The Reserve Bank (RBNZ) is conceding that the current inflation pressures could have been lessened if it had tightened monetary policy earlier last year.

This is one of the findings in an extensive five-year review - a 'report card' of the RBNZ's monetary policy that was released by the RBNZ on Thursday. The report has identified nine technical areas for improvement.

The RBNZ says the review has found that the easing in monetary policy during the Covid-19 pandemic was "warranted and worst-case economic scenarios were avoided".

However, it says while monetary policy decisions have been consistent with the economic data available at the time, "with the benefit of hindsight, it appears that monetary policy should have been tightened earlier in 2021".

"For example, the [RBNZ Monetary Policy] Committee could have supported an earlier tightening in monetary conditions by explicitly endorsing a lower volume of weekly asset purchases, reducing the overall size of the LSAP [large scale asset purchase] programme, and/or stopping the programme earlier.

"Likewise, in hindsight, the Committee could have raised the OCR [Official Cash Rate] earlier.

"Importantly, however, beginning the monetary policy tightening earlier in 2021 would not have fully offset the strong inflationary impulse stemming from a series of supply shocks, including Russia’s invasion of Ukraine."

The National Party's finance spokesperson Nicola Willis was scathing in her assessment of what she described as "the Reserve Bank's marking of its own homework".

"The report, written by the Bank’s own staff, hints at mistakes that have worsened price increases and the cost of living crisis, but fails to say whether those mistakes were avoidable and if so who should be held accountable for them?

"Those mistakes include over-doing the scale of money-printing, not lifting interest rates earlier and designing the Funding for Lending Programme so badly that commercial banks are still receiving ultra-cheap money when that no longer makes any economic sense." Willis's full statement is attached below.

The review said that during the first half of 2021, the MPC considered that inflationary pressures emerging from international sources "were likely to be transitory".

"For much of 2021, central banks globally struggled to determine whether global inflationary pressures were likely to be transitory or more persistent. This assessment was complicated by repeated pandemic-related shocks and the repercussions of the war in Ukraine in 2022.

"Like the Reserve Bank, none of the other main forecasters in New Zealand foresaw the strong inflation increases that have occurred since early 2022.

"As early as May 2021, the Committee began reporting on the risk of relative price changes leading to persistent inflation. This was earlier than most other agencies that made similar assessments.

"However, the Committee only stopped assuming inflationary pressures would be temporary in November 2021, and explicitly stated that price pressures were expected to persist in February 2022."

The RBNZ also says the funding for lending (FLP) programme giving banks access to billions of dollars of cheap funding, which was introduced in late 2020 could have been done with more flexibility.

"Recognising the importance of being credible and consistent, the Committee kept the FLP in place as a source of funding for commercial banks until December 2022, as originally specified," the RBNZ says.

"However, because economic activity improved faster than anticipated, in hindsight, the FLP could have been designed with more flexibility.

"For example, the inclusion of an early termination clause with reasonable notice in the event of changed economic conditions could have been included, although such an amendment could potentially reduce the effectiveness of the FLP."

The review also estimates the impact of the deployment of the so-called 'additional monetary policy tools', or AMP. These included the LSAP and FLP programmes. The estimates suggest these tools have had an upward effect on inflation.

It suggests that AMP tools had "a peak impact" on interest rates equivalent to a cut in the OCR of around 90 basis points.

"Simulating the effects of a 90 basis point cut in the Reserve Bank’s core macroeconomic model gives an approximate indication of the macroeconomic impacts of AMP tools," the review says.

"Within this model, with all else equal, the peak impact of a 90 basis point cut in the OCR would: increase the output gap by around 0.6 percentage points, increase annual CPI inflation by around 0.5 percentage points; and reduce the unemployment rate by around 0.3 percentage points."

The review also talks about the 'neutral' interest rate (most recently identified by the RBNZ to be about 2%), which is perceived as a rate that is neither stimulatory nor contractionary. The review suggests that going back several years the RBNZ's view of 'neutral' was too high and this led to our interest rates being kept higher than they should have been, leading to lower inflation levels than would have been the case otherwise.

"The Reserve Bank’s tendency to over-estimate short-term interest rates may reflect uncertainty in calculating the neutral interest rate. As noted above, the neutral interest rate is the rate at which monetary policy is neither expansionary nor contractionary," the review says.

"It is determined by inflation expectations, and long-run global savings and investment behaviours.

