A survey the Reserve Bank pays close attention to has shown another sharp rise in the expected levels of future expectation in an indication that the central bank is not yet seen as getting inflation under control.

The results of the latest Survey of Expectations, carried out quarterly for the RBNZ, are likely to carry a lot of weight with the central bank in making its next decision on the Official Cash Rate on November 23. At the moment the OCR is at 3.5%.

The key result in the survey is that the expectation for inflation in two years' time - the most watched measure in the survey - has risen very sharply to 3.62% from 3.07% three months ago. If this expectation came to pass it would mean inflation would still be outside of the RBNZ's targeted 1% to 3% range by the end of 2024.

And of course it would be well above the RBNZ's explicit 2% target.

But even looking further forward, there's not much encouragement for the central bank.

According to the latest survey the expectation in five years' time is that inflation will be on 2.44%, up from 2.33% in the survey three months ago.

As for the story looking 10 years out, well the latest survey has an expectation of inflation at 2.18%, up from the previous survey figure of 2.13% and of course again above the explicitly targeted 2% figure. In 10 years time.

Westpac senior economist Satish Ranchhod said the strong increases in the survey "will no doubt be a worrying sign for the central bank".

"Interest rates have been on the rise for over a year now. However, underlying inflation is not showing signs of easing. And now, with inflation expectations pushing higher, there’s a risk that the inflation cycle could be even more protracted. That’s because expectations are a key input into how businesses adjust wages and prices, and their creep higher signals ongoing price pressures over the year ahead.

"We’re forecasting a jumbo-sized 75bp [basis-point] rise at the RBNZ’s next policy meeting on 23 November. Today’s strong result means that sort of extraordinary rate rise is even more likely," Ranchhod said.

The data for this survey was obtained from 33 business leaders and professional forecasters by the Nielsen group on behalf of RBNZ. Field work for the survey was run between the October 19 and 25, 2022.

As stated above, the key survey statistic is what the surveyed experts view inflation will be in two years' time. The RBNZ is always looking for expectations to be 'anchored' around 2%. Recently as actual inflation has taken off these expectations have become seriously unmoored and have risen rapidly.

Since the last survey results came out in early August there's been release of GDP figures in September, inflation figures in October and labour market (unemployment and wages) figures just last week. The last of those three data releases was not released before this survey was actually conducted, but the inflation figures most certainly were.

All of that data was 'hot', mostly surpassing expectations of economists with the sheer strength of the figures. For its part the RBNZ got very close to picking the GDP number, missed by a long way on inflation and had unemployment figure right and was closer than anyone on wage rises - but still came in slightly too low with its private sector hourly earnings increase figure that other economists had tended to look at with raised eyebrows because it was so much higher than other people's picks.

But of course in all this data it's the unpleasant inflation surprise that's truly the biggie - and has led to the kind of result we've seen in this latest survey.

In many respects this survey series can increasingly be viewed as a measure of the RBNZ's credibility in achieving its inflation target.

What the current results are telling you is there's doubt out there that the RBNZ is on track to rein in the inflation beast. Confidence has been knocked. That's a bad thing because if people don't believe that the RBNZ can tame inflation then we will see future price setting behaviour incorporating ongoing expected levels of high inflation. And this can be self-fulfilling.

It's another complication in already complicated scenario for the RBNZ as it decides what to do in its November 23 Official Cash Rate review. And of course yet another complication is the fact this is the last OCR review for 2022 and the next one's not for three months - on February 22, 2023.

Most economists are juggling between picks of either a 50 basis point rise for the OCR or a 75 point rise. Personally, I think these survey results - which will have a big influence on the RBNZ - make at least a 75-point rise a slam dunk. I do still think there's some chance we will see a 100-pointer.

101 Comments

“As of now, we can’t see the fifth dimension, but rather, it interacts on a higher plane than we do. It’s because of this that we can’t really study nor fully prove it’s existence.”

I see your point TTP. Orr has no idea how to study or understand it. Great comparison!!

Rbnz strategy... Ask others what they think inflation will be and then run with that. Never mind that Orr is paid big bucks to at least have some idea himself. This Muppet just got reappointed for another 5 year term. If National win and then want to replace Orr, they will have to pay out his contract. Ridiculous politicking by robbo

A 75 bps raise is totally insufficient.

At the very least, a 100 bps increase must be enforced, together with an express statement by the RBNZ that a similar move will follow up in February, so to bring the OCR to 5.5%.

Anything less, and Orr will be forced to raise to a higher peak later on. If the RBNZ does not act with due urgency and determination, I can easily see an OCR peak of 6 or even 7% by end of the next year.

I do hope that Orr is finally getting it - even a muppet like him should by now have learned the lesson that an over-stimulatory monetary policy only creates inflation and forces much tighter monetary settings later on.

