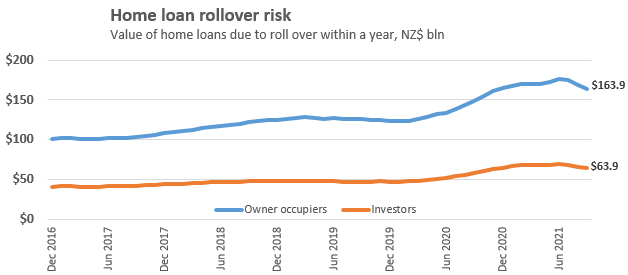

More than $230 billion of home loans will roll over within the next 12 months according to Reserve Bank data.

The repricing risk on this is substantial.

Homeowners and investors may have to find close to $6 billion a year to pay the higher interest rates stemming from recent increases, plus further hikes coming.

That will involve about 1.7% of annual economic output from the whole economy (GDP).

So far, the two year fixed rate has risen from 2.55% to 4.15% (ASB) over the past 90 days. That is an extra 1.6% pa. in a very short space of time. It does not seem unreasonable to assume more is coming. If rates rose to 5.0% by October 2022, some might say that is a conservative estimate.

Holding that 'conservative' estimate, if interest rates rose 2.5% in a year, on the $231 billion that is due to be repriced in the year, the annualised cost of that increase is $5.8 billion. Given our nominal GDP is now running at $340 billion, that makes the added mortgage servicing cost equivalent to 1.7% of GDP. That is a lot of 'growth' required just to pay these higher mortgage bills.

Of course, nominal GDP will likely expand over this time period too, so the impact won't be quite as fierce. Rising inflation may bring rising wages and this will help 'pay' for these increases.

But rising inflation will bring a Reserve Bank response, most probably an extended set of rises in the Official Cash Rate which in turn will drive interest rates higher again.

All this will have a depressing impact on affordability, and the ability to pay ever higher house prices. That depressing effect will weigh on house prices.

With Reserve Bank Governor Adrian Orr out jawboning an end to the long-running house price inflation, he will know he has set in motion strong pressures that will end the run.

Sure, many potential sellers may decide not to offer their properties for sale if prices don't meet the expectations that built up over the past 10 years or so. But with new house building ramping up seriously encouraged by the recent looser planning restrictions, no new migration arriving, and much higher costs of servicing a home loan, you would have to be brave indeed to conclude the new normal will be the same as the old normal and house prices will just keep on rising.

As Tuesday's listing data in Auckland shows, sellers can withdraw for a short time. But they can't hold back the tide.

The previous housing shortage was 'man-made' by local nimby politics (using the Resource Management Act). The era of cheap home loans was man-made too, kick-started in the Global Financial Crisis.

Now the tide is turning, and man-made policy changes will likely turn a sure-thing, one-way bet on house values, into a very unsure thing.

Remember leverage works both ways. There are winners on the way up and they turn into losers on the way down. There will be tears. There are generations who have never experienced house price declines, events which are relatively frequent in many other countries.

So, on top of the bigger bite servicing a home loan will take from our economic activity, the wealth effect rising house prices brings has a good chance of reversing, even if prices don't actually fall much. That will crimp a lot of other discretionary spending. It is an effect that could last years, maybe as long as the man-made good-times lasted.

Adrian Orr is playing with political dynamite. But these decisions are a long-overdue adjustment that we need to have.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

146 Comments

Spare income is best spent on anything housing, as this is NZs economy. I have no idea why anyone would want to waste spare money on silly things like eating out, going to the movies, hobbies, recreational activities, holidays etc. These activities are all a waste of time and of minor importance to our economy. I welcome more increased interest payments to the banks to help support our number 1 economic activity, housing!

'There will be tears'

Yes and unemployment, bankruptcies, suicides.

If someone was stupid enough to believe that house prices could only go up I don't understand how they've made it to adulthood without drowning in a bowl of cereal along the way.

The government never said house prices are guaranteed, the PM just made stupid remarks like New Zealanders expect prices to go up and a bunch of mouth breathers read too much into it.