"The neutral rate is not directly observable and estimates are prone to uncertainty and revisions in light of new data. If, while easing the OCR, the Governor or the Committee perceived the neutral interest rate to be higher than it actually was, then monetary policy settings would likely be less stimulatory than intended.

"While the OCR remained below neutral from 2016, there were times – particularly during 2017 and 2018 – when ex-post analysis indicates that the neutral OCR was falling further than policy-makers believed to be the case at the time. As a result, monetary policy was, in effect, somewhat tighter than intended. This may have contributed to the subdued inflation that New Zealand experienced through the first half of the review period."

The report briefly refers to the RBNZ's decision to remove the loan-to-value-ratio (LVR) restrictions as of May 1, 2020.

It said that in December 2020, "as house prices accelerated and financial stability again appeared under threat", the Reserve Bank began consulting about re-instating loan-to-value ratio (LVR) restrictions on high-risk lending. These restrictions came into effect from 1 March 2021.95 Soon after, the Committee stopped increasing monetary stimulus, beginning with a halt on further LSAP purchases in July 2021.

Separately, it says that in the early stages of the pandemic, the Reserve Bank and most other forecasters expected house prices to fall.

"On balance, lower growth in the population and in household incomes was expected to outweigh the effects of lower interest rates, an easing of loan-to-value ratio restrictions, and weaker construction activity. At the beginning of the pandemic, the Reserve Bank’s baseline scenario was that house prices would fall by around 9% over 2020. Instead, house prices increased 17% during 2020."

These were the nine areas identified for improvement:

Monetary policy formulation

1. Develop broader insight into the impacts of supply shocks on inflation

2. Develop new sources of data for economic monitoring

3. Develop better measures of ‘neutral’ interest rates

4. Understand the future role of fiscal policy instruments in managing economic shocks

5. Refine the measure of ‘maximum sustainable employment’

6. Use LSAPs to mitigate financial market dysfunction

7. Be cautious in providing forward guidance in uncertain times

Monetary policy implementation

8. Maintain the OCR as the preferred tool for setting monetary policy

9. Maintain operational readiness for AMP tools

The main review document is here.

This is the statement issued by the RBNZ:

The Reserve Bank’s review of its monetary policy decisions for the period 2017-2022 was published today, including reports from two independent international experts.

Reserve Bank chairman Professor Neil Quigley says the report is robust, identifying what went well and where there are lessons for the future. “In publicly holding ourselves to account in this review we’re continuing in our tradition of learning as an institution. I would like to thank our international peer reviewers, who also provided a critical and independent assessment to ensure our lessons are robust.”

RBNZ Governor Adrian Orr says “the period reviewed was uniquely challenging, with the global economy responding to globalisation and more lately fragmentation, technological change, declining global interest rates, plus the COVID-19 pandemic and war in Ukraine.

“I am extremely proud of the dedication the team at Te Pūtea Matua displayed, and the outcomes achieved. There is much for us to learn from the conduct of monetary policy during this period, and the review identifies nine areas of focus for improvement, which the Reserve Bank is progressing.”

The review finds that monetary policy decisions were consistent with the data available at the time. The easing in monetary policy during the COVID-19 pandemic was warranted and worst-case economic scenarios were avoided.

Reserve Bank Chief Economist Paul Conway says “the current heightened level of inflation could have been lessened at the margin by an earlier tightening in monetary policy in 2021. However, while we are facing some serious economic challenges, the New Zealand economy has weathered the economic storm created by pandemic and war relatively well. Inflation and unemployment are both low compared to the vast majority of OECD countries.”

Officially called the Review and Assessment of the Formulation and Implementation of Monetary Policy (RAFIMP), this is a five-year review about how the RBNZ has made decisions about monetary policy in the past five years and how those decisions were brought into effect. This is the first such five-year report since it became a legal requirement with amendments to the Reserve Bank Act in 2018.

This is a link to the RAFIMP page on the RBNZ website.

The RBNZ describes RAFIMP as "a detailed report card on what the Monetary Policy Committee (MPC) decided to do, what worked, what we could have done better and how we can learn from our experience".

"RAFIMP is a review of how we have made decisions about monetary policy in the past five years and how those decisions were brought into effect. This is the first time we have done this review — after it became a legal requirement in 2018. However, we have been carrying out regular reviews of monetary policy to hold ourselves accountable for our actions."

