The economic changes that have swept over New Zealand in the last three years have been an unmitigated disaster for aspiring first home buyers.

While economists and other pundits will no doubt debate the merits or otherwise of our recent monetary policies for years to come, their effect on aspiring first home buyers has been disastrous.

Interest.co.nz's Home Loan Affordability Reports have been tracking the main measures of housing affordability for first home buyers on a month-by-month basis since 2004 and these clearly show that first home buyers are worse off now than they were three years ago.

And they are not just slightly worse off, their chances of buying a home of their own in September 2022 were substantially lower than they were in September 2019.

One of the biggest drivers of that change has been mortgage interest rates.

Interest rates aren't the only driver of the property market, but they are one of the most important because most property transactions are highly leveraged. So changes to interest rates, whether up or down, have an almost immediate impact on borrowing levels and prices.

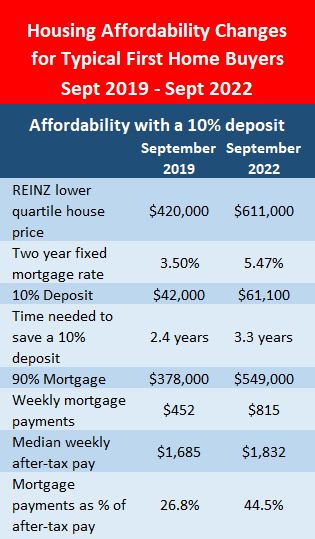

In September 2019 the average two year fixed mortgage rate charged by the major banks was 3.50%.

Over the following 20 months the Reserve Bank pushed down interest rates until the average two year fixed rate hit a record low of 2.52% in May 2021.

From there interest rates have risen precipitously and the average two year fixed rate reached 5.47% in September this year. And it's likely to be onwards and upwards from there.

So what effect did that have on house prices?

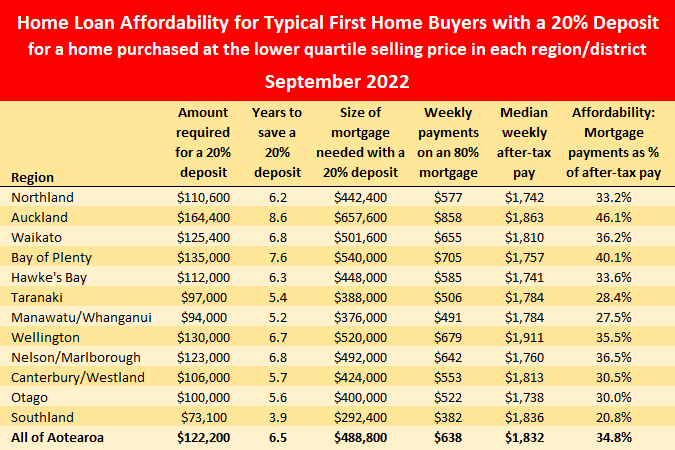

Because first home buyers usually buy homes at the lower-priced end of the housing market, the Home Loan Affordability Report tracks the Real Estate Institute of New Zealand's lower quartile selling price.

That's the price point at which 25% of the properties sold each month are below and 75% are above, representing the bottom end of the market.

In September 2019 the national lower quartile price was $420,000, but falling mortgage rates fed a wave of irrational exuberance that washed over the housing market until the national lower quartile price peaked at $670,000 in November 2021.

Since then, rising interest rates have pushed the lower quartile price back down to $611,000 in September this year, but that's still up by $191,000 (+45%) compared to three years ago.

That means that in September 2019, a 10% deposit for a home purchased at the lower quartile price would have required $42,000.

By September 2022 that had increased to $61,100.

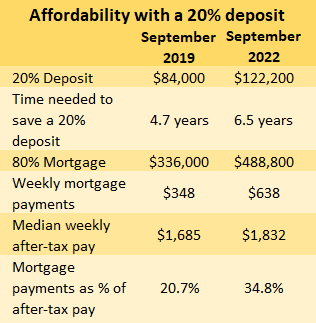

A 20% deposit on the same property would have increased from $84,000 to $122,200 over the same period.

Of course that means the amount of mortgage debt the first home buyer would have needed to take on to complete the transaction would have increased from $378,000 in September 2019 to $549,000 in September 2022 (with a10% deposit), or from $336,000 to $488,800 with a 20% deposit.

That combined with higher interest rates increased the amount of money they would need to set aside each week for the corresponding mortgage payments from $452 to $816 (+80.5%) with a 10% deposit, or from $348 to $638 (+83.3%) with a 20% deposit.

That wouldn't be so bad if incomes had kept pace with such a massive increase in costs, but of course they haven't.

The Home Loan Affordability Report tracks the estimated, combined, median after-tax pay for couples aged 25-29, if both are working full time.

In September 2019 such a couple would have been taking home $1685 a week between them and by September 2022 that would have increased to $1832 a week, up by $147 a week (+8.7%).

That pales by comparison to the extra $364 a week they would need to set aside for mortgage payments (with a 10% deposit), or the extra $290 a week they would need to find if they had a 20% deposit.

Another way of looking at those figures is that in September 2019, mortgage payments on a lower quartile home bought with a 10% deposit would have eaten up 26.8% of the take home pay of a typical first home buying couple.

By September 2022 that figure had risen to 44.5%.

If they had a 20% deposit, mortgage payments as a percentage of income would have risen from 20.7% to 34.8% over the same period.

So however you look at the numbers, the position of first home buyers has worsened considerably over the last three years.

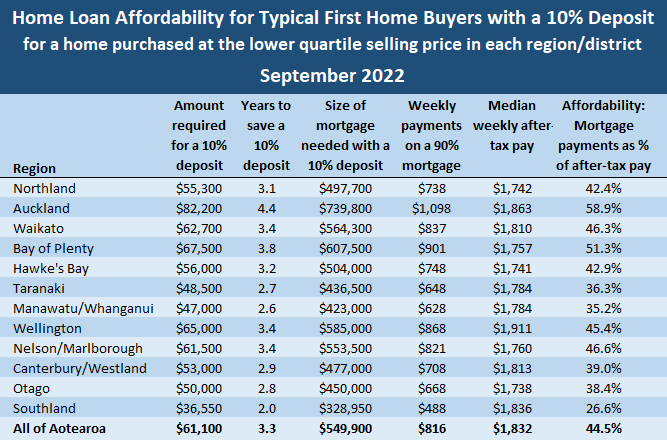

What's even more worrying is that all of the figures quoted above are national figures.

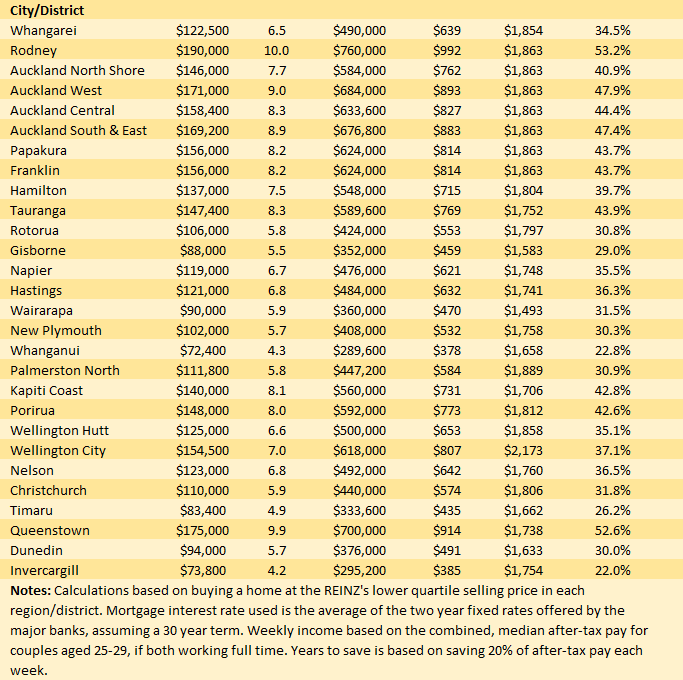

The position of first home buyers in higher priced regions such as Auckland, Waikato, Bay of Plenty, Wellington and Nelson/Marlborough is even more precarious.