No one wants to blame and get blamed, but, the truth is when this kind of event comes, someone needs to be held responsible, especially for those people who are in power, in this case, it would be governments, RBNZ and media. They have the power to influence and intervene the market.

CWBW is not threatened, just calling out your self interest in wanting less competition in the hopes of scoring a house. A bit like a guy walking into a bar and wishing all the men would leave NZ so it was only him and 100 ladies in the room... nice dream but time to live in the real world.

But the problem with this hypothetical situation is that men who are already married (property investors who already have a house aka wife) are out at the bar trying to pick up the single ladies (houses), meaning the young guys (FHB) who simply just want to get married are struggling to do so because a bunch of dodgy old wealthy guys want to be married and shag a bunch of chicks on the side with no concern about the social damage they are doing.

Ultimately, its immoral.

This just gets better, you definitely sound like your own insult, down to a tee and you are only adding more evidence up to the argument, i.e. obsessive concerns about others sexual behaviour. Yep you have it in spades mate.. Here is something that might surprise you, you can have sex, masturbate and have a job that earns over 500k and multiple businesses and properties. In fact the most successful financially and politically tend to do a lot of both. But sure you are *not* an incel you are just concerned about all the other incels. Those other than yourself.

Even children are pretty good a resisting the urge to resort to name calling like that these days HeavyG. Try something a bit more witty or imaginative. Or at least have something a bit more interesting or insightful to say. Raise your game a bit mate. You're letting your side down. Its embarrassing.

What a laugh. You need to look up the definition of incel. They tend to not have children or a strong sense of social connection and societal responsibility. Here is a clue try to not sound like one when you post your next comments, I am sure that would be a change for you.

The problem with your odd little fantasy is that the hundred ladies in the room aren't the kind that are going to win any beauty competitions. Scoring one would be quite embarrassing.

I'm very keen to get out and back to living the real world after being trapped in New Zealand the past year. It's strange how threatening some people find that don't you think?

However women have been more socially and culturally disadvantaged and their employment and investment opportunities are severely impaired. Hiding that truth and only pretending it is an equal playing field would be even more harmful. We have a very abusive culture and even without that the bias against women is prevalent right down to different pay for the same level of responsibilities and training. It is notable especially in the medical profession where women are expected to have more aptitude for the industry only from a stereotype of being more caring for life because they can have and feed babies, yet they are more likely to have vastly inferior pay. Hence the current predicament is severely impacted by the unequal standings of women in society and their investment opportunities in housing are severely crippled. Especially as they are expected to reach certain life goals in our culture like having kids before career or financial stability. Lets not pretend that is fairly applied to all genders and gender identities.

For instance one of the staff I has who provides nursing care has finally been approved for a 6 year training qualification course that she already has 10 years experience in. She was told that because she had kids that would discount her from succeeding right in the course interview, yet she was culturally, socially and by family pressured, (aka either do so or be ostracised), to have children with a guy who abandoned them for his own career goals, leaving her with the added responsibility. Yet from completion of the course because banks would deny her a mortgage here and her collective income cannot support housing she will look to travel overseas after qualifying in the course to a country that pays appropriately and can afford housing and living costs for her and her children. Leaving NZ out another highly skilled and qualified worker, especially needed in pandemic times, who alongside one job runs her own business in STEM fields and raises children. This due to a culture in NZ that does not value women and places higher barriers in the way of them succeeding to even a standard of having basic housing to live in. Lets not pretend that is fair and applied to all because it is not.

Because the NZ housing Ponzi needs to be continuously fed by the greater fools who think houses are a special asset not subject to the same economics' laws that apply to all other asset classes, and that house prices will keep increasing by magic, regardless of economic fundamentals.

For the housing specuvestors, the scenario of younger and highly skilled Kiwis escaping a life of mortgage servitude for better opportunities overseas in a more sane housing market is a nightmare scenario, a scenario where a bunch of boomers are left to try and sell depreciating houses to each other in a shrinking market.

