

I didn't see anything in there for a non house owning 30 year old well skilled person to say NZ would be a good place to stay/shift to. Infact I'd see them completely ruining the population growth guestimate by running in the he opposite direction.

"The Kiwi economy has been well-supported by rising house prices". Just what does that mean? I am told that my house has risen in value by over $200,000 in the past year, but how does that 'support the economy'? That hypothetical figure adds nothing to GDP.

If I rush to sell, then there is some marginal economic activity in fees, moving costs etc but nothing that significantly affect economic activity. To do that, I would have to use my home as a cash machine and borrow to buy stuff. Is that healthy economic activity or not?

I think not, but perhaps I am just old-fashioned.

tomjones_04,

Thank you, but I have just found out that my younger son and his wife intend to put in a swimming pool next year-and not with cash!

Clearly my 'wisdom' has not reached very far. In their defence, they earn a lot, but It's not something I would have done.

Exactly what happened in the US before the GFC. Houses become ATM's. (did it myself, a free lunch). No; you are just using equity to consume more, ask the banker, he loves a refinance and look interest rates are lower.... We are a clone of the US, just trying to catch up. Only difference that Orr fails to comprehend is the US has the world's reserve currency, so can always pay their debts. NZ does not have that luxury, unless we produce more than we consume. Not. Damn Covid.....

... and ... most countries have a broad based economy ... so , they can service higher debt levels than a one trick pony economy such as ours , Fonterra milk powder & sweet bugger all else ... we're in so much trouble if Predident for life Xi falls out of favour with us ...

...experts say there may now be too many homes being built. ...extra supply of a thing will constrain prices, but that’s not the same as saying there are not enough houses for people to occupy. Prices have not soared 39 per cent since March 2020 because population growth has boomed....record low interest rates and the temporary removal of loan-to-value ratios were the reason...when the borders open a generation of young Kiwis will depart our shores for Australia for the higher wages on offer and lower cost of living, and to embrace some freedom after two years being cooped up. Add in catching up on two years’ worth of OE, and we get a movement of the net annual flow of Kiwis back into negative territory, as has been the norm. The past few years from 2015 have been unusual.

https://www.stuff.co.nz/life-style/homed/real-estate/127201554/could-we…

Net migration of Kiwi's has been negative for years. The real question is what the government will do with immigration, as both Labour and National have been happy to keep create the illusion of economic growth by just adding people and underfunding the infrastructure to support it.

Labour have claimed they are looking at an immigration reset. The productivity commission has labelled our pre-covid immigration settings as unsustainable. But I will not be shocked if they quietly ignore all of that and just go back to 50K per year net migration.

.. some months ago , Sir Bob Jones wrote a piece on his " No punches pulled " site , that the trend of the 1970's/80's will resume in NZ when covid restrictions are lifted ... younger Kiwis will flock to Australia ... a brain drain again ... better jobs , higher pays , cheaper groceries .... cheaper houses ... who'd have thunk that ... cheaper houses in Oz than NZ ... and , a Prime Minister who can say " sorry " ... a leader who doesn't talk down to his people as if they're errant kindergarten children ...

Hate to be negative but I don't know why people think the world is getting a better place to live, its not. 2022 is going to be a bad year for anyone up to the eyeballs in debt, if it doesn't kick you between the legs next year then 2023 at the latest. Banks have finally stepped in to tighten lending but I think its a bit to late and now those maxed out are hoping the rates stay low for at least 5 or 6 years. These people are now adrift in the middle of the ocean in a life raft and have have as much control over rates as the weather. My financial advice is start smashing that debt now.

Globally, societies, both Public and Private, are now utterly dependent upon one thing, and one thing only - the capacity to borrow. Ultimately, there's only one way to keep that going, and that's the same thing that kept us going during the 'pandemic' - we pay people to do nothing.