For example in Auckland the mortgage payments on a lower quartile-priced home purchased with a 10% deposit ($82,000) would eat up 58.9% of the median take home pay for 25-29 year olds.

That is not just making buying a home difficult, it is putting it will beyond the reach of people on average wages.

In Auckland, and to a significant degree in regions such as Waikato, Bay of Plenty and Wellington, home ownership is increasingly the preserve of the highly paid.

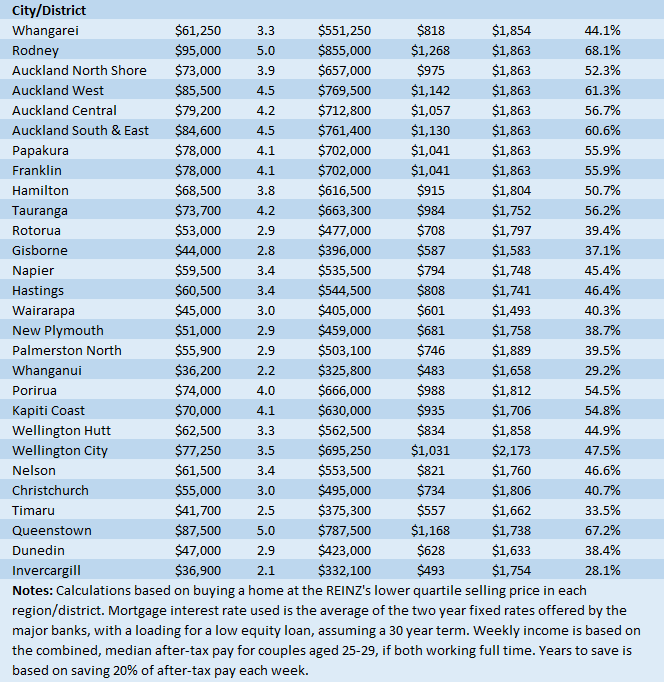

The three sets of tables below show the change in the main national affordability measures between September 2019 and September 2022, the main affordability measures assuming a 10% deposit in all of the main urban districts throughout the country as at September 2022, and the same measures assuming a 20% deposit.

The comment stream on this article is now closed.

*This article was first published in our email for paying subscribers on Friday morning. See here for more details and how to subscribe.

234 Comments

If only we could turn the clock back 5 or 6 years and give first-home buyers a decent bite at the cherry...... 🍒😊

TTP

Crocodile tears from a real estate agent.

Auw,it is so sad to think of all the money that vampire squids and house hoarders are losing every day now, in an illiquid market. I bet the palmy penthouse market is drier than the Sahara right now. 🐊💧

RED FLAG 🚩 Doom Goblins operating above and below.

TTP

I'll buy your penthouse. Give you ten bucks for it.

Very immature comment

I agree, about time Tim stops s**t talking...

The Doom Goblin thing is getting boring now TTP. At least try and get creative with your obnoxious insults and narcissism

Values have dropped since my last post.

I'll give you 9 bucks for your penthouse TTP.

Better be quick! There is another US Fed rate review next week.

Fitzgerald, Tim↘️ won't fall for it. He's just as smart as HW2 🤕

by tothepoint | 17th Aug 21, 11:48am

“It's likely that interest rates have less impact on the housing market than many people here believe”

by tothepoint | 7th Dec 21, 12:27pm

“When inventory goes up, prices go up”

Be quick folks – FOMO is imminent!

So Buffets often repeated quote "interest rates are to assets what gravity is to matter" is wrong then. As rates have risen in the last 12 months, nothing has happened to the NZ ponzi. Tui.

Who to believe, TTP or arguably the worlds greatest investor...

First-home buyers remain as keen as mustard to get into a home of their own - despite rising interest rates......

The real problem is the shortage of houses in NZ - a problem that stems back well over a decade. (But you already knew that.)

TTP

The real problem is a glut of over-priced houses in NZ. A problem that stems well over a decade. Did you know that? (rhetorical question)

Rising interest rates are fast turning this closing day of greed into a nightmare for many.

Surely you’ve noticed all the publicity about top-tier houses still setting new price records...... Thus, there’s also a shortage of houses for the rich and wealthy - not just for lower income people. Plain and simple.

Poppy - it appears you’ve got your head stuck down the potty. 🚽

TTP

Tim↘️ are you suggesting that if FHB can't afford an entry level house they can always buy a "top tier" one lol!

Thats about the depth of your knowledge of not just the housing market, but FHB's financials and wellbeing 😳

Read the article above properly. The housing market is not as healthy as you would like others to believe!

Reverend Retired-Poppy. Imagine if the OCR was 14% ?. Some would suggest the Taylor Rule is needed to fight our inflation problem.

"We want 2%, we have 8.8%. Half the difference is 3.4. The OCR should be around 14%."

Imagine what the Retail Rates would be ? Even higher than what The Prophet is saying for next year. Or is The Prophet just warming us up ?

https://www.stuff.co.nz/opinion/300718332/damien-grant-reserve-bank-isn…

10% Interest Rates Next Year, Guaranteed !

Why 2% inflation? It should be zero. But the financial sector (FIRE) would be screwed.

The only shortage here is cheap credit and low interest rates.

Good luck with that.

They will come, but as a bailout... most won't understand that and leverage all they can, and the cycle continues... for now

Yep, no excess stock on trade me……oh no wait

Interesting you say this. I just went to check trade me stock on North Shore compared to what it was when I was buying in late 2018-2019. (I made excel sheet every month). And the number of houses for sale is actually less for this time of the year 1357 OCT 2022 vs 1540 OCT 2019. Did not expect that tbh.

Give it time. Very few people NEED to sell yet, and most homeowners don't want to sell in a falling market unless the house they want to buy has also come down in price. It will be 12 months before listed asking prices reflect the real market.

And on a positive note, property prices continue to decline

Classy, seeing as you posted this before anyone else had. 🤡

Is it " Doom Goblinary " to speak the truth : that rising interest rates are kryptonite to asset prices ...

... and that , the OCR isn't within a bull's roar of where it will need to be to bring inflation down to the 1-3 % target zone ...

This time isn't different , debt levels do matter , house prices are still defying gravity ...

Turn the clock back five or six years? It was about that time that Mr Twyford was often present, loud & clear, with promises aplenty to solve the then housing crisis. Where oh where is Mr Twyford when you need him?

Our Minister of Disarmament & Arms Control , one Philip Stoner Twyford is constructively engaged in sending angry letters to Vladamir Putin ...there's no time for anything else ...we gotta keep the missives flying towards those very naughty Russians ... let them know , we mean business , we are peeved ! ...

Angry letters, the Wayne Brown approach to fixing stuff. Hopefully Twyford is also following suit and knocking off at 3pm for his nap, especially as he's earning even less than the paltry 300K Wayne is getting.

Twyford is getting $ 288 000 p.a. ... not bad dosh , for doing sweet bugger all ...

... by comparison , new mayor Wayne Brown ain't getting much more than that for a far more complex & challenging job ...

Fair enough, but Wayne is part-time so pro-rata quite a bit more

It won’t be long house price’s are tumbling will soon be back to 2016 levels and who knows might just keep going back in time.

Ohhh, does that mean I'll be able to trade a nice house in Herne Bay for a worthless treaty?

Bahahaha

If only we could turn the clock back 5 or 6 years and give first-home buyers a decent bite at the cherry.\\

This stands true, no matter what year it is written

NZ is having its GFC moment - prices going back exactly 6 or 7 years so do not worry.

The darkest hour is just before dawn.

The bubble is bursting. Rates are rising, and Kaumata Orr has lost control of the waka.

Within the next year or two there will be thousands upon thousands of vampire squid landlords going bankrupt and being forced to sell into a cratering market.

Prices will absolutely crater from here.