PS: I am a "boomer" myself

Exactly. I want to believe. But it never transpires. It's always more of the same, but worse. I'd love to be wrong but I've given up hope.

The talk price crashes causing suicides makes me wonder how many suicides are going under the radar from a generation that's given up hope.

I suspect far more suicides from lockdowns and money pressures than not being able to buy a house. NZ is still a great place to live, if it wasn't there would be 5 million people trying to exit. Gets a bit monotonous the same people bleating about leaving and yet they are still here.

Lots of Kiwis leave all of the time and I have many friends who are never coming back. We've just been importing people to replace them. Right now the appetite for high immigration is very low and the reasons for young people to leave are higher than ever. The birth rate is in a continual downtrend too.

Yes that correct but it's a tradeoff that NZ seems willing to accept in order to keep house prices high. Those looking after you in your old age won't be your kids, and your kids wont visit much as they will be living overseas.

If housing costs were lower, staying here and accepting lower incomes would make sense. Currently it really doesn't make sense.

That's true Brock the remaining population are heads down and bums up working so hard they don't even have time to read interest.co.nz let alone post comments. I don't think NZ would be a better place full of the people that constantly bag this country at least 2 or 3 times on every article. Pretty sure Australia is opening up fast, are you packing your bags ? Your welcome to move then rave about Australia on here, that may at least help some people.

"bums up working so hard they don't even have time to read interest.co.nz let alone post comments." - well, that rules Carlos out of the work hard demographic..

btw I've moved to Australia - it's nice here. I'll probably never move back as long as the career opportunities AND housing situation doesn't improve.

Yes but as soon as our immigration policy changes (which it will) there will be another flood of immigrants, many of whom will be low skilled, low net wealth ( many with bogus qualifications) ready to burden the country even more. Meanwhile young Kiwis are unwilling to do the more menial jobs and instead rely on the Govt for a handout, which Jacinda is all too willing to provide. NZ is changing mighty fast, and not for the better.

Yeah, but do we really think the Banks, RBNZ, and the government can afford to rinse and repeat this time? Last time they all knee jerked to head off Covid, taking interest rates and LVRs while printing money at the same time. It created a perfect storm for price jumps. With inflation on the rise and the government's ballooning debt, these institutions simply can't afford to play the same tricks again.

Found their wines overrated. If you want a nice Shiraz try Cat amongst the Pigeons Barossa or Peter Lehmann even the Pepperjack is nice. If you want something great the Taylors Jaraman is a good as anything I have had on a wine tour and I have done a few in Aussie if you can find a bottle for about $35.

More money spent on servicing debt. Less borrowing to invest business assets and staff. Less money in consumer pockets to be spent on goods and services = less demand = decrease in prices e.g. recent house buyer borrowed $1m at 2.5%, floats in January 2022 into 4.5% = $20k extra interest payments = $20k not spent on restaurants, holidays, cars etc = less demand = sellers cannot increase prices = CPI falls.

There will certainly be some resistance (from both perspectives) to hold back against the changes... Many households have 1-2 years of low interest locked in still, so wont see a problem for some time.

Many businesses have enough confidence to keep afloat as demand and the number of clients willing to pay drops off. So the CPI will stay high for some time too. I'd expect to see a significant amount of hurt before CPI and OCR actually come down.

Can't help but laugh at this article, right next to it is an article saying the average house price went up by $217K in the last 12 months which is the largest % rise on record right next to this article saying they are going to go down

Sounds like a pretty big disconnect....I'll go for whats actually happening in the market vs. theory

Real asset prices are jumping mostly because the RBNZ/ Labour is printing money like it's confetti, so real assets are going up in value in response

Past results aren't an indication of future performance. "Went up" is past, from here anything can happen and it's very easy to see how it could be down or at least flat from here. It's a fascinating situation our country is in right now. 2022 will be very interesting with covid running wild and young people leaving.

They've gone up in direct response to two factors - sharply lower interest rates and a belief that after Covid the whole world wants to move here....

