The Reserve Bank (RBNZ) may have to lift the Official Cash Rate higher than earlier thought if the labour market doesn't show some sign of loosening soon, ANZ economists say.

At the moment the OCR is at 3.5% and is widely expected to be raised another 75 basis points on November 23 in the next review.

ANZ economists say in their latest Quarterly Economic Outlook that their current prediction is for a peak in the OCR of 5% next year.

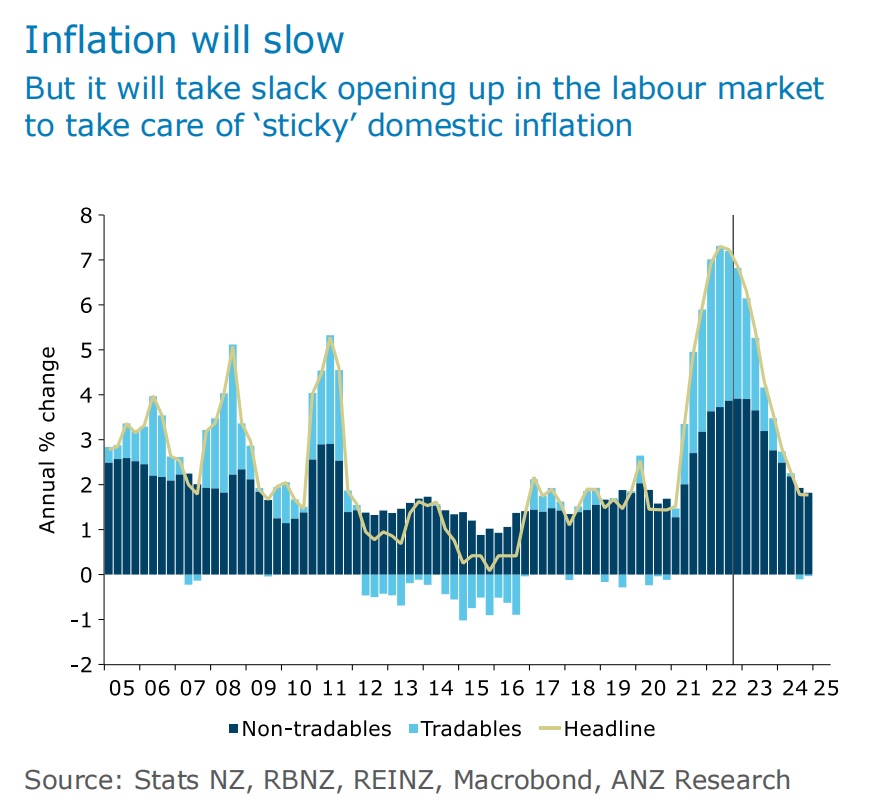

But they say, while they do expect CPI inflation to slow from the 7.2% level seen as at the September quarter, they still see "significant upside risk" to the domestic inflation outlook.

"If the labour market doesn’t show signs of loosening soon, the OCR will very likely need to go higher than the 5% peak we’ve pencilled in.

"...While our forecast is that a 5% OCR will get the job done, the potential for ongoing positive inflation surprises (particularly via labour costs) shouldn’t be discounted.

"Indeed, the [September quarter] read on the labour market was worryingly tight, with records broken all around and recent business survey data from the NZIER’s Quarterly Survey of Business Opinion showing labour as a limiting factor ratcheting up to record levels in Q3."

For the RBNZ to unlock "inflation target achieved" status, they need softer domestic demand to translate into softer demand for labour, the economists say.

"Without that, the wage-price spiral continues, core and domestic inflation pressures remain too high, and the OCR will need to be lifted even higher."

That’s exactly how the data have evolved over the past 18 months or so, they say.

"And we’re not yet convinced domestic and core CPI inflation has stopped surprising on the upside."

Wage growth is where "the rubber meets the road" for the "sticky domestic inflation pulse", the economists say.

"And with average hourly earnings surprising all forecasts in Q3 at a record high of 8.6% y/y the RBNZ should be worried about just how developed the wage price spiral has become.

"Some large retail-sector wage settlements of late have been well into double digits, and have the potential to be the new benchmark for upcoming negotiations."

The ANZ economists say it is important to note that "not all wage growth is created equal".

"At one end of the spectrum you have wages chasing their tail: that’s when higher wages lead to higher prices, which then get factored into wage negotiations.

"This is the end of the spectrum you don’t want to be in, as while wage growth in this scenario is good insofar that it prevents inflation from eroding real household incomes, the improvement in real incomes is likely to prove fleeting as inflation persists at high rates.

"But that is unfortunately a fair description of the current wage-price spiral dynamics we are seeing.

