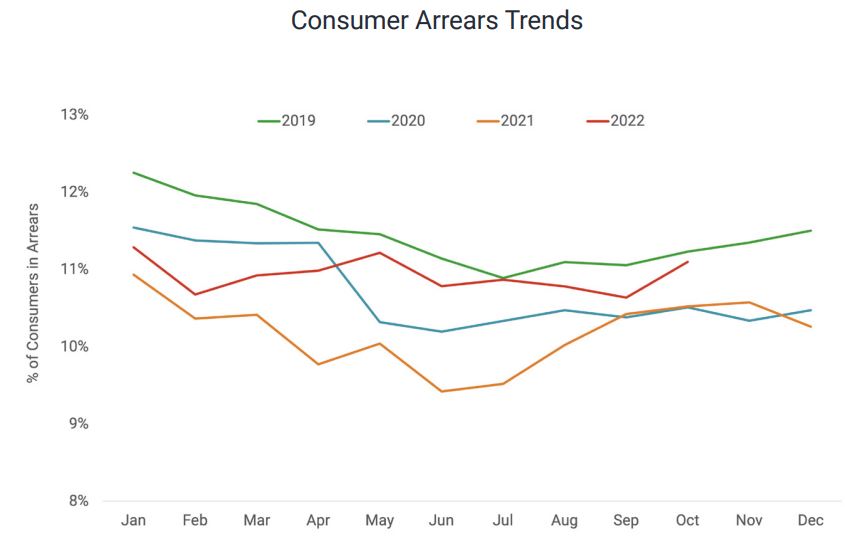

The number of New Zealanders behind on consumer loan repayments is rising but still remains behind where it was in 2019 pre-Covid-19, data from credit bureau Centrix shows.

Centrix's latest monthly Credit Indicator report shows the number of people behind on repayments rose 5% during October year-on-year. That means 400,000 people in arrears on consumer loans, up from 375,000 a year earlier.

Whilst October saw a sharp rise, as demonstrated in the chart at the foot of this article, the number of people behind on repayments is still a little behind where it was at the same time of year in 2019. It is, however, ahead of 2020 and 2021 when a lot of public money designed to combat the Covid-19 pandemic and related restrictions was sloshing around the economy.

Centrix says 4.2% of credit active consumers, which is anyone with a payment obligation on a credit account that's open or active, are currently 30+ days past due. This is up from 4.0% in September. Meanwhile 2.3% of consumers are 90+ days past due, which is unchanged from September. This means 150,000 borrowers are at least 30 days past due on consumer loan repayments, and 82,000 are at least 90 days past due. Meanwhile, consumer credit defaults were 21% higher year-on-year.

The proportion of home loans with missed repayments rose for the third consecutive month, with 15,200 mortgage accounts currently past their due date. Whilst the figure is rising it's still low compared to pre-pandemic levels and represents 1.03% of the total, Centrix says.

Centrix's November Credit Indicator says demand for personal loans rose 18.1% year-on-year, with 60,000 applying for a personal loan. Vehicle loan demand rose 17.3% with 25,000 people seeking a vehicle loan.

In his commentary on the report, Centrix Managing Director Keith McLaughlin said arrears rose in October as people struggled to meet their repayment commitments across a range of credit products including vehicle and personal loans, telecommunications and utility bills, plus mortgages. And while arrears rose, demand for consumer credit also grew as people turn to new avenues to make ends meet.

"New consumer lending has climbed for the last three months, and the looming festive season is likely to be a source of stress for many Kiwis who are already dialling back their discretionary spending," said McLaughlin.

"In fact, we’re seeing those who generally live on a tight budget and young borrowers feel the pinch the most, forced to cut back on non-essential spending due to cost of living pressures and other external factors."

.

"This cutting back of spending is also impacting retail businesses, as consumer confidence continues to dwindle, and rising costs have seen an increase in business defaults in the sector," McLaughlin said.

"Despite this, the hospitality and tourism sectors have seen some great activity as international travellers return to New Zealand, bringing a much-needed economic injection to these industries."

17 Comments

One of the (many) things that get me angry with economists is how they lump everyone together - see the many comments about 'households have saved a lot during COVID' - as if every household is identical and they have all saved money up etc.

What the data is showing is that different cohorts of households are being affected very differently by this weird period in our history - some have amassed zero money during COVID, are now struggling to keep their heads above water, and are going into debt despite working multiple jobs (and putting their kids to work). Other households have decent income but their mortgage is hoovering up 50% of it, so they are chopping back on discretionary spending but staying afloat for now. Other households are doing great - saved a tonne of cash during COVID, investments are paying nicely, got a nice bonus from their companies etc - bottoms up at the local posh restaurant etc.

Ultimately the next year will see the first cohort really struggle, and the second cohort get bigger and more challenged as mortgages flip onto higher rates. The latter cohort (the rentier class) will, as ever, just keep on chinking their glasses to their good fortune.

It's also a good time to be a renter that has either "missed out" on buying in 2020/2021 or has been savvy enough to not join the hysteria that was the post-Covid NZ Housing Market.

So if you're sitting in a rental (even if it's small or dingy), yet on a house deposit that is growing nicely (especially after having had a decent enough pay rise and with interest rolling in on that deposit), now is a good time to chink your glass.

Here's to finding a good, safe time to buy where prices will be realistic enough that you won't be lying awake at night in years to come worrying about how to pay off an insane mortgage.

We welcome your comments below. If you are not already registered, please register to comment.

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.