The system has been stacked against first home buyers, but the system is failing. It is failing under the weight of its own corruption and stupidity. Stupidest of all was negative gearing... so many landlords are negatively geared that they will be falling like skittles now that rates are rising out of control.

First home buyers just need to be patient. Enjoy the fact that whatever rent is being squeezed out of you, the house that you rent is dropping in value by FAR more than the value of your rent. Every day the vampire squid's grip weakens.

NZs property price crash will be bigger than Ireland's crash.

Possibly needs to be printed and framed for posterity.

Pa1nters message to FHB is to "frame and hang those warnings"

WOW!

Yeah, so when people come home to their cube to consume whatever UBI-enabled pellets they're allowed to eat today, they can reflect and think "why the hell did anyone envisage in a time of economic decline, items of wealth would get transferred down the line all on their own".

It's like thinking your pay rises will actually beat inflation.

Certainly highlights we need to be having the Georgist discussion of LVT vs income tax.

Unless we look beyond taxing just Kiwi working folk they'll remain ripe for exploitation.

Big article in the Herald today about the many small business owners who will be exposed in the next year or two, given they use their mortgage as an ATM…

given they use their mortgage as an ATM…

Yes I agree, see it a lot. It's all good.....till it's not.

This is a real problem, but the banks encourage this. If you own a house and use it as security against your business OD and/or loans, you are probably in the 7 - 8% vicinity, for plebs like me who dont own a house, current OD rate is 11.1%, thats on 500k, plus they charge 500 bucks a month for OD "management"

It is like we dont want small business to succeed. Bet it all on the house... Until there is a major cultural shift in this backwater country, housing as shelter, not an investment class, we will continue to abjectly fail. The only way this will happen is through a good dose of massive fail of the current housing market.

Na bro Nu Zullind is different. Ya know, the All Blacks and something about number 8 wire!? Tick that Ford Ranger up on ya mortgage boi, and while you're at it, might as well add that boat you always wanted! To the moon, house prices to the moon forever! Yeeeow!

I have long pushed the idea that low interest rates were masking our affordability crisis, as was the shift to a 30 year mortgage by default (instead of 25). Yes, you can service the debt with interest rates at historic lows, but you're still paying 50% more for the deposit than what your parents' generation would have paid for the whole house.

Certain other users have would always reply this by insisting it's 'always been hard'. Now we have yet another stat to disprove their garbage, will they still cling onto it? It seems like never being wrong about property is something people regard as sacred to their identity. Imagine if that was the only thing you had to give your live meaning. What a bleak existence.

How this is not a threat to our financial stability I have no idea. It's time for resignations, both institutional and political.

By extraction, the question begs if our entire way of life hasnt been subsidised for decades by low interest rates. We went from making stuff to service sector and just borrowed to make up the slack.

If there's a solution, the time taken to achieve it will greatly surpass people's anticipation of how long that should take (i.e. it's way more than a couple of election cycles).

I'd go further than that - we're letting a country with several crucial retail finance differences to ours dictate terms. You can fix rates for far far longer in the US, likewise you get all sorts of tax write-downs at a personal level that we don't do and you have the final option of abandoning a house if you can't make repayments. The debt doesn't follow you, it's attached to the house.

So we have a much harsher retail lending environment, where the banks can't lose, and yet we've gone far harder on the basics like food and shelter and made life as difficult as humanly possible for ourselves, with none of the safety valves the US has demonstrated the proven need for.

We're not that bright, are we?

No it’s easy to buy a house, all you have to do is not eat avo on toast

TTP You can ignore the posts from Fitz. He is just another of retiring poppy's accounts that doesn't say anything of substance

Top of the morning to you, HW2.

TTP

Thanks very much. Do have a nice long weekend break

Just keep in mind over the long weekend the fact that the Auckland HPI is showing falls of close to $4,700 per week now.

And the NZ wide HPI is showing falls of around $1,700 per week.

So, depending on how many houses you've been hoarding, your wealth will be cratering away over the long weekend. Perhaps it might be time to put a few of those rentals on the market on Tuesday.

Aroha.

Oh my days this is hilarious! TTP and HW2 should get together and have a baby. Create the ultimate mega landlord. Destroy the pesky FHB forever!!

They already have : it's called Property Brokers

And that baby is getting smaller and smaller. Soon it will go back into the womb of darkness. Just like the Havelock North Property Brokers office.

This is good news. With Labour's changes to reduce investor's involvement in the market and first home buyers no longer being given hospital pass, financially crippling mortgages, house prices will continue to come down.

The spruikers can spruik as much as they want, with no access to credit FHBs cannot act on their FOMO narrative.

It is actually a Blessing in Disguise for the FHB !

The Lord works in Mysterious Ways.

Basically the only way to enable affordable home ownership is to undo the policy balance driven by entitlement mentality of getting rich by pushing up housing prices and passing massive debt to following generations.

Folk should be incentivised toward productive work, not rewarded for monopolising land unproductively. The brazen entitlement of leaders and voters over these last few decades needs to be undone.

What can't continue, won't.

Funny, if interest rates goes up, it is creating social unrest but was good when interest rate was been dropped to zero - money was being printed out of thin air and being distributed

https://fortune.com/2022/10/22/billionaire-investor-barry-sternlicht-je…

It certainly needs breaking if it produces entitled idiots like him. Capitalism has been broken for a long time, ever since governments decided they had to goose markets with intervention. A healthy ecosystem has to allow creative destruction or the whole land ends up covered in sterile radiata.

There's no such thing as perfect capitalism, so it can't be broken.

It's actually doing what it should, we were just told it'd make everyone prosperous that's the problem. Wealth will always consolidate.

It was always dishonest, trying to convince everyone that using policy to transfer wealth from wages for work to those who own assets would make everyone prosperous.

It just keeps getting harder for FHB's, it a shame that many getting confused and think the opposite.

I think you meant “easier” all they have to do is, nothing!

Just watch the FED and inflation, and let the market fall on it’s arse.

Save cash and keep your job, that is the task of FHB’s.

Save cash and keep your job, that is the task of FHB’s.

That's now way harder than before though.

Rubbish. It's all about perspective, a perspective the spruikers desperately don't want people to realise.

There is no more cheap credit, property prices are coming down in a very big way, if they can see past the now, there will be a much brighter tomorrow.

This task is much easier / better than being down 500K - 600K on that 1 Mil rot-box you bought during peak insanity.

I'll take the high interest rates and ever increasingly, capitualting house prices thanks.

Stay debt free.

Prices are increasing higher than wages. Money is getting more expensive and harder to borrow. Central banks are gunning for jobs.

Ergo, harder to save a deposit or hold onto a job now and in the short-medium term, than before 2020.

Your advice is good, but it rang more true before than today.

Yes, when the job losses start it will get biblical.

Losing a job debt free vs losing a job leveraged to the eyeballs is a VERY different scenario.

I know which camp I'd prefer to be in.

The difference here is patience.

Losing a job without a surplus to live off sucks regardless. At least if you had some equity you could either deplete that or liquidate it. Obviously being upside down in debt and losing a job is going to suck the most, for sure.

Pointless comment. We're talking about whether FHBs should get in the market now. No-one who gets in the market now is going to have any equity if they lose their job next year. Unless you mean negative equity, which is not good to have if you lose your job and are forced to sell.

Upside-down in debt = negative equity.

"The economic changes that have swept over New Zealand in the last three years have been an unmitigated disaster for aspiring first home buyers."

Labour tried and failed with KiwiBuild. COVID appeared and JA 's Government was quick to act. Cash made available and RBNZ opened the tap. House prices dipped and then jumped for the next two years, the likes I may never see again in my life time.

Owning a house is a right, to raise a family, a refuge from everyday work, amongst others.

Is any political party wanting to address this, count my vote.

Owning a house is a right, to raise a family, a refuge from everyday work, amongst others.

It's certainly still possible but not easy if young ones also want to exercise their rights to a useless degree, gap year, cars, phones, parties, Netflix, etc.

Its the govts job to provide stability and confidence not handouts. Handouts got us into this mess.

Handouts pushed house prices to where they are today.

