Realestate.co.nz has released its December 'Property Report' setting out listing levels and asking price averages. It describes a market in a growing funk.

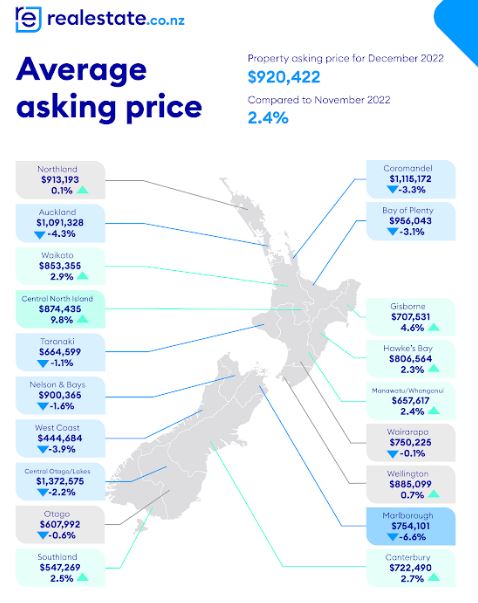

Asking prices are falling. Nationally in December they were -5.5% lower than a year ago. Much of that was driven by sellers becoming more realistic in Auckland.

In Auckland they were -11.5% lower than year-ago levels, the largest fall in asking prices ever recorded in the Queen City, down -$141,000. A third of that fall happened in December from November. That is a -$49,400 fall in December from November, the second largest monthly retreat ever recorded (after the -$53,400 dive in January 2018 from December 2017).

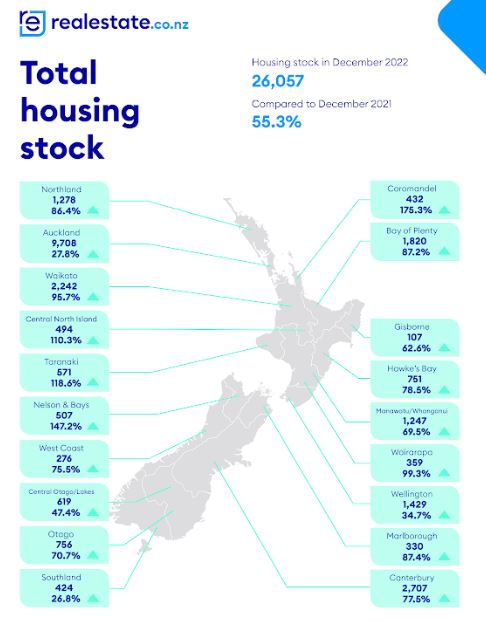

The number of listings available have been rising in 2022 ending the year at 26,100. This is not a high level compared to the record high 60,000 in 2008. We are just back to 2016 levels.

In Auckland the levels are at ten-year highs however

As is typical nationwide, sellers tend to take down their listings over the December-January period. The realisation that prices are retreating may induce more sellers to stay out of the market. As we saw in the Barfoot December sales results, transaction activity is unusually low as sellers struggle to accept the new realities.

Even at the lower levels of listings, they still represent a substantial overhang in dwellings for sale in this market. There are now 28 weeks of listing inventories at the current rates of sale. That is up from 11 weeks a year ago, and up from 23 weeks in November. The largest deterioration has been in the Coromandel.

The shift from November to December was the largest rise in this overhang since the GFC (ignoring the twists in the early months of the pandemic in 2020).

2023 is starting out as a buyers market.

Housing inventory

Select chart tabs

119 Comments

The rates going higher has only just started to take down way overpriced housing market. 2023 could see another 20% off house prices and if world downturn is worse than expected a massive crash could happen, hopefully in 2024 inflation will be under control but the chances of low rates again are small you would think central banks have learned their lesson.

One of my grandads was a POW in ww11 he managed to escape to Switzerland but could not leave there till end of the war many of the others who escaped we’re killed. Not to sure what this has to do with house price’s TTP but don’t mention the war I did once but go away with it.

DTRH… I think your comment is fair. TTP doesn’t like comments that fall outside of his ventures, so he comes out swinging. HW2 is exactly the same. I don’t mind their commentary, I just spar with them because they occasionally come out with witty/funny rebuttals. I think the election is the only hope for the property investors, I don’t think it will make much of a difference if Nat get in personally. Too much downward momentum by then. I think mid 2024 before things flatten

Asking prices are quite a good measure of sentiment in a falling market. In a rising market, they can be dismissed as wishful thinking. In a falling market, they're an indication of what people are prepared to accept.