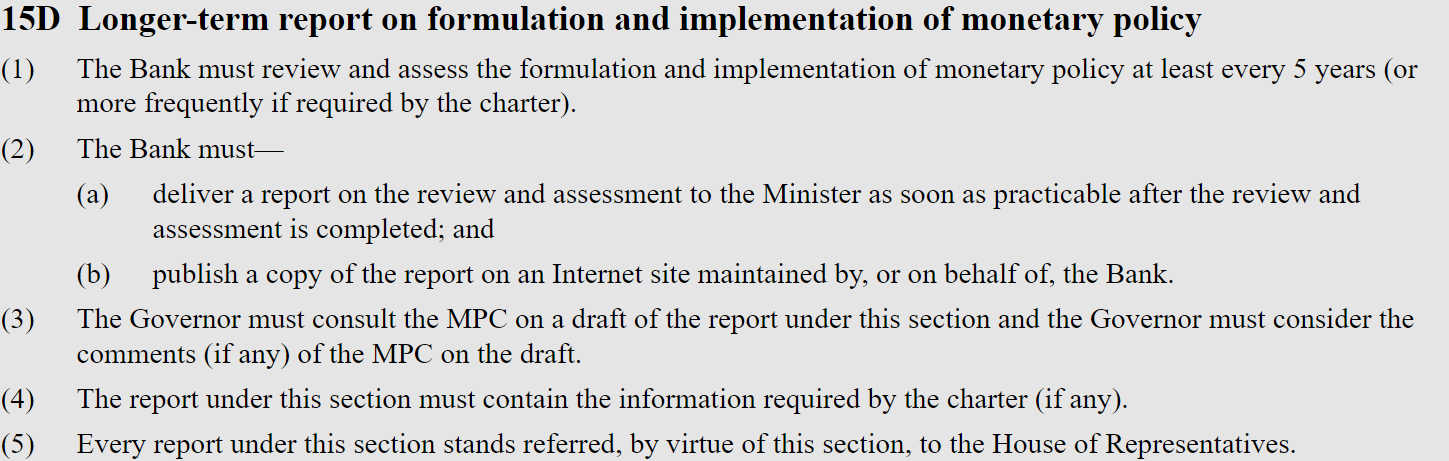

A detailed outline of what's required from RAFIMP, taken from the RBNZ legislation, is appended at the bottom of this article.

Two international independent experts on monetary policy have peer-reviewed RAFIMP. These experts are, and with links to their reports:

- Warwick McKibbin — Professor at the Australian National University

- Lawrence Schembri — former Deputy Governor of the Bank of Canada.

This first report has arguably taken on more significance than might have been expected back in 2018. That's because of the extraordinary measures - stimulatory measures - that the RBNZ has been involved in since the onset in 2020 of the Covid pandemic.

While RAFIMP covers the Monetary Policy Committee’s decisions on the Official Cash Rate (OCR), it also includes new Additional Monetary Policy (AMP) tools that were introduced during the pandemic. These of course include the Large Scale Asset Purchase Programme (LSAP) through which the RBNZ ultimately bought about $53 billion of government bonds and the Funding for Lending Programme, which to date has provided the banks with $16.4 billion of cheap money priced at the level of the OCR.

Extra significance still has been given to the report by the fact that Finance Minister Grant Robertson just this week has re-appointed the polarising figure of Adrian Orr as Reserve Bank Governor, something that prompted howls of protest by the opposition who were against Orr getting another five year term ahead of next year's election. The believed he should have been re-appointed (after his current term expires in March 2023) for just a year, so, that an incoming government next year could choose a new governor.

This is the statement from Nicola Willis:

The Reserve Bank’s self-assessment of its own performance fails the credibility test, says National’s Finance spokesperson Nicola Willis.

On Thursday, the Bank released Review and Assessment of the Formulation and Implementation of Monetary Policy.

“Predictably, the Reserve Bank’s marking of its own homework pulls its punches and fails to deliver any accountability for mistakes in the management of the New Zealand economy,” Ms Willis says.

“The report, written by the Bank’s own staff, hints at mistakes that have worsened price increases and the cost of living crisis, but fails to say whether those mistakes were avoidable and if so who should be held accountable for them?

“Those mistakes include over-doing the scale of money-printing, not lifting interest rates earlier and designing the Funding for Lending Programme so badly that commercial banks are still receiving ultra-cheap money when that no longer makes any economic sense.

“These errors matter to every New Zealander. When the Reserve Bank gets it wrong, we all pay, with inflation and interest rates being higher for longer than they might otherwise have been.

“Kiwi families – already struggling with runaway inflation – are now being squeezed by hundreds of dollars a week in higher mortgage payments. We need to know whether that pain could have been reduced.