In Cost of Debt terms (% rates) that sees us plunge into the world of negative interest rates. Not just a few isolated Sovereign Bond rates - all rates. People will be paid to borrow, by making the repayments add up to less than the amount the drawn down. Buy a house today for $1million, and pay $900,000 back over 50 years. Do we understand what that is going to do for asset prices? I'm not sure if we do (and see them go up, isn't the answer)

bw, you say "People will be paid to borrow" (because of negative rates) then you also say "Do we understand what that is going to do for asset prices? ... see them go up, isn't the answer"

Care to elaborate? I would indeed expect negative interest rates lead to higher asset prices, pay me to borrow to buy a house and I will indeed buy one or two or three...

If you buy an asset (or lots of them to reference your question!) for $1million and the net cost to you is $1,100,000 (after paying debt cost etc), what is the least you have to sell it for to make a profit? $1,100,001.

But if you buy an asset for $1million and the net cost to you is $900,000 (after paying, say, negative debt cost etc), what is the least you have to sell it for to make a profit? $900,001.

And....the next owner that gets if from you at '$900,001' only has to get $800,002.

And what other income (wages) does each successive owner need to support their lifestyles as asset prices fall? Less.

I understand your point but I think your logic is flawed. I think the correct logic is: if people get paid to get a mortgage to buy a house, many more people will indeed buy more houses. Many more buyers has only one outcome on house prices and that's to increase their price. If you're not sure, just picture the auction rooms full of buyers, they will probably have to run auctions in large gymnasia or other public halls.

And what does that auction room look like if you're standing in it with your asset to sell with a reserve of $900,001 rather than $1,100,001? And....you know that at some future stage, the lucky bidder will be able to accept a bid for it for less than he pays you? And perhaps more importantly, you know that other vendors at the auction can undercut you as well, and still make a profit?

How many more homes will be built if the end cost is $100,000 less than the entry price? What will that do to re-sale numbers of existing stock in that auction room?

You know my view. Mortgage Rates ; all lending rates, are going to 0%, but.... Debt will be redirected away from speculation (1 property mortgage per IRD number, say, and an LVR of 0% after that) and aimed at productivity. We all know something has to be done. It's only a matter of "What" and "Who has the courage to do it", and if we don't do it in a controlled manner, it will come anyway.

A good analysis/forecast.

I think an important metric is being missed, the billions of $ paid by the government in the form of wage subsidies and Resurgence support and the significant fact that these billions of $ will stop being paid out in 2022. I believe the NZ economy will not be "roaring out of the 2021 lockdown back into overdrive" in 2022as expected.

NGK, no not every adult Kiwi has paid the REagents, only the ones who sold a house.

Also there is no "ponzi schene run by RE", the price of each house sold is determined by how much the buyer is willing to pay and how little the vendor is willing to accept. The RE agents simply facilitate the sale by bringing the price gap between buyer and seller.

You should really learn a little how a house sale transaction works, I take it you have never bought or sold a house before.

A few Yvil and I always expect the agent to get me the highest price when selling... the same goes for buying, I know the agent is working to get the highest price for their vendor - they're certainty not helping you as the buyer.

Maybe you've sold yourself short with previous properties?

With investors out of the game because they now need equity and have reduceding tax rinsing offset, sales in 2022 will be dictated by fhb'ers ability to borrow. Those pre approval levels are being lowered across banking.

The proof is indeed coming soon. Who can bail out the stupidly in debt when their resign comes due as most are in the next 18 months?

"and our universities are still world-ranking", ah nope. Auckland ranks highest at 81st in the world. However, we have never been the first choice destination for students. Our attraction has been the pathway to residency, which then eventually opens the door to pop across the ditch to Australia. The right to live and work in Australia or Canada is the big goal.