In both cases, if properties aren't selling, then market value is below the asking price. The difference is that in a rising market, sellers can dig their heels in and wait for the market to catch up. In a falling market, it's a race to the bottom.

It would be good to see a table of prices by NZ region on Jan 2020, and prices now to see how far we have to travel just to get back to pre covid madness.... In most parts of the world its between 5-12% (Thinking London, Melbourne etc) but we had a special form of madness here.

Found old REINZ report Feb 2020 so for end of Jan 2020

National Avg price 615k 810k 24.1% fall required

Auckland Avg price 875k 1065k 17.8% fall required

ex AKL nat avg was 525k 715k 26.5% fall required

Regions are proving sticky but they will move.....

It won’t necessarily “all depend on interest rates” - we could see rates falling quickly due to some very bad economic reasons and house prices continue to slide with it. Lagging effects of higher rates would also continue to show up in the wider economy for months after rates drop.

Of course :) I'm a self confessed novice. What's your point? Unlike your good self, I'm not puffed up to the gills with self importance. Readers can take my forecasts with a grain of salt. I am an underling in the masses. I have done well financially. Your 2017 forecast of an imminent Great Depression was not a winning forecast either.

Cowardly? I was absent with work commitments! It seems TTP is still grieving my past absence and you've got an axe to grind) too🪓

RP you ask "what's your point?" I can only copy and past my previous post; "you forecasting house prices to fall in 2016, 2017, 2018, 2019, 2020 was not a winning forecast", in reply to you saying "But-but, house prices are falling - forecasting this was entirely correct." That's my point.

Considering First Home Buyers potentially sign up to a 25-year mortgage and fork out hundreds of thousands in interest, waiting five years (based on mine and other’s forecasts) save heaps in interest/earning heaps in interest with a backdrop of falling house prices is proving prudent. You're on record as forecasting 2024 as being worse than 2023 - right?

Home ownership should be a life changing experience for all the right reasons. If it's meant to be more yours and less so the bank, it will be with time, patience and unwavering determination (not speculation).

Any young person with an inch of economic/financial knowledge knows buying a house is financial suicide in NZ at current going prices.

Houses in some small towns are still very high, Taupo for instance, 700k for a hole in the worst streets in the town with multiple gangs on the same street.

We still have a long way to fall before the current gen of FHB will "get on the ladder".

Getting on the ladder sounds like joining a pyramid or ponzi like scheme.

The banks credit criteria and stress test at 8.25% is a free market form of DTI. In many ways the banks already implement a framework around affordability due to CCC. They have complex rules around the % of different income streams you can count etc etc.

At the moment its hard for first home buyers to get credit hence offers are lower, vendors do not seem to have all worked this out.

Triple C is the banking acronym for the Credit Contracts and Consumer Finance Act. It makes directors of lending institutions personally liable for large fines if their organisation has not adequately accessed a borrowers ability to reasonably meet repayments. It's been tweaked a bit by Labour since introduction. Its why borrowers now need to submit months of bank statements so the bank can look for Netflix / Uber Eats etc and other totally unreasonable ways to spend your personal money.....

Yes, the banks should be enforcing credit standards not the central banks. The problem is that bank management behaves with a very short term perspective (get the big bucks before the music stops) and then bank shareholders have the incentive to exercise a call option given the "too big to fail" idea. The solution I think is to enforce higher capital requirements on banks (as the RBNZ is in the process of doing, albeit crudely) based on those lending standards and let the banks decide how best to allocate lending.

People will have you believe that it's the borrowers that should be assessing the credit standards. They should know that interest rates couldn't stay low forever and shouldn't have taken out massive mortgages.

Don't blame the bank for dropping the test rate to 5.8% last year, considerably less than current mortgage rates. The borrower should have graduated with a degree in finance and made a qualified assessment. It seems only in the lending space does the customer have to wear a loss due to poor risk assessments.

Because the speculators are holding out for 2021 price while their 2% mortgages hold. Greed greed and more greed. It's not that people dont want to buy....they just cant make it stack.

How many are rolling to 6-7% this year again....oh yeah, most of them. #nosale #nocomission.

RBNZ Mortgage Data has the average number of new mortgage commitments at 7035 per month for 2020-2021. The majority of those were fixed for 1 or 2 years.