“This report could never answer the most vital questions because it was written by the people responsible. In fact, the Minister of Finance reappointed the Reserve Bank Governor for another five years even before publishing this report.

“National again repeats our call for an independent inquiry into the monetary policy response to COVID-19. This is about learning lessons for the future and upholding basic standards of accountability. New Zealanders deserve no less.”

The legal requirements for RAFIMP:

63 Comments

Yes honestly - for years people have been predicting a meltdown and they could have done something about it, but nothing. Now it seems like they cant turns the taps fast enough regardless of the impact it is having. Maybe he has a kink for steep lines on graphs.

Can someone smarter than me find out what Orr is investing in and how much money he is making out of all of this.

That's true, not many investments offer guaranteed $550K + (assuming a more reasonable salary of $250K) for five years. And all the prick needs to do is bump up rates as he sees fit with complete disregard for any of the advice given to him before this mess. Orr is a joke.

Seems pretty common, even on here, for people to ascribe our current inflationary environment to central bank and government actions.

It's a contributing factor, but the shit show is really due to extenuating events as you have mentioned.

The worst thing reserve banks may have done is prop up a continued period of growth so the market and it's individuals have become to secure when taking on risk. Only makes responding to adverse conditions that much harder.

If the external factors were unavoidable then getting the bits we could get right right was even more important.

Using the fact they happened as a shield for the mess we have now is defending against something that no one was seriously suggesting in the first place.

getting the bits we could get right right was even more important.

Given we seem under resourced on any given day just to uphold the status quo, thinking we would ever have a highly effective disaster mitigation infrastructure for all the various potential pitfalls is fairly ambitious.

I can still see in the commercial realm a level of disorder given the changed nature of the world. They'll be around for years to come. Sometimes they're excuses, other times it's just how it is.

If we apportion fault when really it's no one fault, that allows us to abdicate responsibility to no one.

When I say 'the bits we could get right', I mean things like not uncorking investor LVRs, not running FLP long past the point of sanity, not leaving the OCR on the floor - the RBNZ specific bits.

These are decisions made by a committee. That committee should bear collective responsibility, which along with accountability, used to be an established governance convention that we don't see a lot of these days. No infrastructure required or need to link the non-RBNZ decision process with external factors. We're talking about the quality and speed of decision making.

If the decisions don't ultimately matter and no one is responsible for them, then what are you paying people for? Just flip a coin or something.

That's collateral damage. The alternative was economic hardship followed by a period of rising inflation. Maybe that would've been better, high unemployment, high inflation for 2020 and 2021, then the RBNZ starts stimulus about now, and you get less asset appreciation because everyone's optimism has spent 2 years getting obliterated.

In future, maybe we will have better tools, like direct money transfer to citizens rather than via interest rates and giving money to employers. They'll come with their own interesting consequences.

Yes but we now have a massive house price bubble at precisely the time we need to raise the ocr to stop people spending.

Thus the likelihood of a massive crash in house prices is far greater than it should be because they are so ridiculously overvalued.. all due to the ocr being too low too long (and the rest of the rbnz actions.)

I see this report as being something mainstream media should have on the front page for weeks... in the uk the tabloids would want blood (via a dumbed down version of the story everyone would understand)

"I see this report as being something mainstream media should have on the front page for weeks... in the uk the tabloids would want blood (via a dumbed down version of the story everyone would understand)"

Precisely, which begs the question, are they being influenced, ignorant or do they know something we don't?

Yes just like everyone has been saying for YEARS - it went so far past the point of making sense that people gave in and made decisions they should have never had to had Orr has any sense of decency or understanding of economic systems. The printed money, the low interest rates, the blind eyes turned while everyone was telling them this isn't good and not going to end well. And now here we are.

I have said it once and will say it again, the gov, or reserve bank, I dont even care who, needs to put policies in place for future generations so that if rates drop this low again the minimum repayments stay at a more reasonable level such as 5%, and the extra in the payments made go straight to paying off the loan faster. How much better off would we be as a country if they had of implemented this 5 years ago? No property bubble, limited inflation, steady as she goes. But nope - $800K and Orr still cant think outside of the box.

Going into the Covid19 lockdowns & restrictions , we had a robust economy ... and a long era of rampant house prices ... we had no demand side issues ...

... does the RBNZ not understand this ... Keynesian pump priming of the economy is called for during deep recessions & depressions ...