It's a canard, the idea young aren't saving. An excuse to keep the status quo.

What's needed is to undo the policy mix of subsidies, tax privilege and artificial constraining of supply, and let property be a free market on more equitable terms with work. Welfarism for property has brought us to this point, and it needs to go.

Hi Tee,

Gareth Morgan’s TOP aimed to address the exact issues you outline…..

But scarcely anyone voted TOP.

TTP

It is house or family. Can't afford both.

Anyone having kids these days is simply not thinking ahead.

Incel67 has spoken.

Anyone growing lettuces these days is simply thinking a head .

The cause is the RBNZ. Would you prefer they weren’t independent and the government controlled them? Or do they need a new mandate and if so what?

It would be even better if they weren't incompetent.....

In the past they were reasonably competent ... but , Robbo selected Adrian and ... oh , you know the rest ... sigh ! ..

Independent - bwahahahaha, please, please, tell me another story!

Multi-unit developments were selling well, and buyers bought "off the plan". Today, buyers prefer a finished abode.

Buying houses that don't exist yet is a good way to spend a couple of years in a transitory state.

And if you've never done it before, you'll take the completion date you're given as being even remotely plausible, plan your life around it, and have a 95% chance of disappointment.

FHB's have a finite amount to spend, around 40% less than when interest rates were at an all time low. It's not the FHB's who have a problem it's the STFHB's (Sellers to FHB's) who have a problem.

That's right, nobody can force you to buy a house. But people can force you to sell one. I'd much rather be in the former position.

If no ones forced to buy a house

Then why are so many people pretty charged about house price.

People are nuts about house prices therefore you must buy one?

It's probably just a social media phenomenon. Like this site, hundreds of comments on daily articles about house prices makes it interesting, which draws more views, which encourages more articles, etc.

Well, it's a now decades old cultural norm around home ownership, probably coupled with the fact that no one working for jack all net benefit likes seeing people get wealthy, seemingly just by owning a house.

It certainly seems to generate the lion's share of traffic on this site, that's for sure. For all the talk about the "real" economy, those sorts of articles generate far less interest, when ironically you'd want them to attract way more than the 143rd article this month about what house prices and interest rates are doing today.

If you don’t want to read it, don’t.

As bad as complaining about the Kardashians. If you don’t want it in your life, Marie Kondo it.

Yeah but is it as bad as complaining about complaining about the Kardashians?

Just an observation about irony really.

As it has been said, for may in their 30's FHB it is the house or kids as you cannot afford both. For those who saved like hell for years and watched the prices spiral out of control, couldn't afford to buy when they calculated what it would cost to service a mortgage of 800k-1m if the interest rates got cranked up to....now. Now these people are left in limbo where they will benefit from waiting, but can't afford to progress their lives in having children before they sure up the house to secure a family home for the long term. I know many of these people and can tell you it isn't a nice position to be in, however it could be worse. You could have 10 properties and be haemorrhaging equity by the second

Alternative Headline: 'Harder for bridge jumpers to jump now that safety fence has been installed.'

Day five in your seminar for Property Spruiking. What did you learn to do?

Not to swim in the poppy intellect pool as it is extremely shallow

Wonderful! 🤔 You see yourself as a big clumsy fish then. Swimming in deeper waters with sharks like Tim is more your thing then 🐟

Lodge your tenants bonds NOW!

Chatting with my scaffolding crew, who see the building industry from inside. They tell of cray-cray prices for matchbox sized units, crammed onto tiny land parcels and subject to rafts of compliance and costs barrelling down the track:

- Full safety harness and anchor points if over 500mm from Gaia for tradies.

- 140mm framing and insulation boosts to higher R values imminent. 50% more timber...

- Double to triple glazing shifts imminent, 50% increase in weight for windows.

- Diesel costs have tripled so freight and just getting around are more costly.

Whereas a small kitset house, 100 squares, is still under 250k including foundations, on a level, 'Good ground' site.....

Oh yeah, scaffold requirements can double or triple the cost of getting certain items done. It's kinda difficult because you don't want to kill tradies, but then a competent one shouldn't need the level of scaffolding/health and safety that's being mandated from the top down.

The problem with kitset houses is often the size, and whether you have access to tradies familiar with whichever particular kitset you're using. They're actually usually more expensive per square meter to build than something onsite, and you're a bit limited in scope down the track if you ever wanted to increase it's size.

Of course, it's trade-offs all the way. But we are gonna haveta get used to Them.

And your comment re competent tradies is spot on. My scaff is up, and I put a roof anchor in mainly for me. When my roofer came Friday to measure up, he stepped all over the structure, purlin to rafter to purlin, no harness, no rope, holding his day book and tape to take and to record the measures.

Told me about a Sydney accident he witnessed. Tradie was anchored and harnessed, but still managed to fall off of a multi storey structure. Roof anchor pulled out, hit the unfortunate victim on the head after he hit the ground....Murphy rules....

Yeah so if I were offering someone wanting to build a house advice, it'd be source out a really competent builder (ideally not a housing company), and let them go to town. One experienced builder is going to churn out more work in a day than 3 relative newbies. 6, if they're not managed properly.

Finding that sort of builder is kinda rare these days though unfortunately. Hey, maybe that's contributing to the high cost of housing.

The 140 framing, double triple glazing are value-added items and will help future-proof the house, especially so when prices fall. Maybe not so much to enable the house to sell for more, but that it can be sold without a huge discount when other houses become more obsolete. And of course, there will be lower operating costs.

The real 'cray-cray' price is still what it costs to buy raw land and get to the development stage. Until we are willing to acknowledge the stupidity of how much we pay for the land, then I don't have much sympathy for any other non-value-added cost, because they are in effect a direct result of this non-acknowledgment of the land issue.

Fully agree. But affording the initial increment is the issue.

I wonder how much rates would actually go up if councils weren't front loading costs into development expenses.

That's really the nub of the whole article, ie that relationship between CAPEX and OPEX. In a more free stable market, they pay far less for housing and therefore are holding less housing debt and because they are stable, when interest rates rise, it has less effect.

Their LVR is less as there is not as much capital gain to offset the bank's risk, but the total $ deposit is less than in our jurisdiction because the price is that much less. Renters pay a higher yield as a % but still less in real $ terms. A higher yield is needed because there is very little capital gain.

This adjustment NZ is going through is the 'mid ground.' ie the worst of both worlds in that we are still paying too much, interest rates are going up, and the banks see the fall as an increasing risk to what they have lent and therefore are making it more difficult to buy.

This does not mean that we should revert to the old status quo as a solution, as it was that status quo that is now causing the present crash.

There is no jurisdiction in the world that has unwound a bubble without pain. The real effort should be not to put the economy in that position in the first place, or return it to that position but to enact change so it does not happen again. And we will be in a position to do that once we are at the bottom of this present fall.

Until then ......

140mm framing is an excellent idea. I built five years ago, and did the whole thing in 140mm timber. At the time, the framing and trusses were around 27000 (from memory) and the 140mm were about 35000-40000. The additional cost in timber is not that much, quite a bit of the cost is in the actual framing and trusses services.That was for a 300sqm home. So the change to the timber cost is not much and far outweighed by the far superior structure and insulation capability you get as a result. Houses built with 90mm timber feel very tinny to me these days. I think 140mm is quite normal overseas. We probably just use 90mm here because we build cheap shitty houses (even most of the new ones).

90mm is fine in an area that never goes sub zero. It the double glazing that makes most of the difference, 140mm and triple glazing is overkill, far better off spending money on a better roof. I have a single heatpump in a 175sq/m home it has no trouble keeping the place warm and I have a ton of glass. Yeah maybe if your in the South Island or places like Queenstown or Wanaka where it snows, then sure.

140mm framing on your average 3 story duplex in auckland soaks up quite a lot of liveable area. That hallway life just got squeezier.

House prices did rise rather exponentially in last few years plus the record low interest rates during covid era..

People should have realised that these interest rates at that level wouldn't last forever..