Biggest months were Nov 20 9289, Dec 20 9652, Mar 21 10487, Nov 21 9084.

The decisions those borrowers made on fixed rate terms are going to be impacting right now. Either way a lot of people got kicked hard in Nov, Dec 22. They probably went into denial mode until after Christmas/New Year. But now it starts to hurt. They will soon be getting their monthly credit card bill and may find they don't have the funds available to clear the full balance as they usually do. Because the interest rate increase has eaten their savings. That is the start of the spiral. Now they are carrying 20% credit card balance debt and higher interest mortgage debt.

FOMO to FONGO turns on a dime.

Indeed. The hazard warning buzzer has been sounding loudly for over 12 months. Perhaps greed causes financial deafness.

Rates are higher now that in 2016 before central banks lost their minds by plunging rates globally. Inflation has been outpacing pay rises for some time, mopping up any remaining discretionary spending from potential buyers. Banks Directors are now on the hook personally for lending more than people can afford.

Do the math.

Looking at the past 5 years, investors have been setting the price by bidding up homes that typically are in the First House Buyer space. At the moment they are not active and the market is falling month by month.

I think the biggest price movements will occur once these investors start becoming net sellers.

Unlike FHBers who mainly sell if they are trading up, these investors will be selling to prevent losses overwhelming them.

They will be more motivated to meet the market than a single home owner who still need accomodation.

The two most likely buyers for these sales will be FHBers, and .... smarter investors. I think smarter investors are going to wait until a house beats term deposit rates.

Here's the data. That's an awful lot of investors borrowing up large, especially when you consider they often require a 40% deposit. Any guesses where the deposit comes from? I wonder if C31 incorporates equity leverage in the "New Borrower" figures.

C31 New Investor Lending:

- 2015 - 65,419 borrowers, average $335k, avg 104% of FHB

- 2016 - 62,832 borrowers, average $342k, avg 91% of FHB amounts

- 2017 - 41,032 borrowers, average $331k, avg 86% of FHB amounts

- 2018 - 40,605 borrowers, average $341k, avg 87% of FHB amounts

- 2019 - 36,371 borrowers, average $350k, avg 85% of FHB amounts

- 2020 - 42,347 borrowers, average $400k, avg 85% of FHB amounts

- 2021 - 37,736 borrowers, average $494k, avg 90% of FHB amounts.

- 2022 - 20,499 borrowers, average $526k, avg 92% of FHB amounts.

The only option to buying into a falling market, is buying rising one, which is hard work.10% building cost inflation means the eventual recovery will be strong, so now is a pretty good time to buy, if you don't rely on past sales to set pricing. If you decide what a property is worth to you, and ignore vendor expectations, you will have a more choice to buy well, compared to a sellers market.

Agree, it's been a sh*t show to buy property over the last few years... atleast you can now go to an open home without lines out the door, take your time with due diligence and have the ability to be able to negotiate on purchase price with vendors who are generally more realistic.

Low balling sellers is generally a waste of time. Pretty much you have to not be fussy about a house and put in a hundred offers until you get lucky. If you are at the other end of the spectrum like me it took a year to even find a decent place I was prepared to live in. You see places along the way you wouldn't want to buy at half the asking price.

You get the feeling more car and boat giveaway’s with house sale are coming, once house price’s are down 20% fear will set in a 20% is much better than waiting for a year and losing 40%. Most people who sold over last few years would have made huge profits but now is the time to give some off that back.

For the last 12 months capital values have fallen MUCH FASTER then your principal would have via repayment in Auckland. 2023 will be the same, if you wait and buy cheaper you well pay off the house at the same payment rate in 12-15 years.... thats even better HW2 people paying off massive mortgages are enslaved.

I've run the numbers a few times. It really depends on what's important to people i.e. family stability vs making money.

- Rent $500 per week

- Increases 5% p.a.

- After 15 years = $615k

- After 30 years = $1.84m paid

- $500k Mortgage, $917 per week @ 8% on 30 year loan term,

- Increase payments 5% per year

- Total interest = $404k, Total Loan $500k = $904k. Paid off in 15 years.

- $3k rates, $4k insurance increased at 5% p.a. = $200k in 15 years, $500k in 30 years

There are other considerations:

- Save or invest the difference of about $400pw. One will have saved $300k in 15 years, that is, if they have enough discipline. Investment returns on top of that? Probably another $100k. So financially it can make sense to rent rather than own.