Well both arguments are toast. Interest rates have regained all of their Covid induced reduction and due to go higher - and net migration is stuff all. A recent article observed foreigners selling NZ property at twice the rate they were buying. Domestic de-population from Auckland to the provinces, stronger wages in Australia, and the biggest building boom is recent history - all conspire to disorderly unwind the market (especially in Auckland) over the next 1-2 years.

The best sentence I have seen in ages which FOMO followers need to remember for a long time.

"Remember leverage works both ways. There are winners on the way up and they turn into losers on the way down. There will be tears."

I fail to understand, being a highly literate population who can read, people still do not tend to do some research before they get into FOMO mode.

What did everyone who bought in last 18 months at exorbitant high prices think that money grows on trees and can be plucked when it's ripe in 3 months and they will pay off their 30 year mortgage?

"What did everyone who bought in last 18 months at exorbitant high prices think that money grows on trees" - well it did. The RBNZ and government were spending like drunken sailors, creating money, so it wasn't so much as "growing on trees" but being "magicked out of thin air", with future consequences thrown to the wind. If the government acts like that, it sets a precedent for FHBs who are young and see it as "just the way the world works". Will the government bear any consequences? Nope. Will FHBs? You bet ya...

Really do you think banks are naive to take a loss? They are protected all over the place dude. Even if they fail, they will be bailed out with tax payer money. I guess you haven't read about citibank case. Too big to fail.

Where is you money? Under the mattress??

Governments don't let the banks fail. They let individuals fail and have mortgage auctions.

Common, if we really haven't thought about this, then need more financial literacy in this country.

New house building ramping up seriously encouraged by the recent looser planning restrictions...

Precisely the reason to buy the biggest plot you can afford in the right places- the potential returns may be counter regulatory risks.

Property owners are incentivised to draw up covenants restricting further densification through grassroot action.

Conversions of larger estates into motels will see exemption from most new requirements as well as long term lease to HNZ.

For properties on dual use zoning, owners of fully paid-up properties may consider converting it into commercial and new owners may reconvert them back post sale- the frictional costs may be well worth it.

New buyers should consider tier 2 and non bank lenders. Non bank lenders may work closely with developers to assist new buyer financing.

As cost of financing is being re-priced, landlords should also re-price their rentals to better reflect the market conditions and regulatory risks.

With inflation induced higher maintenance costs landlords may also consider stipulating maximum allowable tenants on their properties and ensuring the enforcement of no sub-let and pets.

Buyers, upgraders will be wise to act soon as risks from timing the market are evolving and businesses capitalising on their home equities may consider mitigating their risks by finding alternative funding with a similar comparison rates to decouple their businesses from their private properties.

Most of the problems we face are well detailed in your comment, ie: There is a way around any regulation or tax that might be inflicted on the property sector.

There is only one way to enforce change - access to debt. Not the price of debt (mortgage rates), say, LVR 0% for all but a singular home loan application.

If you can't borrow, you can't buy or renovate or restructure or calibrate - nothing.

If you want to do any of your suggested actions, then go for it - with 100% of your own money.

Will that stop those determined to get funds at any price? No. But it will stop the majority. And it's that majority that will be 'the next buyers' of whatever it is that's presented to them.

A lot of headwinds have built up in the last five years. FBB, AML regulation, new tenancy regulation, healthy homes regulation, no foreign students, immigration gone, tax rinse going/gone, 10 year not a capital gains tax, increased supply with record consents and construction activity and central Govt driving increased intensification. More recently we have banks enforcing DTI, changes to minimum equity rules with RBNZ expected to formalize them. Then interest rates being forced up by rampant inflation with likely more to come. Yesterday you have the RBNZ pleading for kiwis not to put all eggs in the property basket - what does he know that we don't.

Capital gains train has had a golden run but its not a big step to see the fabled capital losses start to manifest. Timing after all, is everything. Please remember if any friends get wrecked from being over leveraged in the next five years, they did it to themselves.

Anyone tried air fried popcorn...?