Home buyers should have locked in 5 year rate @ 2.99% in 2021 so most mortgage holders would have been safe for at least 5 years.

I do have a small mortgage @ 2.99% fixed till 2026 and Im getting 4.3% in term deposit now hence bank is paying my mortgage now...

I don't know why mortgage brokers always try and fix for 2 years only and always claw the customers back every 2 years...

After tax on your term deposit, you're currently at about break-even?

That will likely swing further in your favour in the short term.

But having the same foresight you had at 2.99% to lock in whatever term is left on any free cash-flow at, say 6%, is when it looks like there is 'more to come' (as it did, to go lower at 2.99% - that's why borrowers locked in for shorter terms) will be the test for you.

Deflation is almost upon us. It is yet to show its hand, fully. And when it does 2.99% might look expensive. Let's hope we;The RBNZ and Government have the sense to 'lock in the changes' when that happens and not let the property monster out of its cave again.

Of interest:

https://www.stuff.co.nz/business/property/300716236/how-i-saved-200000-…

Yep, the RBNZ and Government and learned their lesson, they will absolutely never juice the money supply in order prop up the economy, ever again.

They will probably say the same in 2026

Great piece. And makes a mockery of the widely quoted Demografia reports that measure affordability solely based on Debt To Income ratios.

Bet all the buyers from the start of the year who missed out because of the governments CCCFA are really peeved off.

Damn that nanny state.

Yawn not sure the DGM's would have a life if they couldn't get up at 6am on a Sunday morning and start commenting on a housing article. Fact remains unless you actually enter the market at some point and buy a house it really doesn't matter if you are right or you are wrong because having a rant from the sidelines forever gets you nowhere.

Fact remains if you enter the market at the peak of a housing bubble then you will go backwards some way before the bank inevitably kicks you out. This is already happening.

Yawn not sure the spruikers would have a life if they couldn’t commenting complaints about DGMs commenting on the very same forum.

It’s pretty clear that having an opinion of what is clearly happening in the economy is taboo. We only talk about positive house prices here in NZ! Anything else is banned.

Article states facts that are good news for FHB in coming years, labels that as a negative for whatever reason. Can’t blame the FHB for getting the feeling the whole thing is rigged.

The DGM's will always be DGM's they will never enter the market regardless. Some people will never be able to afford a house and just expect prices to fall back to 3x income level so they can, that's never going to happen.

Oh but it will, it will. Every landlord is leveraged up the arse and negatively geared, it's not like most of them have lots of equity overhead and income outside of rent to fund things. They shall all fall, then those with nothing will have it all!

99% falls and 30% interest rates, guaranteed! The Oracle has foreseen it, and it cannot be unseen.

The DGMs do contribute to the rental market in a way, by putting people off home ownership…etc. So they are kind of essential to a functional market.

Interestingly, Michael Reddell is wont to point out that 3X incomes does seem to be a pretty common resting point where policy is not used to keep prices artificially higher.

Problem in NZ is that housing has been turned into a welfare scheme for our older generations, rather than a free market with price discovery.

The back patters think that the only game in town is property, I'm sure many on here have other business's where they make money and invest in. Residential Property is a zero sum game for New Zealand as a whole. It increases unaffordability by competing with average buyers.

We want money coming in from overseas, not reduce disposable incomes of normal kiwis.

Look at more complex ways to make money not grab lowest hanging fruit. We want more companies that have a small footprint like Xero yet bring in millions. Plenty of online business's, and technology business's, out there. We need to setup infrastructure so these companies can get some traction.

Yes it is rigged.

But it was rigged by fools.

And they are unable to prevent its collapse.

Only 2 people commented before 7am.

The first person to comment was TTP. Is he a DGM?

Top comment Carlos, empty vessels make the most noise.

if it were an unmitigated disaster then you would think a FHB getting their first home would be almost unachievable,and yet the weekly payments on a 20% deposit is about what you would expect to pay in rent,in whangarei anyway.

Its been that way for years. Rents on the North Shore went way past what I was paying for the mortgage, my payments topped out a $630 a week the same house got rented a year or so ago for $830 a week.. House prices doubled every 10 years because many other things also doubled.

Double tick, very true

It’s always been that way? Really at todays bank rates and at todays prices it’s cheaper to buy. Pressing the BS buzzer on that one

2 bed apartment renting in Devonport for $640. Homes valuation $1.6M.

Show me the maths where buying is better than renting.

That tallies - currently paying about $460 in rent on a place that just changed hands for 1.1m. Most people who make the 'cheaper to buy' argument lack the basic economic literacy to factor in the opportunity cost of putting 20% down on a purchase too. They also fail to account for the fact that the opportunity cost also moves up with the risk free rate of return.

Its been that way for years. Rents on the North Shore went way past what I was paying for the mortgage, my payments topped out a $630 a week the same house got rented a year or so ago for $830 a week.. House prices doubled every 10 years because many other things also doubled.

As is the way with credit-driven property bubbles, repayments increase. The argument that "house prices double every 10 years because other prices double" is social media / Granny Herald reasoning. Doesn't add anything to the understanding of the sheeple. If you looked at increases in the money supply and credit creation, you can find more meaningful relationships. Interestingly, household debt to GDP has taken 20 years to double. But if you start from the early 1990s, h'hold debt to GDP roughly increases every 10 years. Conicidence? Good luck expecting the sheeple being able to borrow like drunken sailors going forward.

The big boys want to sell you things and if you don't have the money, they're going to lend it to you.

Why would you think that'll stop now?

The big boys want to sell you things and if you don't have the money, they're going to lend it to you.

Why would you think that'll stop now?

Because the currency will become worthless and the financial system will become increasingly unstable (which in many ways is bankrupt now). If you're not aware because these matters haven't been reported by Granny Herald or announced at the water cooler exchanges, you will likely be ill equipped to protect yourself accordingly.

Because the currency will become worthless and the financial system will become increasingly unstable (which in many ways is bankrupt now).

Those are possible consequences, although they existed and were known of since the early days of currency creation. So the question begs, why's now any different, and why do you think the authorities would stop?

Aside from the debt being higher than ever (which is always going to be the case), I haven't picked up at the water cooler or herald or wherever that governments and central banks world over have declared money printing abolished.

Those are possible consequences, although they existed and were known of since the early days of currency creation. So the question begs, why's now any different, and why do you think the authorities would stop?

More than happy to listen to the 'house prices double every 10 yrs' ideas if they're actually put it into a robust explanation or data-based model. Talking about this idea like it's a religious prophecy should be treated with the scorn it deserves.

Your responses don't make sense. Who's saying house prices will double? Why couldn't house price inflation slow down? Why does money have to become worthless?

Who's saying house prices will double?

The media and the people who either believe or promote the urban myth.

Why couldn't house price inflation slow down?

Happening now.

Why does money have to become worthless?

Because increasing the money supply results in inflation and destroys the currency as a store of value and its purchasing power.

No one in this thread is saying that house prices will double soon. Money is always reducing in value but it doesn't become "worthless" unless you mean worth less? It seems you have an issue with Pa1nter who I'd rate as one of the more sensible and grounded commenters here.

No one in this thread is saying that house prices will double soon. Money is always reducing in value but it doesn't become "worthless" unless you mean worth less? It seems you have an issue with Pa1nter who I'd rate as one of the more sensible and grounded commenters here.

You can believe whatever you want and believe in the ideas of whoever you want. Just because my beliefs are different is irrelevant. But it is the foundation of how forums work and debate.

Currency can become worthless when it's no longer legal tender, But that's only as a means of exchange. It may have worth to someone; for ex, a collector. Because a currency is less purch power and diminished store of value, it doesn't necessarily make it worthless.

Everyone is free for sure, but when you keep claiming public ignorance and using the word "sheeple", then never really providing great counter arguments, it's hard to work out who the shepherd actually is.

If your argument for why bitcoin/crypto has a future largely rests on 5-6 years of price increases up till 2020, then decades of longitudinal data for housing prices should be more than enough evidence for you.