Demand impacting inflation assumes a highly competitive market, and no constraints on supply. Something we do not have in NZ on any good or service.

Domestically lack of demand is more likely to lead to lack of product rather than lower prices. Companies will just drop anything that is not selling.

We may even see prices to increase, as firms try and ensure revenue remains on track.

NZD is certainly bucking the trend. A few people were saying a month back that the NZD would be lower than 52 USD and 80 JPY by now. I remember Keith Woodford being one of them. I had mentioned that the NZD had oscillated regularly between 82 and 87 JPY for many many months and that would continue, rather than sink well below 80. And there it is back up at 87.

I don't think I made any specific predictions about JPY but I'm well off the mark with the NZD at this point, which I thought would be heading below 55c before the end of the year.

As far as the JPY goes, it made no sense for it to drop by as much as ten percent either way, but yes, definitely has upcycled against what I expected to see happen. Although I'm much less invested in it now that I've paid for my car - but there's always the next project around the corner...

We have a massive bottleneck in our country's main port (result of COVID and post covid redundancies that never recovered) and no short or medium plan to fix it.

It now does not matter what shipping costs drop internationally - they will not drop locally because of our broken supply chain.

Good post. Like all these things there’s complexity at play, with inflationary and deflationary impacts. But I would bet on the deflationary impacts outweighing the inflationary impacts of demand destruction.

Most prices won’t go down but they probably won’t go up much as demand destruction strikes.

Also I would expect to see wage inflation diminish significantly as demand destruction commences.

Businesses now have about $280 billion of loans (and rising) - the cost of servicing those loans is skyrocketing and a 75 point rise would quickly add another $2 billion a year to business input costs - taking total interest payment to around $17 billion per year.

Explain to me how increasing the costs of providing goods and services is supposed to reduce the price of those goods and services.

And, don't start with the 'zombie companies need to die' nonsense as if having less competition and more market consolidation will bring prices down.

I get the theory, but businesses won't sell 'wants' for less than the price of producing them, they will just downscale production to match the demand at the price that they want / need to charge. Downscaling often increases the production cost per unit (and therefore the price charged). Economic theory gets this last bit the wrong way round.

Kind of but business resources are so stretched that the costs of producing that last product out the gate are higher than average, effeciency actually drops when trying to do too much with too little. NZ doesn't have the size to scale effeciently like say AUS so supply doesnt so effectively increase to meet demand.

That's fair - as ever with these things, it depends doesn't it? Some businesses might see efficiency increases at lower levels of demand, some will see decreases, some will see both depending on the level of production. I guess it just makes the point that broad assumptions based on simple models are often wrong.

Jfoe, the price of a good or service is not set by how much it costs to manufacture or provide it, the price is set by what customers can afford. Higher interest rates means customers have less money left to afford said good or service, that's how higher interest rates, theoretically at least, are supposed to lower prices, hence inflation.

You see HM, it's when you make stuff up like "TA my hero" that your credibility evaporates.

You also know full well that I'm bearish about 2023, I made this very clear numerous times, I absolutely expect house prices (and other assets) to fall further in 2023.

It's just really poor form of you to make this stuff up.

Rates were always going to go up people borrowed way to much for property, now that million dollar box in Auckland is not looking such a good purchase as house price’s crash banks will still want payment even if monthly payments double. Expect to see more housing stock on the market and a acceleration in house price crash. Speculators who were left holding the bag with a number of properties will be up to necks in crap.

I think you are over simplifying it a bit there. A business can only seek higher costs until it cant. It will bring non-discretionary prices down. Staple foods wont and that's the scary part. The economy needs a recession reset. The housing market badly needs one. That means temporary pain yes but what's your alternative measure if you are opposed to lifting rates and just letting inflation run for years and years?

Exactly this.

The trouble in nz seems to be that our fixed rate mortgage mentality means when Orr raises the OCR it takes forever for it to filter through to the consumers and the economy. It is kind of like watching a car crash in slo mo.

Surely each month more mortgages and biz loans refix at a higher rate and the % of loans that are refixed (if its an average of 4 year terms thats 1/48th of the total loan holders each month)...

Because we all saw it coming odds are a ton of people renegotiated last year then that that high percentage will have 4-5 years of a good rate to run?