Yes, and in the meantime thousands of young apprentices have been lured into the construction industry, so here is the scenario if the housing industry hits the wall: thousands of unemployed young construction tradesmen become unemployed, many of whom will have young families. But now that employment has become a mandated requirement of the RBNZ, a consideration equal to inflation, depressing the housing market will not be allowed to happen overnight if at all.

Ok, the RBNZ may try to suppress housing market activity and thus reduce prices by raising interest rates quickly and steeply, but raising rates will still hit FHBs because they will be paying higher mortgage rates for their cheaper house prices: a zero sum game!

If the '4-sticks' are about to strike, and some have already struck, then I would expect to see real estate agents signs going up all around me as panicking vendors scramble.

However, what struck me today was the complete absence of such signs in my expensive inner suburb and, in a popular high-density home-unit street in Royal Oak where my sister lives, for the first time in the 15 years that she has lived in the area there are NO real estate signs at all? We have never seen such a dearth of real astate activity.

In summary, I think the projections laid out in this article are more wishful thinking than realistic forebodings.

I had a large mortgage in 2006, house prices were skyrocketing and interest rates were climbing fast too.

Fixed rates were over 8% and floating was nearing 10%

I scored a 'great deal' of 7.69% for 5 years and i was 'ahead' for a year or so, then everything starting

crashing down but i was stuck with 7.69% until 2011, by which time rates were maybe 50% down and property

had 'crashed' 10% in 2008.

It all sounds familier, i wouldnt be locking in too long. One false move re china/covid or anything will change things i guess.

I did pretty much the same thing, locked in a 7 year rate at 8.6%, sounds pretty bad but the thing is with a total mortgage that started out at $255K it was peanuts compared to todays typical FHB mortgage and I was able to smash it in 15 years. Put the numbers into a mortgage calculator, its very interesting I would have still been better off back then than now on even double digit rates.

To be fair to the Interest journalists as it's mostly the BTL contributors, but this site has probably been the single worst place to look for economic advice or predictions about future house price movements over the last 3 years. Even this week there have been record prices and results for Auckland house sales.

Will it run out of steam? Of course it will - but none of us know when and in the meantime those sitting on the sidelines have watched their prospect of home ownership disintegrate before their eyes.

I didn't give any advice though, I simply made an observation. Yes, interest rates have risen but that doesn't seem to have taken any momentum out of the market yet. The strapline of this website is "helping you make financial decisions", they should change it to " helping you make financial decision, just don't read the comments".

Who would you take financial advice from, someone who could buy the multi-million dollar house or someone who cannot?

" helping you make financial decision, just don't read the comments"

Why should they need to state the obvious? Surely anyone with any sense knows that basing financial decisions on what random internet commenters post in a forum is a bad idea. Don't get me wrong, I enjoy reading the comments - but I'm not taking advice from anonymous commenters who, for all I know, have completely made up the claims some of them make about being an investment guru with dozens of properties.

There are a few posters here who have been calling property higher for a number of years, but the vast majority did not. That doesn't mean I/we think that's a good thing, but it was predictable. Many other assets have risen as well, but generally you don't get the leverage or tax concessions. A few posters here are better informed/experienced than you might think and certainly far superior to an financial advisor.

A few posters here are better informed/experienced than you might think and certainly far superior to an financial advisor

Sure, that might well be true. But the point is that all I (and anyone else) have to go on is their anonymous comments on a forum. There's no way of confirming that any of the claims they make about their experience are true or not. The person who claims to own dozens of properties and be an investment expert could be a 14 year old posting 'advice' for shits and giggles.

If you look at all the advice and predictions given by different posters, its all over the place. So even if you wanted to, you couldn't follow 'all' the advice. You'd have to pick one or two commenters and follow theirs. But then you get this problem - you've got no way of verifying any of the claims they make, and no way of verifying who they are or what their motivations are. Point being, it's good to be informed and reading a variety of comments on a website such as this can help people become more informed, but I think it's nuts to base financial decisions on what an anonymous internet commenter says in the forum of a website, no matter how experienced and informed they claim to be.