Sheeple is just a metaphor for what people tend to believe based on what they are told. Is it ignorance? Maybe, but not necessarily.

If you have an argument for the "doubles every 10-year" theory, I am more than open to understanding how and why it is. Showing a 20-year period where prices increase 200% is not "proof" of some universal phenomenon that "house prices double every 10 years."

That wasn't actually my claim, although we can see that doubling going on for nearly half a century. It certainly looks like a trend, although I wouldn't say it's an unbreakable law.

Change some or many of the underlying economics, and that trend could change for sure, you were asserting that money lending as we know it is over, that'd probably have an influence. Your evidence for that rests almost entirely on your perceived negative consequences. What is to say central banks won't make lending favourable again (either by dropping rates, changing lending criteria, or both) once there's an economic crash, and they want to give things a little push?

That wasn't actually my claim, although we can see that doubling going on for nearly half a century. It certainly looks like a trend, although I wouldn't say it's an unbreakable law.

What data set do you use? Data shows that h'hold debt to GDP in NZ has increased from 20% to almost 100% since the early 90s. Does that mean that there is possibly a relationship between credit creation and the 10-yeat theory? What does that tell us about the broad money supply?

https://tradingeconomics.com/new-zealand/households-debt-to-gdp#:~:text….

Money has always been worthless but for our belief that it has value, and we've since replaced money with debt. Inflation, whether it be of assets or consumables erodes the value of money. Somehow we believe that if we get more tokens for something we've received more worth/value.

Money has always been worthless ....

Okaaay

I don't know, saying that money is worthless just comes across as unhinged. Sure, it's a really bad investment, unlike property which could double in price in ten years. Money will not do that.

I don't know, saying that money is worthless just comes across as unhinged. Sure, it's a really bad investment, unlike property which could double in price in ten years. Money will not do that.

Depends. The gold price has increased 0.8x in the past 10 years relative to NZD. Some people consider that gold is money.

Haha the item purchased has worth according to your perspective, whether it be an intrinsic or extrinsic value. Or it pays taxes which at one point could be paid in other forms. The medium of exchange only has value based on belief. We currently use pretty pieces of paper. Before that it was pretty rocks. Before that it was labour. Before that it was wheat.

We must all be a little unhinged thinking that doubling the price of property provides a net benefit to society or the economy. Which, by the way should be one and the same but seem to be distinctly separate... that's a little unhinged. It's also a little unhinged that we're obsessed with the housing market but not so much with the food market, the clothing market, the education market, the health market etc, all the other necessities for human wellbeing.

These unhinged people who think house prices doubling every 10 years is a good thing are probably the first in line to have a gripe at the price of petrol.

Money has always been worthless but for our belief that it has value, and we've since replaced money with debt. Inflation, whether it be of assets or consumables erodes the value of money. Somehow we believe that if we get more tokens for something we've received more worth/value.

Fiat money is essentially based around debt obligations. And you're correct in that higher prices of objects doesn't necessarily mean higher value.

Let's fix this

Sounds hard. Can someone else fix it, and we'll just show up?

Wayne Brown?

... he will have it sorted by 3 p.m. Tuesday ... then , head off for his afternoon nap ...

You can see why demand and prices went up, $348 would have been way cheaper than rent, a bit of a no brainer to buy then.

House prices are still adjusting to market rates.

It's on pretty much everywhere.

Secret RBA modelling shows 20pc drop in house prices.

https://www.afr.com/policy/economy/secret-rba-modelling-shows-20pc-drop…

Home buyer demand collapses to below 2019 levels as mortgage rates soar.

https://www.telegraph.co.uk/property/buy/home-buyer-demand-collapses-20…

China on Monday suddenly delayed the release of its economic data—including September housing sales—that was scheduled for this week. But there is little doubt that the property market is still in a dire shape.

https://www.wsj.com/articles/in-chinas-property-sector-there-is-nowhere…

And just for fun:

Reserve Bank isn't really serious about tackling inflation. The bank continues to run an expansionary monetary policy, which is why inflation isn’t falling.The OCR should be around 14%.

https://www.stuff.co.nz/opinion/300718332/damien-grant-reserve-bank-isn…

10% Interest Rates Next Year, Guaranteed !

Good piece by Damian and his 14% is likely to be far closer to what the OCR should be if Kaumatua Orr were interested in price stability. The irony is that if the credit creation had been directed towards productive activity, then inflation would have been lower. But it's largely been thrown at the bubble and consumption.

It is clear that the current OCR is extremely low and extremely stimulatory. Given Orr's incompetence, it is also clear that he will not act decisively to redress this situation. This simply means that inflation will stay above the target band for the next few years, which will force the RBNZ to ultimately raise the OCR to a level close to 6% (or higher), and keep it at that level (or close to it) for the foreseeable future, at least for the next 5 years.

I until recently thought that an OCR peak of 5% was the central scenario, but I am now convinced that the peak will reach 6%, very possibly higher than that.

So however you look at the numbers, the position of first home buyers has worsened considerably over the last three years

Yet, when people like me advised FHBs to buy 3 years ago, people with no experience in owning a house, were making fun of us.

The problem is, Yvil, that it’s easier said than done. Even 3 years ago house prices were extremely high in this country relative to incomes. Not easy getting a 150k+ deposit together.

It's quite incredible isn't it? How we went from houses being 3 x the average wage, to the deposit being more or less 3 x the average wage.

Once upon a time you could save the equivalent of 3 years wages, with term deposit rates in the double digits, and buy the house outright. Now you need to save 3 years wages, with term deposit rates up until recently practically at zero.

There are many, many compounded reasons for that change nzdan. Did you ever gloat about the multi-bagger profit you made on your first-home? Yes! By the same standard why do you lament that others did likewise

Whether I gloated or not, does it make my comment wrong? I made many sacrifices to make that "multi-bagger profit", which I wouldn't have done if the market had remained sane. E.g. upping sticks to a new town, 4 hour/day commutes for the first 5 years, first 6 months of that confined to a single bedroom with a newborn, who today only sees her grandparents by video call/if lucky once a year in person. All for a house that was 3 x my salary.

Good news is my "multi-bagger" equity has halved in the last 6 months.

Looking at when a FHB should buy is not really just about when affordability is best.

Its about the peak and troughs of the prices (and direction of interest rates). If the trough is in 3 years and price is 20% lower than 3 years ago. Then that is the time to buy - banks will have deals to lend and the monthly payments will drop as the boom starts again.

Probably they will save $100-200k on their loan that way and not have to work for 5 years of their life to pay it off. Plus will not be starting in a period of financial uncertainty.

Telling people to buy after 7 years of upward economic trajectory is adding risk and stress

But during that time they are paying rent and helping someone else pay off their mortgage. The cost of building a house is still going up in price, and we have a lot of inflation, so even if house prices froze, they would be dropping relative to inflation. Timing the housing market IMO is like gambling.

It's easy to time, just wait for long long plateau and mortgage rates stabilizing along with inflation. It doesn't bounce like a basket ball.

Most likely see few distressed sales and buyers able to negotiate sensible prices. Why lose thousands of unnecessary dollars. FOMO is gone let's hope it stays away. It was and is completely irrational or insane.

Why even read an investment website, if you do not believe that markets can be timed?

Successful timing of the markets is at the very heart of successful investing. Do you also think that it is gambling to try to time the share market?

And because the housing market is relatively slow.moving, with lots of data available, it ought to be easier to time than most markets.

Here in NZ, it is the irrational and unpredictable interventions by the govt and RBNZ that have made the market tricky to time... who would have predicted the lvr removal and mortgage holidays, right at the peak, for example.

But yes the housing market can be timed just like any other. And the stakes are high. The rewards are high. And so are the risks for the highly leveraged.

Reading through the many comments, not much has changed over the years. There are a few commenters who take charge of their lives and make things happen and then there is the vast majority, typically the posts with the most likes, who just whinge and complain, often using sarcasm and ridicule others.

Yvil, you're one of the key ingredience that makes this public forum what it is. Now you're a critic of how it tastes😁

How precious...