We've endured supply side shocks since Covid19 arrived ... that , coupled with flooding the economy with cheap credit has led to ? ... Adrian ! ... you boy , answer the question ...

"They" spent a decade and more trying to encourage Inflation - to no avail. Then, Covid came along. An opportunity not to be missed, and they didn't.

Once interest rates hit 0%, something else had to be tried. Conspiracy Theory? Perhaps, but it looks like it's worked.

As Richard Guest said on Hosk's show this morning , central banks have been like someone standing in a shower cubicle ... you're turning the hot tap , nothing comes out ... turn it some more , still nothing ... you keep turning ... then suddenly , shit hot , you're scalded by a blast ...

Yes agree but it has also put the country in a position where it is dependent on low pay and high house prices. Now they have got us here they need to work out how this mess can be smoothed out over time. Orr, the master of doing nothing, is all of a sudden the most reactive man on the planet. In my mind the Reserve Bank and Orr on his $800K salary should be able to see issues coming and act before they become issues. If they are only reactive I am pretty sure we could take someone with no skills or education off the benefit and give them the simple task of increasing rates based on inflating increasing. It's not hard if the job is reactive but it should never be that way.

Huge and bleeding obvious mistakes were made while they held press conferences and laughed about asset bubbles.

Economic vandalism and reckless incompetence was the order of the day.

The organization has been stacked with political diversity hires instead of competent economic experts.

Nothing has been learned and nobody is being held accountable.

... exactly ... within NZ financial circles the RB is a laughing stock ...

We were dealing with a nasty flu bug FFS ... we weren't in a deep depression or grinding through a protracted world war ...

... the economy didnt need Orr & Robbo to overdose it with credit ... least of all the housing market , that was already up in ga-ga land ...

"Likewise, in hindsight, the Committee could have raised the OCR [Official Cash Rate] earlier.

Rate hikes are not, in and of themselves, restrictive of inflation or even the economy. Why would they be? Companies which perceive high nominal return opportunities aren’t going to be dissuaded by a few additional points on borrowing costs. If the profit is there, what difference the interest rate?

Furthermore, those who make the loans are only more willingly to do so, given higher interest potential. Link

"a detailed report card on what the Monetary Policy Committee (MPC) decided to do, what worked, what we could have done better and how we can learn from our experience"

If they had learned they would have sacked Kaumata Orr the other day as opposed to giving him an extra 5 year tenure.

All of us could see the inflationary pressures the second they announced the COVID spending in 2020, and the need to start the slow OCR creep then.

"LEARN FROM OUR EXPERIENCE"??

What is this the monetary policy training ground? Pretty sure Orr is supposed to have the experience to avoid issues, not react to them.

The whole situation is so frustrating, hence the many comments - sorry people but it finally feels like everyone in charge has finally woken up from their deep sleep and realised how bad things have gotten and only now are they doing something about it. The people should be FURIOUS over this. Orr should be marched into his managers office and given a shakedown and told to do better. Instead he gets a pat on the pack and another $4 million over 5 years. YES $4 MILLION of taxpayer money, taken from the people that will be doing it very tough over the next 5 years, to pay for this clown to make a mess of everything.

I see homes.co.nz still has a vastly over optimistic price for my house about 12 - 15% over what I would believe it would sell for. One roof and my banks valuation seem to be about right . Why is that? With homes.co.nz I see that agents can alter the estimate of properties they are marketing, maybe placing the estimates too high? So would this then affect the estimates of the surrounding properties and push them up to unrealistic levels in the homes.co.nz algorithm?

Surely it would cost less than $800k to develop an AI reserve bank governor that just puts the OCR up or down based on inflation? Added plus side of being able to program it not to talk to trees either.

Was discussing this y'day. Shouldn't the central banks be run by AI and algos? The way things are run seems to be quite archaic.

Luxon is showing interesting signs, in looking at making RB Gov a new government position. It's a bold attack on reserve bank independence. Brazin polictization of it's independence to manufacture economy results that suits the then government in looking for reelection.

What confidence can the market have if Governor can be changed at will by PM of the moment?

https://www.nzherald.co.nz/business/reserve-bank-open-to-being-made-to-…

Plus, everyone has a job who wants one.

By providing additional stimulus, AMP tools contributed to higher-than-otherwise economic activity and inflation in the economy during the COVID-19 pandemic, consistent with the Committee’s objectives. However, with significant uncertainty over the strength of the transmission channels, it is difficult to accurately quantify the net economic benefits of these programmes. In contrast, the marked-to-market cost of the Reserve Bank’s holdings of government bonds bought under LSAP is relatively straightforward to measure.