To paraphrase The Bard:

"better three (years) too soon than a minute too late,"

Is it better to watch the possibility of home-ownership disintegrate before one's eyes or watch the same happen to one's net worth (or worse, if we ever hit negative equity scenario)? As you suggest, we'll all know in another (3 years) time!

I sold property in Opaheke at auction yesterday. 5 registered bidders. Lots of auction pauses and negotiations behind the scenes. Went fractionally below QV.

Not the frothy sellers market of recent times. Real time experience is reported a month later in stats. From my limited experience yesterday, I'd say the high tide mark has been reached. How quick and how much the water recedes will be interesting.

That's interesting Citm.

I posted this last week but didn't write it very well.

We sold our place on the shore last Thursday, there was no marketing campaign other than listing it on TM last Wed arvo (and an internal B&T email sent that same day).

There was an offer in writing about an hour after going on TM. Somehow the agent put our numbers on the internal listing so we had 3 calls from different agents wanting to come through.

Overnight the original offer went up 6 figures. Another two parties through Thurs morn. Phone calls from more agents wanting to bring people through.

We almost certainly could have got more. But it would have meant going to auction on the place we wanted whereas if we accepted the raised offer on our place we secured the place we wanted so we took the bird in the hand.

The person who bought our current place hasn't been here, there were no internal photo's on the TM listing, just drone shots.

We sold just shy of double CV. (which is way, way over the property high/low price bracket estimates)

Of course we paid nearly double CV the place we bought so we're not retiring into the sunset, but we were surprised at how crazy it was.

It was all over in about 18 hours.

Yep, it's screwed up in the worst possible way. (hope I didn't sound like I'm crowing about it because I'm not)

The only winners are the people with multiple properties. Us plebs who just want somewhere to live are no better off whatsoever.

As for the younger generation, I'll certainly be encouraging my kids to head overseas when they're older unless there has been an almight reckoning.

I've got a mate at B and T, spoke to her today, said crazy market in Auckland, most houses being sold before hitting the market as per your description, or multi offer. So at this stage it's bau up there, lockdown hasn't slowed things at all only added to the fomo.

Hi David Chaston,

Do not agree with you for :

1 : Never underestimate the power/influence of Orr and Robertson (Though are two separate entity but reality is otherwise).

2 : Greed is too Big : Addiction of easy, fast and BIG money has become a way of life in NZ (Earlier also but not at this level and was with certain percentage of population but not all). Many businesses have either shut down or put their businesses in hibernation and are concentrating only in speculating or have become mum and builders - pathway to retirement in a year or two and are not wrong.

3 : Only real economy in NZ is housing Economy which is also been substantiated by bank data released that confirms that appox three fourth of finance went into housing sector.

Wonder why you or anyone does not highlight the biggest factor is not Supply but FOMO for steep multiple rise on monthly basis, if that was not the cause why would people fight over toilet paper - so can imagine what it is and will keep on doing to housing as is basic necessity which has been turned into speculative chip by people in power.

When Jacinda Arden says that no Kiwi wants their value to fall (As must be brain washed by bureaucrats and experts surrounding, otherwise why would she be talking the same tone as of National - reason bureaucrats manipulate the show by pressing the right button be it any party in power- all those not sure should watch BBC serial Yes Minister) - she is partly correct that no one wants the value to fall ANNUALY and if it goes up by 60% or 120% and falls by 10% or 15% is not actually a fall but important not only fundamentally but also to control FOMO.

David, will like to see in 3 to 4 months time if your thinking proves to be correct or.....

Also should ponder and write about FOMO and beside financial divide, how this has divided the society, which will take time to heal and hopefully is peaceful.

Feel that will need lot of effort and changes by this people in power to calm FOMO and have doubts...it has to be external factor like interest rate hike, which is due to wholesale rate/international rise and not just because of rbnz rise of 0.25%.

Your thoughts or / and comments from readers who feel otherwise as discussion is always good.

