There may be no shortage of predictions about house prices falling, but for now at least they remain just predictions.

The Real Estate Institute of New Zealand's national median selling price increased by $33,000 in November from October.

Some commentators have suggested that's because the bottom of the market has cooled and most of the activity is in the upper end of the market, pushing up the median.

However the REINZ's lower quartile selling price increased by a healthy $20,000 in November, suggesting the bottom end of the market is still trucking along at a decent clip too.

The REINZ's House Price Index (HPI), which adjusts for differences in the mix of properties sold each month, increased by 1.9% in the month of November. If it continued to increase at that rate this would give annualised price growth of around 25%.

That has led some commentators to point out that the rate of price growth is slowing, which could be a precursor to eventual price falls.

It's true that price growth has slowed.

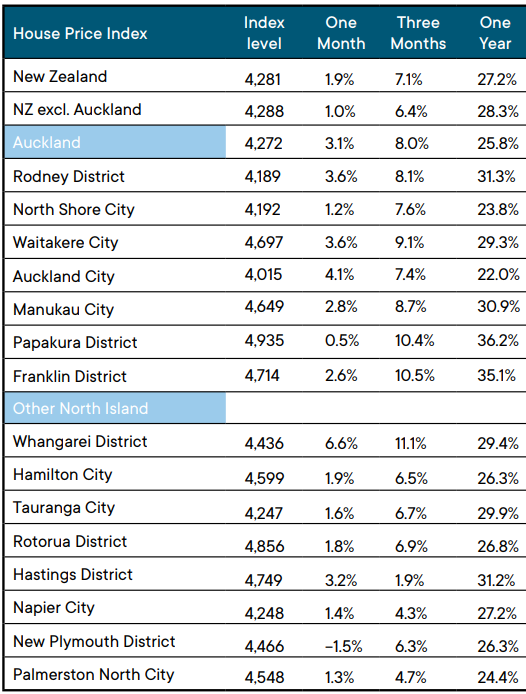

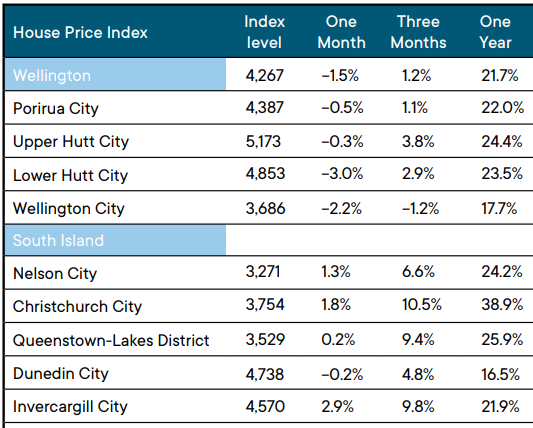

The REINZ's HPI increased by 1.9% in November compared to 3.3% in October (see the table below for the HPI figures for all main urban districts).

But the October increase was exceptional and after such a big jump in October you would expect it to ease off a bit the following month.

However the REINZ's monthly HPI figures can be a bit lumpy anyway.

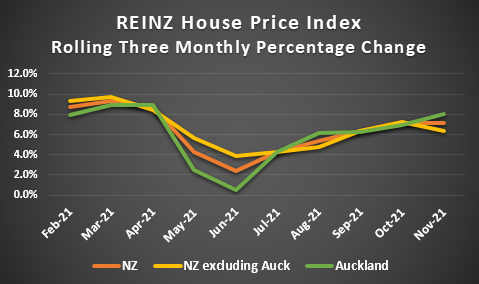

A more reliable indication of price movement is the rolling three month HPI.

The graph below shows the percentage change in the REINZ HPI between February and November this year, for Auckland, the whole of NZ, and for all of NZ excluding Auckland.

What it shows is that over the three months to the end of November, compared to the three months ended October, price growth continued to increase in Auckland, declined slightly in the rest of New Zealand, and as might be expected in such a situation, flattened out nationally.

Those trends are also reflected in the monthly HPI figures, which show ongoing strong price growth in Auckland, with only slightly weaker growth in the rest of NZ and nationally.

The key trend the graph highlights is that price increases have remained in a narrow band of between 6% and 8% every three months for the last several months, and those rates of growth are still exceptionally high and would have to fall substantially before they were even close to indicating price falls.

However the latest monthly figures do indicate some soft spots in the market, notably all of the Wellington region where prices were in decline last month, and some regional centres such as New Plymouth, and Dunedin.

Unfortunately it could be three months or so before we get a clearer picture of where prices are heading.

The market is about to put on its pyjamas and curl up for its Christmas/New Year hibernation. Thus January's sales numbers will be minimal.

It will be February before sales return to a reasonable level and those numbers won't be finalised until the beginning of March.

And of course all bets are off if Covid-19 numbers head skyward and force us back into lockdown again.