"At the other end of the spectrum, you have wage growth driven by improving labour productivity. In this case, a given amount of labour input yields higher output for businesses, who can then afford to pay a higher wage, while not having to increase their prices.

"Households get the benefit of higher wage growth without the self-defeating flow-on effect on inflation eating that up. But while improved labour productivity would be a wonderful thing right now, it’s not an easy thing to generate.

"In fact, productivity has taken something of a hit in the wake of the pandemic, and that’s just made the inflation problem worse."

While CPI-adjusted income is now back in positive growth territory, many households out there will be finding the rising interest rate environment a significant challenge, the economists say.

"Indeed, any household with a high debt-to-income ratio will find it relatively hard to hide from the impact of rising rates, with strong income growth providing only a partial offset. And given typical re-fixing lags, the peak impact for these households is yet to come."

But so far, there is little evidence to suggest that a "meaningful lift" in forced house sales is underway, they say.

"In fact, new listings data for October were unseasonably weak, suggesting potential sellers are choosing to wait it out.

"All else equal, this will be keeping growth in inventories contained (as house sales slow), keeping the market tighter than otherwise and preventing prices from falling as much or as fast as they would if listings were higher.

"It’s all been a very orderly adjustment so far, with very little blood on the floor. While around 2% of households are currently in negative equity, these remain, on the whole, paper losses."

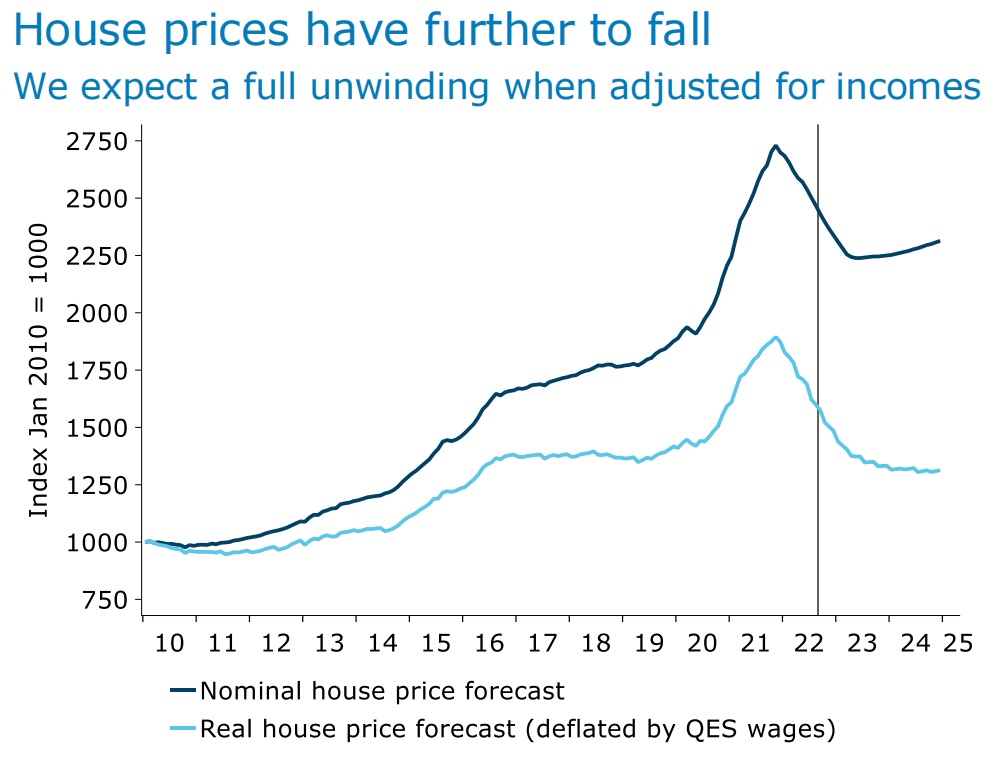

But for house prices, there’s still no escaping the fundamentals, the economists say.

New housing supply is much higher than new demand, housing inventories are at a six-year high, affordability (as measured by house prices relative to incomes) still has a long way to go to get to half-respectable levels, and debt-servicing costs are still lifting.

"We see this culminating in around a 18% peak-to-trough decline in house prices, or 27% when deflated by [Quarterly Employment Survey] wage growth.

"In income adjusted terms, that’s a full unwinding of the pandemic stimulus / FOMO [fear of missing out] driven bump."

Whether or not New Zealand avoids recession remains a line ball call, the ANZ economists say.

"But it’s important to note that not all recessions are created equal.

"A recession that brings about a transition from the currently over-stretched economy towards sustainable expansion, while also avoiding a significant household income shock, may not be as bad as the R-word sounds, particularly from a long-run economic stability perspective.