All of the above, plus start incentivizing other investments or even just PAYE

- Lower tax on any kiwisaver

- Gradually shift tax burden from income tax to land tax, or at least have a reasonable balance of both

- Lower CGT for holding stocks or other investments long term

Yes not looking great if you are over committed on a property or properties. What I don't get is that you can bet your bottom dollar that there will be a heap of people that sign up to purchase a property this very day after having begged, borrowed and sold their souls to the devil to do so who will be blissfully unaware of what is bubbling away.

Don't get me wrong, I have a lot of sympathy for FH buyers as I was lucky enough to purchase my house in a different era, however I think if there was ever a time to avoid the FOMO trap and do your homework before committing to a lifetime of debt, now would be it.

Unfortunately I don't think many will believe there is a problem until it affects them directly, like when the have to re fix their mortgage for the first time.

Just lining up to introduce a Universal Basic Income to help cover the shortfall. When disposable income drops enough to hurt the economy, they will top it up. UBI will help FHBs save up a deposit and keep the can kicking down the road. Or, it will help stop a backslide in house prices.

You lower interest rates / print money to save your economy, that causes inflation. You raise interest rates / stop printing money and your economy tanks. You lower interest rates / print money to save your economy, that causes inflation. You raise interest rates / stop printing money and your economy tanks. You lower interest rates / print money to save your economy.

Buying and sitting on a house long term is a no brainer unless a completely new monetary system is coming!

Yes, I think you are right. When the property bubble blows up this time, it's going to be bank bail out time (despite them apparently being assessed as being able to handle almost any downturn, according to the RBNZ stress tests). Enabled by printing a trillion or so NZD and handing it out left right and centre to any big business that looks like it might be in trouble. It's a central wankers wet dream, screw the young as long as my fellow economists don't suffer any consequences.

I also think you will be right. First they will kill confidence in the currency, but the deleverage follows anyway.

The extent to which they rely on money creation determines the theft from savers, and the borrowing determines the hit to current and future tax payers. Shall we split the bill?

Although the cost of mortgages has risen by some 50% in the last few weeks, the rates are still significantly less than the inflation rate. So for investors that isn't a bad thing at all, apart from the blow to free cashflow.

Hard to see how this will all play out, many moving parts here such as net migration, interest rates, building costs, land values with the new density rules, interest deductibility sinking lid, etc.

It would seem that the market has topped out or should soon do so, but this may not actually be. There is an awful lot of wealth and money sloshing around. In terms of Phil Anderson's land value cycle theory that I last looked at a couple of years ago he thought this would keep going to 2026 or so after the mid-cycle slowdown. I must check that again come to think of it. Maybe the cycle has been foreshortened.....

Possibly at the 16th hour on his 24 hour clock - so right near the end of the 14 year 'up' cycle.

When did the 'up' cycle commence, about 2010? So yeah the cycle might be a little foreshortened, by a couple of years. He does talk about these cycles in terms of average number of years.

PM mentions the term "speculator" in the context of being the primary cause of the housing boom this year. Not just once either. Ten year bright line mentioned in changes under currently progressing under urgency.

I reckon they need a hotline for people to highlight property sales in their area that should be being taxed. We need our tax after all...

But house prices logically CANNOT go lower, I believe, unless more land is released and/or the cost of building a house (labour and materials) is reduced. This is not happening.

This is because, demand side pressures have been going up and down for the last 100 years and are not the UNDERLYING cause of our housing crisis. This is surely the fact that the supply of city fringe land stopped in the 1970's; when councils in the big cities ring fenced their fiefdoms.

Auckland was releasing 600 hectares a year in the early 70's, (eg Pakuranga) but since then, has averaged about 30 hectares per year. To make up for the lack of supply, every large city needs to double in size - to crash the price of land from 50% of purchase price back to 20%. I believe we need a "Housing Act" to compel this and put in place, "price triggers" to mandate land release when prices rise. If not, we will all become landless peasants living in Soviet style boxes.

We welcome your comments below. If you are not already registered, please register to comment.

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.