In the meantime all we can do is put our feet up, pour ourselves a glass or two of festive cheer, and make the most of the Christmas break.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

REINZ House Price Index - November 2021

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

41 Comments

What it shows is that over the three months to the end of November, compared to the three months ended October, prices continued to increase in Auckland, declined slightly in the rest of New Zealand, and as might be expected in such a situation, flattened out nationally.

? The 3 month graph doesn't show prices falling outside of Auck, it shows the rate of increase decreasing....

Thanks for spotting FE. Left a word out in that sentence. Fixed now. Cheers.

It's the properties that haven't sold that tell the story. If only the cream is selling at the lower end, that distorts the figures.

That's nonsense, how are you going to measure the value of the houses that haven't sold? Can you present us a graph of the value of the houses that haven't sold so we can get an idea of where the property market is heading?

The properties who tell the story are the ones who have sold.

While its hard to pin point on one single factor with whats happening to the housing marketing, 2022 is shaping up to be a very interesting year ahead. I have been watching the auctions the last month and ever since we got into December more and more houses were passed in. I would put it down to several factors, people switched off and thinking of xmas and going on holiday instead, people backing off because all you hear now is house prices will go down, rising interest rates, people cannot get their finance in order quickly enough to be at the auction and perhaps lack of confidence.

However I believe its due to the CCCFA and people are taking stock of what this all means or is stopping people getting the finance they need. CCCFA will have a huge impact and the banks can't do anything about it unless the government changes the regulations around it. Banks are looking at every transaction you make and adding buffers to expenses. This is adding weeks on to an application which in turn slows everything down and people end up missing auctions. People are also finding that with CCCFA banks are not lending as much as you used to be able to get so this is going to create a stalemate between buyer and vendor. Will vendor adjust to meet the market or will we end up in a situation where people just stay where they are, reducing availabilty on the market.

Interesting times ahead

House Price fall is a fallacy as neither rbnz nor any political party will be interested in Harakiri. It may stabilze or not grow for sometime but fall........never as has the blessing of reserve bank and government.

Can discuss and analyse each data but fact is, NZ has no economy except Housing. If housing market falls NZ falls.

This country is in need of reset. We can't live on borrowed money and free handouts forever.

Come on, it won't be too bad. No one will die!

That's exactly what the currency debasement engineered by the government and reserve bank is doing in slow motion.

Do not hold their monopoly money.

I would normally agree with you, but I think this time is different. I know those words gets used alot, but the CCCFA is going to change everything unless the RBNZ and Government step in, however they will only step in when its too late and take months and months of sitting on their hands.

On behalf of future generations who don’t have a voice, let it fall! We the privileged believe that we have a god given right to live our lives without any possibility of hardship and certainty of endless fiscal growth. Our arrogance towards those to come is despicable.

The mortgage market has stopped. So the property market will soon stop.

If local banks won't lend nearly as much, is there another player that could step at higher margins?

No I don't think so because they will still be tied to the CCCFA and the regulations around this. They will need to follow the rules aswell and the days of relying on your equity you have in your property have gone. Its purely based on what you earn and what you can service and the CCCFA has just made it that much harder. The banks have questioned everything from how many coffees you buy, to lotto tickets to usual expenses i.e gym memberships, every transaction is reviewed. So if anyone was to apply for a loan I would keep 3 months of clean statements and spend as little as possible.

A million is just a number these days. People ask for multiple of millions for properties these days. Seems like the value of money is not worth the paper it's printed on.

How many years does it take to save a million on average salary. The whole market place is about speculation and money which will be made in next 20 to 30 years. If an event happens and we try to realize this virtual money now, you will find that all pockets are empty.

Money doesn't exist anyway. It's just a unit of account.

27.5 years

No lending market means a falling housing market

Absolutely. The demand side is dropping away significantly while the supply side is rising.

Only one outcome that's likely really, unless the RBNZ changes course (unlikely in at least the next 6 months) or there is a global or local event (eg earthquake) that forces its hand.

A Delta/Omicron outbreak can easily change the directions things are going...

At the moment it looks like Omicron might substantially accelerate the end of the pandemic based on rapid doubling time and very mild symptoms. If this plays out as it has so far in South Africa and the UK I hope New Zealand doesn't have to suffer Delta much longer. However politically it may be seen as expedient to try to get one more popularity boost by frightening people with apocalyptic Omicron scenarios instead of making a decision on data.

All bets are off if it's a political rather than scientific decision.

You can already see it playing out that way in the UK. The messaging from the UK seems alot different than what's coming out of SA.

BoJo is trying to use it as a smoke screen as pictures come out of his staff partying it up last year during lockdown. Also they've made no real progress on the channel migrant crisis, only helped slightly by the fact that it's difficult to cross in winter using small craft.

The biggest risk to house prices (and the less important parts of the economy) is a delay to border reopening. It looks like Government are trying to find the perfect scenario in which to reopen borders and, of course, no such scenario will ever exist.