So... my feeling it that it will only start to bite enough people (say 40%of total loans) to have an impact by mid to late 23 and be felt on mid 24? By which time if we keep raising then the ocr might be at over 8% and inflation approx 5-6%

Just a theory. Interesting to see the numbers.

https://www.macrobusiness.com.au/2022/11/jacinda-ardern-confronts-inter…

I still think this is the most telling chart of why we are in the calm before the storm for selling pressure:

https://www.macrobusiness.com.au/wp-content/uploads/2022/11/Capture-31-…

{kind=link}

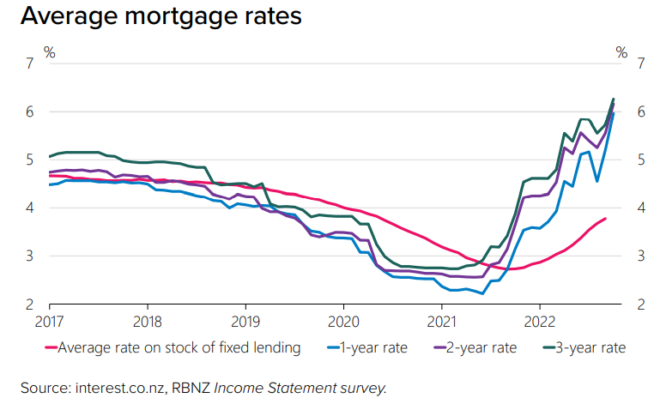

The average rate on the outstanding stock of fixed mortgages has gone from 2.8% to 3.8%~. That figure will be steadily rising over the next 6-12 months with all fixed rates looking set to be north of 6%

Also there is only a percentage (was it 21%?) of people actually holding mortgages, and not all of them will be high value mortgages ~800k+ which will limit the impact of the OCR hikes and interest hikes on households. There will have to come a time again where renting is more costly than a mortgage and the mortgage seems more worthwhile however the way interest rates are going this will be a while yet, dependent on your location in the country of course.

Not really according to Bernard...

https://www.stuff.co.nz/business/opinion-analysis/124385961/new-zealand…

Yvil NZ has some much going for it but over the last 10 years people have just been pumping up house price’s creating a huge imbalance in society a lot of money which has gone into housing could have been invested in business. All that is happening now is banks are making large profits and most of that will go out of the country and the banks have so many people in huge debt and will just cream for the top by raising rates for next however many years, they will not care if your struggling or if the property market crashes.

Yes but housing has been a sure fire bet right up until the last 6 months or so and businesses are hard work and the majority of them fail leaving you with nothing. People just go where its the least risk, just common sense really the whole system has favored housing investment based on historic data..

Mr Orr, Listen to experts in interest.co.nz (comments section :)

Go for shock treatment by raising OCR, more than what the market is expecting and this time the expectation is 0.75%, so go for full 1% as shock treatment will have the effect that even o.5% x 4 could not achieve.

The inflation we are seeing is mainly supply side, driven by energy costs one of which is manipulated by restricting production e.g. crude oil. Most people are spending most of their income on essentials. Aggressive raising of interest rates will only make things worse and crash the housing market. Banks profits will rise and be sent offshore. The only thing that will effect them is if there are too many non performing loans and house re-possessions.

I'll call this one "Monetary Policy":

Step 1) Central Planners make bed by scattering lovely cash all over the place, for decades

Step 2) Central Planners lie down on bed

Step 3) Bed is so thick and deep it begins avalanching and, eventually, catching fire

Step 4) Years later, Central Planners wake to smell of smoke and realise they have no good options due to step 1

Oopsey Doopsey

I am on 2.39% now and struggling with ill health , cost of living and may need to go on a benefit, I am a self employed ubereats driver, my income is less than $25,000 a year, my debt $200,000

My fixed term runs out in march 2023, should I break now and fix now, in your opinion.

I don't want to lose my home next year, but struggling to cover costs already.

If you go on a benefit, I believe that there are top up payments available to help with the mortgage. Not sure if the rules have changed, you could check with winz. Being self employed, you could possibly drop your hours below the benefit threshold, and get a benefit with a small top up from a few hours per week doing Uber eats.

Lots of jobs around at the moment. Perhaps you could increase your income? Or get a boarder?

Don't believe ANYONE who says they know for sure where interest rates are going.

Hundreds of thousands of people just made incorrect predictions about interest rates. People get this stuff wrong All The Time.

....having said that, I personally would break and fix for a longer term if I could afford it. Just for peace of mind. At least your mortgage is small (by today's standards).

Speak to WINZ before doing anything. You need to know what your benefit income + supplements would be in a worse-case scenario (i.e., if you have to leave work for health reasons). Then work out what level of mortgage repayments you can afford. If you have a good loan-to-value ratio, it will be in your bank's best interest to keep you in your home. For example, they might offer an interest free loan in the short term to reduce your outgoings for a period.

Yes 100% agree with the strategy, but low LVR loans are easy meat for banks to maybe not help as they are well protected by the owners' equity, ie the banks can force the sale, easily clear their debt, and get rid of a nonperforming loan in one go.

However, if there is any chance that in selling they might also lose, then they might be more inclined to help (themselves).

Always remember, these institutions are not your friends. The fact you may like what they do for you is a happy coincidence.

We welcome your comments below. If you are not already registered, please register to comment.

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.