Interesting viewpoint. Bank economist predictions have had a 50/50 outcome at best. Some you get right. Some you don't. Kiwibank will get 50% if they're lucky. The national & indeed, international situation today is so complex that any one of a hundred factors could play out, and from any angle. Locally we copy & paste what the Fed tells us to do, but global influences from other major players are right up there. Read China. The only way to sustain the current set up is with wholesale debt forgiveness, which is a tall order from where I sit. A financial reset is already underway with distributed ledger blockchain technologies already in high demand as the trust in central bank controlled currencies falls away dramatically. This is step change I believe, through a collapse of confidence in politics, politicians, commercial banks, central banks & authorities generally as well as the realisation that we've been undersold in our education systems for many years. This is being seen in our poor attitudes generally, poor relationships, poor communities, poor families & a general decline in the way we treat one another as we all head into our little bubbles. All the while slagging off the others who don't work, won't work, won't go to school & do only want to learn certain things in certain ways, rather than what the big ugly reality really is. Hence we are falling further behind our trading partners especially in the Asian region. The culture of freedoms past has gone. Our current freedoms are now relative. If you do not comply you are sidelined. Big Brother (or should that be Big Sister?) has arrived.

The only way to sustain the current set up is with wholesale debt forgiveness

Sounds right.

And a way of achieving that is....slowly. Loans that are re-set at, say, minus 5% are effectively, Debt Forgiveness over time.

What did The System do when the GFC hit and some parts of it got into trouble? Took them into Bad banks - and forgave the debt over time.

This time, it's The System in its entirety that's at risk of failure (your comments) and so there is no entity to float the Bad Banks.

It can be done. But....New Debt has to be redirected away from asset speculation. Asset Creation, sure. But not recycling what's already been created with new debt.

.. our capitalist system is always corrupted and at risk of meltdowns so long as governments backstop the banks ...

If they're deemed too big or too important to fail , then they have a platinum pass to lend with an overabundance of exuberance ... nothing to lose ...

Before 1913, banks that overlent for speculation went bankrupt. The privately run Fed will not let that happen to their personal banks. Wage earners (debt slaves) and savers will always suffer first. Banks will always be bailed out at the fear of a financial collapse. Kinda like vaccination, fear driven. The true productive economy would never suffer from a 'financial collapse' as the banks like to promote. Any bank can create money out of thin air by pushing a button and they should only survive if they do it in a productive manner. But no; the Fed will not let their personal banks fail. GFC was about banks going bankrupt for their reckless behavior that is always promoted because they can never fail. But the beat goes on and the beat goes on.

Before 1913, banks that overlent for speculation went bankrupt. The privately run Fed will not let that happen to their personal banks. Wage earners (debt slaves) and savers will always suffer first. Banks will always be bailed out at the fear of a financial collapse. Kinda like vaccination, fear driven. The true productive economy would never suffer from a 'financial collapse' as the banks like to promote. Any bank can create money out of thin air by pushing a button and they should only survive if they do it in a productive manner. But no; the Fed will not let their personal banks fail. GFC was about banks going bankrupt for their reckless behavior that is always promoted because they can never fail. But the beat goes on and the beat goes on.

I think the KiwiBank economist is wearing his rose tinted glasses today. Banks are part of the problem so you can only expect propaganda and little in the way of what problems are on the horizon. I think people understand that the situation is much worse that he lets on. Even in Aussie, I came across this:

'In Hobart 60% of workers could afford fewer than 10% of homes for rent. While the bottom 80% of workers could only afford 10% of homes for sale.'

This is not a sign of a well functioning, healthy economy or society.

It only "functions" because of continual injections of debt, and of course it's the banks pumping in the debt, that makes them the number one most important institutions in the economy.

Except of course the reality is they are the problem not the solution. Hence in the article many negatives are looked on as positive and positives negatives.

.. true , that ... we're floating atop the biggest debt & inflated assets bubble ever ... worldwide ... ever !

Recall the irrational exuberance of the dotcom bubble in the early 2000's ...

... now we have houses & cryptocurrencies , priced mega times out of reality...

Not many people on here remember late 1980’s early 1990’s housing crash happened in uk most places lost up to 50% was 10 years before house prices recovered .I would say coming form such a large amount of borrowing even if interest rate only hit 6% with inflation this is going to be just as big of a crash. Hard to believe people happy to borrow million plus for poorly build house in area’s where crime is a way to make a living.

... now we have houses & cryptocurrencies , priced mega times out of reality...

So what's your benchmark for pricing? We can observe house prices to income over time and suggest 12x is more 'over-priced' than 4x.