House price rises are the only thing keeping Labour in power. If this dwindles in 2022 then Labour are cooked. Never have I seen someone build up so much political capital in one year, only to lose most of it the next. She's gone. Maybe Chairman Xi will give her a job.

You're dreaming to think this is what is keeping Labour in power. 80% of people want lower house prices according to a recent survey.

The numbers are out of date. Anybody with their ear to the ground knows that a frigid wind has been blowing over the Auckland market these past few weeks. Very little is now selling at the auctions.

Price discounting is just a matter of time.

Yep they are truly backward looking.

The Auckland market has frozen that's for sure.

Certainly wouldn't want to be a developer or builder midway through a development. Good luck to them! Keep prices the same at settlement and risk making a loss or try and wriggle out of the sales and purchase agreement (as some are doing, refer recent NZ Herald article on Chancellor) and hope like hell there will be new buyers....

Carnage coming. It's got mid-late 70s NZ house building crash written all over it.

Have the same sentiment, but the cost of land and building is increasing - this will keep huge falls in check esp.in AKL.

House price flatline now for 2022. This happened several years ago in Auckland, house prices when nowhere for a period of 5 years or so. No idea what some people are going to talk about on here when it happens. The problem is when they finally "Go Up" they really move. Annual price gains now of a few percent will send everyone to sleep.

I don't think anyone can be certain at all, which makes it interesting.

Tony Alexander wrote a good piece the other day about the impossibility of forecasting in this climate. And that is a guy who usually makes a call.

Better to talk of scenarios and probability.

It was only a couple of weeks or so ago and he was making a call, now he's coming out with articles like this...?

No one can predict but given the prices easing, and rates rising , when would be a good time to buy ?

Now or wait and see ?

I just advised someone in the family to wait until Jan-Feb. Not so much about pricing but many people are trying to unload complete rubbish into the end of the FOMO market. Auckland is full of staggeringly old and badly built houses that owners have made no attempt to even try and maintain, honestly complete trash at $1.6 mil that you wouldn't buy full stop.

Seems to me like the vast majority of the houses like this selling for that price are being knocked down.

Buy old house for $1.6m

Build 4 units for $2m

Sell 4 units for $5m

$1.4m profit.

However the REINZ's lower quartile selling price increased by a healthy $20,000 in November, suggesting the bottom end of the market is still trucking along at a decent clip too.

That's the golden nugget- nothing like moving ahead whilst the rest is asleep.

There's still room for upward valuation.

Be quick.

I have had property dealings in 2 other countries - USA & Australia and have now come to the conclusion NZ'ers as just as crazy on property, as the Americans are on their stock market. While they are both built on corporate welfare and handouts from the government ie taxpayer !

This Labour Goverment really does just spend money like "lolly water" and they never think HOW will all this money be PAID BACK ???

Then you have higher interest rates now and inflation (theft) around the world - for a small economy and looking at it optimistically, I can see a lowering of 90% of peoples standard of living to be a best case scenario for 2022.

I won't even go to those "worst case" scenarios - I have now "drunk" the kool-aid and to mention anything negative, you are thrown in to the "DGM" box, as not suiting the narrative of those with "vested interests".

I now just live by the mantra to minimise any F.I.R.E. spending - Finance (no credit card interest etc) Insurance (if you can afford to lose it, don't insure it or minimise payments) & Real Estate - minimise your rent or mortgage(s) etc

Looking from the outside at the NZ (esp. Auckland) property market, is just tax payer fed "ponzi scheme" with "easy money" (only for some) and a debacle that makes NZ laughing stock around the world.

'I now just live by the mantra to minimise any F.I.R.E. spending - Finance (no credit card interest etc) Insurance (if you can afford to lose it, don't insure it or minimise payments) & Real Estate - minimise your rent or mortgage(s) etc'

That's a great mantra. Avoid the FIRE!

Homes.co.nz just released the latest update, another $30K on my place in a single month.

Thanks for the REINZ 3 month HPI rolling average Greg, it's a great, telling graph.

Have a wonderful X-mas break!

beats working

https://www.google.com/amp/s/au.finance.yahoo.com/amphtml/news/2022-pre…

10% Rise Aus

https://www.showhouse.co.uk/news/house-prices-forecast-to-break-records…

10% rise UK

https://www.newshub.co.nz/home/politics/2021/12/treasury-predicts-house…

10% rise by NZ government 22

27 Trillion of money printing globally with rampant inflation and asset appreciation.

So to cool it banks decided to let auctions go a little soft unless you willing to risk some cash like all their willing conditional buyers.The conditional market is multi offer globally with a mean sale time of 21 days and the south island is next day on most.

150,000 long term migrants are now rightfully getting residency for free after being denied it for up to ten years. That's 5 years of demand right there and are immediately getting a home loan!

We welcome your comments below. If you are not already registered, please register to comment.

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.