The fund that was set up 20 years ago to help out with New Zealand's future pension requirements has just enjoyed its strongest ever annual return, lifting its value by 29.63% to $59.8 billion.

The NZ Super Fund's chief executive Matt Whineray (pictured) said the $15 billion increase in the value of the fund in the financial year ending June 30, 2021, was "exceptional".

“This past year demonstrates the importance of sticking to our long-term investment strategies, which are designed to play out through market cycles. The Fund has a portfolio mix that was well positioned to capture strong returns from rising asset values over the year.”

In the nearly 18 years since investing began in 2003, the Fund has returned 10.67% per annum (after costs, before NZ tax). It has exceeded the 90-day Treasury Bill return by 7.14% per year - that's by $39.1 billion in total, and the fund's 'Reference Portfolio' by 1.24% per annum.

Whineray says these are world class results.

"What this means is that the team has added $10.6 billion of value above what would’ve been achieved with a simple, market indexed, passive portfolio. This is achieved by active investment strategies that leverage our endowments, such as our strategic tilting programme, private market assets and credit & funding investments."”

The net contributions from the Government of $12.4 billion have now grown into a $59.8 billion nest egg, ringfenced to support future superannuation payments.

The Government is projected to start making withdrawals from the Fund to help pay for superannuation from the mid-2030s, and the Fund is forecast to continue to grow as a percentage of GDP through 2070.

"Given that time horizon, we’ve built a growth-oriented portfolio that will generate strong returns over the long term and performs strongly in periods of market expansion," Whineray says.

However, there's some caution for the year ahead.

"With markets continuing to perform strongly and economies rebounding, supported by accommodative fiscal and monetary policy around the world, we’re possibly looking at a period of increasing inflation and rising interest rates. That combination should weigh on company returns and creates a challenging investment environment. We do not expect the outperformance of recent times to continue forever," Whineray says.

"At the same time, the ongoing impact of Covid-19 and uncertainty about virus variants weighs on economic sentiment. It’s a recipe for ongoing uncertainty we aim to tackle by focusing on the long-term performance of the Fund."

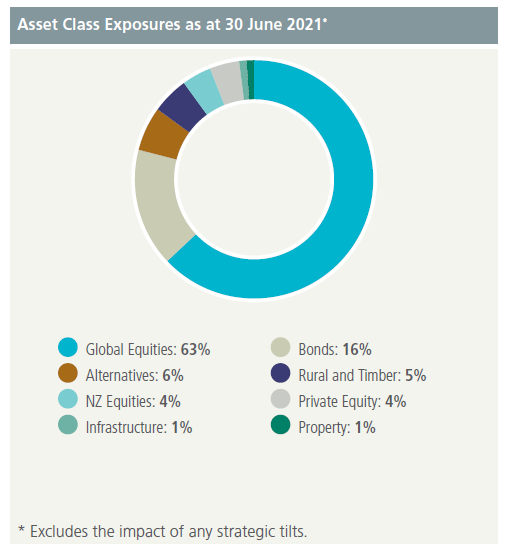

This is what is in the fund:

The Fund’s New Zealand investments include stakes in Kaingaroa Timberlands, Kiwibank, Datacom, LabTests, Fidelity Life, $2.5 billion in listed equities and a range of investments in property, farmland and small-medium size growth companies.

6 Comments

"Given that time horizon, we’ve built a growth-oriented portfolio that will generate strong returns over the long term and performs strongly in periods of market expansion," Whineray says.

What happens as we go down the Limits to Growth downside (as per Herrington/KPMG)?

I doubt it will 'perform strongly' or 'generate' (a word stolen from physics, where it really means something) strong returns.

Was Whineray asked about that?

so 15% against interest of 3% not to mention the tax return they get back off the superfund each year already, up to last year they have paid tax of 6.9 billion

people talk about national being in charge of the government books because they are better managers of of the books which makes me laugh they are every bit as bad as labour if not worse, they have no long term vision when they get there its all slash and burn for quick results

We welcome your comments below. If you are not already registered, please register to comment.

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.