And if it means squashing the current wage-price spiral before it necessitates even more aggressive action by the RBNZ, then it may be a cost worth paying.

"One way or another, the economy needs to find its way to a sustainable path. Price (and economic) stability is at stake, and so too is very hard-won central bank credibility. Hopefully a 5% OCR is enough to get the job done."

24 Comments

There has been no significant change to policies since Covid lockdown to indicate migrant workers can solve genuine skill shortages.

Bringing in a handful of tradespeople, doctors and engineers on top of tens of thousands of business students, cooks and admin workers each year is going to produce worse outcomes in terms of high basic costs and poorer living standards for all, as it has in the past few decades.

Spot on but businesses want to cut costs (need cheap labour if materials are increasing due to global prices) to make even bigger profits which a lot of just end up offshore lol.

Lets keep the borders shut and keep the wages rising. Need to try reduce some of our huge debts so inflating it away is a great idea lol.

2022 has been a great year for potential first home buyers, houses getting cheaper and wages rising more than inflation.

People need to realize our inflation rate lowered last quarter, look at the US, UK & AUS all with higher inflation than us and lower wage growth.

I know who I would rather be.

Inflation isnt going to come down here if global inflation is still running rampant lol. Thats even with lower wages!!!! We are way too reliant on imports.

Got to love it --- blame the whole thing on the poor wage slaves gettign rises LESS than costs go up -- its up to the Slaves to take a haircut first on pay to get inflation down and be patient

Shit - how about Banks , Oil Companies, Pollies, gravy train wellington consultants all start by taking a massive cut in their trough !

how about Banks , Oil Companies, Pollies, gravy train wellington consultants all start by taking a massive cut in their trough

And they certainly will because they have a social license to operate.

Kudos to Cindy's PR spin agents, who unlike her project delivery team, have pulled their weight quite well in coming up with these catchy terms.

Sharon's masters run NZs biggest residential loan book. About 69% of ANZs total lending.

on 20th July 2016

The chief executive of New Zealand's largest bank has warned that house prices are over-cooked and the market may face a "messy end".

Well we are now at the wall, the can is not going any further. Interesting how everyone is so confident that things will not get too messy now we are here. Prices have moved up a lot since 2016, if we fall back to the OVERCOOKED levels of 2016 , what happens, what happens if prices move down from there to affordable DTIs.

Labour market correction = hard landing.

If you work for someone else there is always risk of job loss. If peeps dont like it simply start their own biz..easy enough in nz for most people if they want job security and financial freedom.. simply take the risk.

Those that have escaped and started their own business are currently forced to pay higher and higher wages to their staff as there arent enough job seekers for them to employ instead. So they raise their prices and pay the staff more. And thus domestic inflation surges.

To get more job seekers and break the cycle we need more unemployed people. Not a lot.. just enough. Right now the economic .arket is running way too hot (mainly due to orr and robertson handing out free cash, printing too much miney and giving almost interest free loans and mortgages for too long).

Basic capitalism.

We should have had a minor downturn 5 years ago.. but the powers that be decided to keep the upward trend moving upward at all costs.. and now we need to force a bigger downward trend to prevent inflation getting out of control and a huge economic crash and majir social unrest.

Just on this: A huge chunk of small-business lending for things like business assets is secured against - you guessed it - residential property! So if you lose your job, can't keep your mortgage and have to sell, then you've got nothing to secure lending against to start your own operation if there's a whack of seed capital required.

The cancer that is residential property bias has long long dendrites. We don't appreciate that yet because it hasn't mattered in a negative way until now. It's going to.

You are missing the point though in reality, Wage growth isn't the cause of this inflation it is the effect.

No way prices are coming down any time soon with international prices rising so quickly!

Do you think we are better served with more unemployed soaking up tax payer dollars + lower wages for the working but prices still going up but just a bit slower?

Small business included if they don't have customers who can afford their good or services they are worse off than they are now!

"In their quarterly economic outlook ANZ economists say the Reserve Bank 'should be worried' about how developed the wage price spiral has become"

One does not have to be an expert when wages are going up not by 2% or 4% but by 12% like countdow.......

It is an open and shut case.

Agreed. Wage and price spiral is well under spinnaker. Shudder to think what interest rates took to shut this off last time it did so in the early 80s. Look here for clarification...

https://teara.govt.nz/en/graph/23100/interest-rates-1966-2008

ANZ can assist the RBNZ achieve their goals with a SACK and FREEZE strategy.

They can simply SACK a large amount of staff and FREEZE any remaining ANZ staff wage increases and directors compensation...

Oh wait... it's better just to tell everyone else what the problems are!

We welcome your comments below. If you are not already registered, please register to comment.

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.