But how about crypto. I assume you're referring to Bitcoin. How do you assign a benchmark to suggest its price is 'out of reality? It's not a question of affordability as anyone can buy an equivalent amount of BTC for NZD10. So why is it 'priced out of reality'?

Furthermore, where is the counterparty debt for BTC? I own BTC. That ownership is not based on a debt obligation. BTC cannot be 'lent into existence' under a debt obligation.

... early 2000s we had millions of men in their 20s & 30's piling aggressively into internet stocks ... the dotcom bubble ...

Two decades later , we have their boys going hell for leather into cryptocurrencies ...

... history does not repeat exactly , but it sure as heck fire rhymes ...

I see. So speculation is all about the 'young fellas'. Comparing the likes of internet stocks and NFTs is somewhat misguided, but I guess that's how the mainstream thinks about the emergence of crypto, NFTs, and even the metaverse.

The problem with how you see things is that the 'young fellas' are quite open to the idea of digital assets falling 80%+, whether it be the value of an NFT or the price of a crypto. In the latter, we've already seen it happen. More than once. In the space of 10 years.

So I don't think you're predicting anything that people don't know. In fact, I wouldn't be surprised if they know it better than you. They have skin in the game.

.. cryptocurrencies are to the mainstream financial world , what anti-vaxxers are to medical science ... a great fear & distrust of the government regulated system ... a middle finger to the power brokers ...

But ... how had that panned out historically, hmmm ? ... the politicians , bankers , ruling elites have always prevailed ...

... yet you somehow think , " this time is different " .. .. good luck !

Completely agree with you. The whole monetary system is being challenged. But it's not a zero sum game. You do have to ask yourself why so many feel threatened by it if it's little more than a pie in the sky scam.

I think you overestimate the power of the boomer paradigms. Their systems are not omnipotent, even if they have a firm grip on power.

I'm gonna throw my two cents in.

I think housing will go for a bath mainly in so far as construction companies and builders and a few sub trades could go under later in 2022. Any developments they're working on could hit the skids, likewise buyers of them will retreat to existing houses for fear of price escalations and inability get the loans.

Winter 22 could start to get really ugly for home sellers. With tons of listings all over the place and few buyers. A few distressed sellers.

Areas lacking in infrastructure, transport and jobs could get oversupplied with new and existing houses. Particularly Auckland, Wgtn and Chch given prices being asked. They just don't add up to me.

Apartments and townhouses all over NZ will be toast. Kiwis want houses with a bit of land even if it's only a tiny courtyard lawn.

Auckland apartments toast.

Auction clearances down in Aus too. Spoke to my cuz today in Sydney, market turning there so he's planning to buy later next year.

Those who can hold on and not sell will do so but maybe with rates increasing that could get harder.

Lots of tradies will talk about leaving and the trickle could turn into a torrent by 2023 even though Aus housing also coming up against same factors. But most kiwis don't follow what's actually happening there so well be unpleasantly surprised.

The economy could really splutter by end 22 and into 23. It will become political. Big time.

Just what Mr Luxon is looking for, a platform to rally the converted.

- Immigration

- Foreign Buyers' Ban

- Local Government, Environment and Resources Consents Acts

Looming property market problem? Solved. (It would make one despair if it wasn't all so predictable)

Agree.

Oh look, housing problem! Kiwi debacle the solution to everything.

OK no, bury that.

Oh look covid... money printing, house prices. Houses must not fall.

Builders pile in, everyone piles in.

Frown.

Oh look problem. Too many houses.

Hmm... no wait, property can be the solution. Who and what will the solution be??

I think the govt will try and pump it cos the economy is so connected to it now. Houses are the economy as we know.

Can't honestly see massive price falls as kiwis just won't sell.

Houses cannot fall or banks will end up insolvent. Orr will take a page out of the Fed's playbook and lower the low interest rates and throw in a little QE because we 'have a liquidity problem'. Keynesians are so predictable and so manipulative. Economists do not run central banks, Bankers do....

We welcome your comments below. If you are not already registered, please register to comment.

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.