"ingredience"

Notice, the one who spell-checks, he (it) cannot actually spell

F-wit

Funny, Yvil👍👍 was just commenting above about commentors like you 🤡..who offer little substance.

Your ego will survive.

... reckon we've just created a new word : " ingreviance " ... posters who're intolerant of other's views on interest.co.nz ... pissed off at their attitudes or spellin ....

Ingreviance !

HW2, the only reason that you are calling Retired Poppy names is that your ego is bruised, and you are worried about cratering house prices.

Falling fast now. Have you checked yet how much money you've lost? Going to see a real.estate agent on Tuesday, perhaps?

This property price crash will be epic. So many undeserved, parasitic fortunes will be lost.

Calling people names on social media won't stop the money bleed. Only selling will stop the losses.

🧛♂️🦑

Mate have you heard the ancient story of the ant and the man.

The ants were sitting around discussing and wondering about men and their world. As they sought to understand life on a higher scale.

(The point being that it was well beyond their capability)

At that moment an anteater walked by and did what anteaters do.

In this case we are probably all ants awaiting our fate

Fitz, I think it is you who is cynical and who is trying your best to hurt others with your comments. You probably think you are subtle about it, you're not.

Haha sounds like someone is whinging and complaining about not getting enough likes.

Tell ya what, I'll send you a medal, a winners trophy for taking charge of your life.

#voteforevil👍

Not sure what you mean. The content shows that marginal buyers are potentially in a worse situation when the bubble is relying on them to participate in what is potentially one of the biggest sh*tshows in modern economic history. In terms of economic management by the ruling elite, there is arguably good reason for complaints.

No you don't understand what I mean. There has always been and there will always be reasons not to do something. What differentiates where people end up in life, is not the circumstances, it's what people do about their own lives.

Really… a taste of reality will tell you different… there are plenty of circumstances that are not in one’s control and are the major cause of ‘where one ends up

Life can definitely deal people shit sandwiches.

One analogy I often refer back to, even on days I'm feeling sorry for myself, is that there's a lady who lives a few ks from me. Bad car accident, so she's paraplegic, after decades of walking. She has every reason to lie down and veg out. Instead, she's riding a bike using her hands every day, and still working.

Being a victim is a place most people put themselves.

Very well said Pa1nter !

No you don't understand what I mean.

Maybe you're being purposedly obtuse there Yvil. Part of a kind of troll repertoire.

Well said J.C.👍👍This is Yvil's😇 modus operadi. He/she is bored with life. This public forum represents people from all walks of life. Best we accept people for who they are and not judge. If Yvil😇 thinks he/she is a superior human😇 then the ground only hurts more when it hits. For starters, there are people who suffer from serious mental illness. They find basic everyday tasks, that we take for granted, like climbing Everest! Does Yvil think mental illness is a choice too?

We're all equal.

Definitely agree with that sentiment to a degree. But good luck / bad luck, good / bad timing etc etc can still play a big part in how life goes.

But I do agree that frame of mind and positive intent is a good place to start. It at least gives you a chance.

But I don’t think it is anywhere near as determinative as you suggest.

Yvil facts house prices are falling very quickly, rates are climbing, inflation high,NZD tanking, people have paid way over the top for property in NZ compared to wages, the bubble has burst and the downturn is going to be here for years we are just at the start, world problems everywhere. With all of this going on you should understand this housing market will be seriously affected and house price’s will see biggest falls ever, stop getting upset if you are over leveraged see a financial advisor get on top of debt before it to late.

"house prices are falling very quickly, rates are climbing, inflation high, NZD tanking"

Of course, but this has nothing to do with my post. What's your point?

I will definitely complain about unaffordable housing for average NZ. I am a kiwi that wants NZ to be a great place for all NZers not a few.

My business is setting up supply chains around world, and selling goods in many countries, buying property is easy and was helped by government. Property is low hanging fruit, and reduces disposable incomes of normal kiwis. It's not about me, NZ as a whole is better off as a country if Average NZers are enjoying life. It trickles down to crime and other social behaviors. Reduces financial stress in people's homes and helps parents bring up happy children.

So yeah I'm happy to be chucked in the unaffordable house whingers bracket. Will wear it like a badge of honor.

"The position of aspiring first home buyers has deteriorated substantially over the last three years"

Greg Ninness tell this to Jacinda Arden or Robertson and you will be termed as Liar.

Is it interest rates or interest rates on a mortgage which is over 1 million dollars. Pretty sure FHB would rather pay higher interest on lower priced house.

"Heres to the goodlife or so they say"...."On the other side of a coin theres a face"..."theres a memory somewhere that I cant erase" ('In a little while') , 'Uncle Kracker' song .

"Last year the ground floor apartment of challenge heroes Stacy and Adam, resold at the peak of the market for $2.1m, yielding the owners – former Block producer and television supremo Julie Christie and her daughter – a tidy $620,000 profit in two years. (nzherald , oneroof 24/10/22)

Welcome to 'The Block'...oops machine...(Pink Floyd)...lol , So if folk can profit from a rising market ,Why then does everyone throw their toys out when its a sinking market. Is it because everyone prefers to appear to be doing everyone else a favor and that in a rising market there are no losers? Or is it because everyone loathes a sinking market. Good to make $600k bad to loose $600k... My guess is folk want to be protected from losses but dont want to be restrained from gains... No surprises we have inflated values given the pump and dump some folk have been engaging in...problem now is the layman or sheeple as some prefer to call them have latched on to whats been going on....not sure the above nzh article does the industry any favors...I guess they couldnt help themselves... $620k is not bad money for others to aspire too in a short time period ,Are they hoping to reignite a smouldering heap or critically , have they shot themselves in the foot with this article given the current market and rising interest rates. Not sure newbie FHB's presently can afford to play in the big sandpit... but clearly the tv show has inspired many to climb up the ladder and its easy to point the finger at the RB for inflated values but let us not overlook the other components that made 'F.I.RE' burn so intensely .

The others components like negative gearing, high lvr lending to investors, nil cgt . Most of these thing have changed as well as raising interest rates.

Good piece on Australias housing madness, negative gearing :

Yep theres a very good reason why the RBA isnt hiking aggressively ....

Even if they do not hike aggressively, they will not be able to stop mortgage rates from rising in Aus.

The central banks have limited power. Inflation is in the driver's seat.

There are two wrong beliefs that I have observed above.

1. That interest rates doubling means that house prices will halve

2. That house prices (for social reasons) should not increase ... ever. Though everything else does.

The printing and availability of cheap money on a global scale was unchartered territory. The full side effects of doing so are still unknown.

HW2, its extraordinary you already know the outcome of this money printing experiment. Through vested interest, being in complete denial is a personal choice.

Choose wisely.

Hi troll, 👏

Without responding to the points you weigh in. Spinning your broken record and putting your mantra on repeat. Boaring 🐖🐗

HW2, even if your responses lack thought, they're the one thing that's predictable. All you had to say in response to my points was "I did not consider that"

I am glad you know your name and come running when called 🏃♂️🤣

Consider that..

HW2, all your responses lack thought 🤕 They're the one thing that's predictable.

His is Reverend Retired-Poppy. You may refer to him as The Reverend.

"In the 15th century it was used as a general term of respectful address, but it has been habitually used as a title prefixed to the names of ordained clergymen since the 17th century."

Welcome to NZ, where we turn basic human needs into an investment opportunity.

Yes but you can say the same about all other human needs. Companies providing solutions is what makes the world go around

And you have unwittingly illustrated my 2nd point above that business owners are whacking up their pricing right now. While the price of rents is below the cpi, perhaps falling. Which one gets the lions share, or even all of the attention and vitriol

Eg contact energy having a field day with price increases they could not justify as we are high percentage renewable. Do you or anyone of the DGMs invest in contact energy shares either directly or indirectly.

"business owners are whacking up their pricing right now"

Sounds like higher inflation which means even higher interest rates - which is bad for asset prices like houses.

If rents are based upon supply and demand there HW as most property investors tell me, then it won't be an issue as rents will keep up with the rising interest rate costs - but if they do, they too will feedback into the CPI, which will result in even higher interest rates..