The review also estimates the impact of the deployment of the so-called 'additional monetary policy tools', or AMP. These included the LSAP and FLP programmes. The estimates suggest these tools have had an upward effect on inflation.

It suggests that AMP tools had "a peak impact" on interest rates equivalent to a cut in the OCR of around 90 basis points.

"Simulating the effects of a 90 basis point cut in the Reserve Bank’s core macroeconomic model gives an approximate indication of the macroeconomic impacts of AMP tools," the review says.

by Audaxes | 23rd Feb 22, 7:47pm

Here’s what, oh, the Reserve Bank of New Zealand (RBNZ) has to say about LSAP effectiveness:

When we buy assets, this increases their price and so reduces their yield. That means the interest rate, in this case on government bonds, fall. This has the effect of ‘lowering the tide’ on other interest rates in the economy, particularly longer-term interest rates of two years or more. It also reduces the cost of borrowing for households and businesses…

LSAP programmes have been conducted in the euro area, Japan, Sweden, the United Kingdom and United States.

The evidence shows LSAP proved effective in providing much needed support, lowering long-term interest rates and exchange rates, and underpinning economic growth and inflation.

Studies found the government bond purchases worth 10 percent of GDP have, on average, lowered 10-year government bond yields by around 50 basis points. [emphasis added]

It’s true; many academic studies from around the world focusing on different program types in different places have come to similar conclusions using all kinds of regression analysis. They find that QE programs do correlate with falling interest rates; maybe even “around 50 bps” (the “around” part means rounding up).

Even if we take them at their numbers, and presume correlation equals causation (because, they’ll tell you, they do account for the difference when regressing variables), you should still end up wondering why they even bother with this stuff.

In the removal of the LVRs we had the admission that in NZ the property market IS the economy. There was no reason to do it other than enrich the politocrats heavily invested. When you understand that, then the fact that the FLP is still in place is not surprising.

Both actions are corruptions for which jail time should be the answer, not renewed contracts. How can you get a review that says they over stimulated yet the FLP is still in place.

It's like piloting a hot air balloon, you've got to be thinking far ahead when you boost the burners or shut off the flame, the effect is delayed and not instant. You're in control of the second derivative, if you want to be technical.

For that reason, the current interest rates rises are already enough. Just got to wait 6 to 12 months for the new rates take effect -- and they will -- as people roll off their 1- or 2- year fixed rates.

Don't overcorrect in the other direction by continuing to raise rates, or this article about how the RB should have acted sooner can be republished as it is in 12 months from now, just change each word to its opposite: "increase" to "decrease", "tighten" to "loosen", etc.

Their "report card" is measuring the wrong stuff.

Bernard Hickey put it so well yesterday:

When a supposedly independent financial institution works hand in glove with a politician to change the wealth distribution of a nation AND fails to achieve its one clear legislated target, then it has a social license and a credibility problem.

Re worse case avoided? We've only just begun. They think this is going taper off and everything will normalise.

Are any of these supposed analysts and experts aware of the current global geopolitcal situation? How can they make such a claim.

Under these Be Kind Authoritarian Regimes we printed more money than has ever been printed. Adding to already pre existing post GFC printing bubble. This money is only now appearing and the global instability it will bring, will make the GFC printing caused Arab Spring and ensuing and ongoing migrant crisis look like a walk in the park.

Clearly these people are just trying to keep selling as good a picture as they can to make sure it doesnt sink too much on their watch. Hoping the can lands when their tenure is done so they can blame the new people.

Our journalists make me so angry

So true.

The worst case is only just beginning. Average houses cost a million bucks, but are really only worth ~400k. Everyone in debt up to their eyeballs from purchasing rapidly depreciating "assets", with inflation and interest rates spiraling out of control. Aussie banks sucking record profits out of NZ. Epic recession/depression incoming.

"Worst case avoided" my @%$€.

Its why they are drawing a line under all this before everything really turns to custard.

Then they will say the whole low ocr/money printing thing was already reported on and shouldnt then be part of a second investigation into why our housing.market and economic crash was so much worse that others

At least they are having some introspection and admit they could have done things better. It seems as though that is rare in the current age:

Hillary Clinton: I was perfect, Americans are sexist

Trump: I was perfect, The election was stolen from me by fraud

Efeso Collins: I was perfect, Aucklanders are racist

We welcome your comments below. If you are not already registered, please register to comment.

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.