- But if you have children and can't find a stable long term rental? "Sorry kids, we're moving again which means a new school, new friends etc. But don't you worry, Daddy is making bank".

The home owner nails the mortgage in 15 years, and the next 8 years doesn't pay $50k p.a. in rent = $400k.

2023 looking great for Investors/FHB's with long term horizons. Cost of new houses going up by the day and olders ones down. Will hopefully be lots of bargains as panickers bail Excellent for those who don't read or accept the naysayers continual rubbish.

After all who has ever gone broke buying property in NZ

https://www.interest.co.nz/property/74363/olly-newland-says-property-in… lots have but RE etc dont promote it.....be quick

GPH, young gens have no interest in putting themselves into 30–40-year mortgages to float boomers massive profitable retirements.

Younger gens know that there are not enough of us to keep the gold run going on property.

We can just keep importing people to grow our population but that too is pushing out more and more talented kiwis.

Go the boomers!... Unlike Gen xyz , we actually worked our ARSES of to earn our money, paid taxes, and the little feckers AKA kids, aka gen xyz get the benefit of our hard work vin our wills!

The boomers saved NZ and are propping up the economy right now.

Spend hard and enjoy boomers and 🖕 to the useless self entitled youth

Plenty i know have bought or are wanting to buy. Many are returning professionals or skilled immigrants whose number will only increase once Labour is gone.

The thought of all that wasted rent for no asset in the end deters most rational people .Perhaps the naysayers are just not rational and anyways ill be buying this year. I suppose that's why they call it a market willing seller meets willing buyer

Your joking right GPH??? Or just massively out of touch, or living fulltime at the Antarctic Scott Base?

You will see the crying on NZ TV/papers/property investors websites/ER recovery rooms, NOW and much, much more soon, with thousands unable to pay the new resets to 6.5++% new 1 year rates they will see as they roll off the mega mortgage written with the emergency teaser rates if 2.6%.

NZ is much worse than the predatory ARM mortgages that that the banks dreamed up to extend the USA housing ponzi (much like the new 30year plus plus NZ mortgages the NZ bank are creating now!!) leading upto the 2008 housing crash. This all conspired to take down the entire US economy.

Don't you know anyone that went completely bust and economically untouchable/tits-up, after the 2008 economic/housing boom/bust ???

I do.

The speculative runup to 2022 was steeper and more epic in it excesses and bad, bad loan formation. This deleveraging will be equally as epic and sadly many will likewise go bust - absolutely.

NZ Prices for many materials is out of control and housing is still out of reach for most and excessively expensive by every metric. DONT BUYNOW! imho.

The Crash is playing out right now, much faster than Irelands 60% cliff jump (a likewise analogue to NZ, in many ways) and another 20 to 30% falls are coming as interest rates will be written in the 7 to 8+% range this year - its practically guaranteed.

This crash will reset all prices much lower and then and only then - a time to buy will emerge!

No jokes this end , how many have you got to sell cos im likely to be a buyer at the other end of your doom and gloom scenario. Those who sold after GFC in 08 must rue their decision everyday whilst those who bought are in clover as usual .Its people like you who i hope are given as much air time as possible on this subject. Remember that economist Shamabeel someone who has been going on for years about how irrational the NZ housing market is and how would would always rent as a crash was imminent . It would seem he was wrong on this matter , your not him are you?

Great news 🤑🤑

sold property's at market high✅

inflation up✅

Mortgage interest rates up✅

government dept hugely up✅

RB saying recession ✅

COL out of control✅

economy fecked✅

over supply of houses✅

low demand✅

beautiful... Just waiting for the inevitable crash and boon💥 buy buy buy .. to easy🤙🖕

great.. thanks Jacinda...

Labours lateness for the building of " affordable housing" has yet to overload the housing supply .

We are seeing it all over NZ... New builds for Africa! .... At the same time TM listings hitting new highs and demand plummeting!

Once again. labour feck's the market.

Supply is huge - demand is weak = CRASH!

Sell now and hold until April and boom 💥 cheap housing,, recession, Ardern gone by lunchtime...

You heard it here first 🥂🤙

Hot of the WWW. .

Reuters latest article...

World recession 2023.. ..

https://www.reuters.com/markets/world-bank-warns-global-economy-could-e…

We welcome your comments below. If you are not already registered, please register to comment.

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.