Its a dangerous game if that feedback loop gets out of control.

Am pretty sure that you invest in contact energy shares. Your conscience is seared, by your double standards

"Am pretty sure that you invest in contact energy shares. Your conscience is seared"

Not at all - if any business is raising its prices at a rate that is too fast and is contributing to runaway inflation, or inflation above the mandated band of the RBNZ, I fully encourage the central bank continue to raise the OCR until it is not possible for them to do so any further. I expect share prices to fall in like other asset prices would/should as the cost of capital increases - but that is the price you pay when inflation is allowed to get out of hand in order to save people and companies holding bad debt.

(might be time to take a break from the keyboard there HW2 - I've just gone through the comment thread above and it looks like falling house prices might be making you lose your cool - calling people f-wits etc).

And would you stop editing your original comment - this is what TTP does....modifies his comment in order to make your response to what was original said, to be taken out of context. My response to your original post is now 30 minutes before your original post..so you've spent 30 mins changing what you originally posted. I might need to start copying and pasting all of your comments before I reply to them - such as I do with TTP as I don't trust him to not to try and play tricks...(odd that he was done for deceptive business practise eh?....or perhaps not).

Fix a typo... can/cannot. My bad

I appreciate your response, dont agree with it though. Mostly waffle and pot calling kettle.

"Fix a typo... can/cannot. My bad

I appreciate your response, dont agree with it though. Mostly waffle and pot calling kettle"

50% of your comment changed and included new arguments about companies and holding of a specific company shares - that isn't fixing a typo. That is introducing new lines of argument in order to try and twist my response in your own favour. (i.e. it is deceptive).

Unfortunately my trust is gone now with your comments, so like TTP, I'm going to copy and paste your comments before replying to you from here on in to prevent you doing this.

I think you are talking about my original post IO. Added a bit at the time which is pretty normal, something you have done yourself. Compared to one or two others here you are quite reasonable without all the posturing and personal attacks.

Tell me, do you still want to buy a home and when by?

Truly unbelievable...... 🤕👎

The amount of times I come back to an article, see "new comments" only to find the bulk of them are edits several hours after the original comment was posted. Usual suspects are TTP and HW2.

What a liar you are, you do yourself no favours with comments like that. If you want to talk about editing posts you need look no further than retired poppy and his forever fiddles

And as for your own fake laments on incremental house price rises, do you need reminding how you were boasting right here many times about multi-bagger profits you made on your first home. How you sold out to a first home buyer at the top of the market. But now trying to come across all pious of course.

.... or HW2, going from a small time Landlord with a sole rental in Hamilton to having one in Auckland, Tauranga and Coromandel. All in the space of 18 months. Then proceeding to boast about 100% profits on all three! HW2, you are indeed the master of make believe. You are the one who is truly unbelievable. 🤕👎

HW2, the truth is easier to remember OK! 🤕

Something tells me you're going to regret making up this stuff now that house prices are in full retreat. Que the back-peddling.....

I also own a ride on lawn mower as well as a double battery mower. Aren't I doing well. How are those bonds of yours, I bet you cashed them in and bought a rental late '21.

It is all about choices and timing

HW2 caught out telling, what this housing correction has revealed, as poorly timed lies. 🤕 You'll most likely vanish than face others that know your potential losses. Rather than complicate things for yourself, I'd suggest just keep it real like the majority of others on this forum ok😉

I never held a gun to their head, they made an offer via deadline sale. Nothing wrong with a little gloat, it doesn't exclude me from lamenting the market conditions that lead to it. I mean, I could have sold below market rate for altruistic reasons and then put my family in a worse situation when buying our next home.

Hating the game and doing well out of it for your family aren't mutually exclusive.

Think the quotes I have read are 30% drop in real terms.

The price increase of a cabbage is completely different then hundreds of thousand of dollar increases for the largest part of people's disposable income.

It would appear that the only thing that can save the housing market would be a premature pivot by the Fed before inflation is contained.

And if they do this, it is the beginning of the end of the US/western hegemony we've experienced in our lifetimes.

Uncontained inflation for the global reserve currency isn't an option for the world as we know it/have known it - it would cause global chaos/war (because of the pain and instability it will cause other nations - and it would make the US extremely unpopular - ie people will want to go to war with them to remove their reserve currency status in order to improve their own lives/countries).

So which way do our property spruikers want it - to preserve the insane valuation of their over priced house in an insignificant country like NZ, or see the end of the western led world and living standards? I've discussed this topic with a lot of the property investor class, and for many, they believe that the value of their asset is more important than maintaining the world order - which has given them so much over their lifetimes. It's crazy in so many ways. Killing the goose that has laid the golden eggs.

#peoplehavelosttheirminds

Viewing above I have to say the smugness of the spec crowd has retreated somewhat.

Radio today on what to do if your 2% is finishing and your facing 6-7%. Even Propeller is advising selling your spec box and paying down debt.

World must be ending if Propeller are saying that.

Be a laugh if their new slogan is 'sell your housing portfolio immediately to secure your financial future'.

Ideal for FHB in Palmy North..

Ideal location right next to the duck poos lagoon. Would have been 2mil + in the heyday.. But that day will come again according to TTP

https://www.trademe.co.nz/a/property/residential/sale/manawatu-whanganu…

Yep over $2M in December 2021 according to Homes.

https://homes.co.nz/address/palmerston-north/hokowhitu/73-jickell-stree…

Being here only 2 years and a first time buyer, I find the comments section on Interest a huge insight into Kiwis perception of what's going on in the market.

To the 98% of you with your in depth opinion backed up by NZ housing trends and history backed by quoted fiscal studies, thanks so much, I really appreciate reading your views on these Articles.

To the other 2% I bet there are thousands like me that look at this forum to form an opinion. Just saying ...

As a potential home buyer I come here for daily news updates as a valuable resource to learning and knowing more. I am hoise sitting to make extra savings and its going great.

Most of the banter is good with some wise commenters and the others are just wise guys who need a proper hobby. I agree with the previous comment

You want to be careful coming here and taking other peoples advice because had I been here all those years ago and been put off buying a house forever I would still be renting and totally screwed now instead of living in a mortgage free million dollar home.

The truth is in the middle, not up/down, in/out, rich/poor. Being careful not to say L/R

All those years ago is the key.

Fact is nobody knows where the market will be in 15 years so house prices doubling is still likely. If you want to win Lotto, first you have to buy a ticket.

It is just a snapshot in time, as house prices have to drop as interest rates rise. But that price drop will take time to filter through.

Fitzgerald and other socialist-minded readers on this forum - if you read the article, you will note that first-home buyers have not benefitted from the recent interest rate hikes. Whilst these rate hikes are crashing the housing market, first-home buyers are actually worse off. This is because they cannot afford a mortgage at higher interest rates, even though purchase prices have significantly decreased.

I, and other pro-economy minded commentators on this forum, have told you so. Remember, you will likely not benefit from socialism. Communism/socialism leaves almost everyone worse off, including (likely) you. The only exception are what East-Germans used to call 'apparatchiks'.

Also, your glee towards the well-off does not help you. Apart from the fact that envy is a vice (i.e., it puts your eternal life at risk), it is also unhelpful in this life. I recommend you focus on your success, rather than on other people.

Personally, I am lucky to have sold properties as the market crash was unfolding. I am effectively in a cash position (or one might say, a 'short' position regarding property), with an unconditional large settlement due in a few months. But be that as it may, I do feel for others and I try to never, ever, at any cost, to be gleeful about others' misfortune.

God bless!

I love these comment sections on interest.nz. It shows true colors across all spectrums, spending hours and days replying to comments on a bulletin board to strangers. Great productivity :) Thankfully I only come once in a blue moon to check in lol

I think the people here should become the government. Why not? It's the same mess anyways judging from the comments on wanting doom & gloom for all. Enjoy the ride and keep praying!

-7

We welcome your comments below. If you are not already registered, please register to comment.

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.