By Gareth Vaughan

As a long-term advocate of greater competition in New Zealand banking, it's fascinating to see the drums beating for a potential Commerce Commission market study.

If you look at interest.co.nz's home loan tables you'll see there are 15 banks offering mortgages, plus a range of building societies, credit unions and other non-bank lenders. And on the deposit front you'll find deposit rates from 16 banks, plus the range of other financial institutions. So there are plenty of financial institutions operating in NZ. Yet year after year the same four big banks, ANZ, ASB, BNZ and Westpac, almost completely dominate the NZ banking market.

Contributing to this dominance are examples where successive governments, the Reserve Bank and Payments NZ, the bank owned payments overseer, have let down the New Zealand public and smaller NZ-owned banks and other financial institutions, effectively helping strengthen the dominance of the big four Australian owned banks.

This is certainly not to say this is the only factor. The sheer scale of the big four banks, operating primarily in a commoditised banking market dominated by largely homogeneous home lending and deposit collecting, gives them a big advantage. But there are clear examples, which I'll set out below, where the actions of our authorities have helped reinforce this dominance.

This has contributed to a NZ banking market described by Deutsche Bank banking analysts as a; "unique market structure, we are yet to find another one, generating oligopoly-like returns."

More sunlight needed on switching between banks

A key factor in a competitive market is how easy it is for customers to leave their current service provider and shift to another one. This is easy in NZ banking. However, I often come back to the thought that a lot of bank customers simply don't realise how easy it is to change banks.

A simple bank switching process, managed by the bank the customer is moving to, was established as long ago as 2010. Taking five business days, it was touted as the fastest in the world by Payments NZ, the organisation overseeing it.

In 2014 the Productivity Commission noted no public data was available on the number of customers moving between New Zealand banks even though banks are understood to get monthly data on the volume of customers switching between them. Such information, the Productivity Commission said; "would help demonstrate the effectiveness of the current switching process and give consumers greater confidence about the ease of switching banks - hence sharpening the overall level of competition between banks."

This data still isn't publicly available with a Payments NZ spokesman this week saying; "we don’t hold, or plan to hold, data on the number of customers who switch banks as this type of information is commercially sensitive."

Clearly it's not in the interests of the major banks, with big customer numbers, to necessarily promote the ease of changing banks. However, in the case of ambitious smaller banks you might think it would be. But I can't recall any recent campaigns by any banks promoting the ease of switching. So I asked some of the banks who might want to promote switching to see what they have to say. Kiwibank and TSB responded.

A Kiwibank spokeswoman noted it's easy, safe and fast to switch, and that there's information on Kiwibank's website for personal and business banking customers wanting to make the switch, with the bank's "customer-facing teams always here to help."

A TSB spokeswoman also said the switching process is easy.

"We haven’t promoted it since it was first introduced, but we have a new website launching soon, and this information will be part of this. At the moment we only have the step by step instructions on what to do when switching a home loan," said the TSB spokeswoman.

Here, clearly smaller banks could do more to promote the ease of moving your business to them, assuming they want it. And publicly available data, updated monthly or quarterly, on the volume of customers moving between banks, should be mandatory.

NZ a payments laggard

Payments is an area where NZ has been a slow mover. Notably shifting to processing electronic payments 365 days a year, introducing open banking, and merchant service fee regulation.

To give a bouquet alongside the brickbats, the current Government has moved to regulate merchant service fees, albeit more than 20 years after Australia did so and not to the extent I'd have liked. Nonetheless, this should directly reduce costs for small businesses that accept credit and debit card payments.

The move to 365 day a year payments, and work towards open banking, are both areas overseen by Payments NZ.

As Payments NZ notes on its website, it was formed in 2010 by the industry with support of the Reserve Bank. It governs NZ’s core payment systems and works with the industry to lead the future direction of payments in NZ. Payments NZ's shareholders/owners are ANZ, Westpac, BNZ, ASB, Kiwibank, TSB, HSBC and Citibank.

From May NZ banks are finally scheduled to begin 365 day a year payments, shifting from sending and settling payment transactions only between Monday and Friday. This won't, however, mean real-time payments where consumers, merchants, and financial institutions can pay friends and customers, settle bills, and transfer money immediately, 24/7. Alongside Israel, NZ is one of just two OECD countries without real-time payments.

Open banking requires banks to share product and customer data with customers and third parties, with the consent of the customer. The idea is that such data sharing should both increase price transparency, and enable comparison services to accurately assess how much a product would cost a consumer based on their behaviour. This could therefore enable the recommendation of the most appropriate products for individual customers.

Last November Labour's then-Commerce and Consumer Affairs David Clark announced a move towards open banking, saying this would ensure banks must share customer information if they request it, making it easier for New Zealanders to compare mortgage rates, apply for loans and switch banks. But Clark said actual implementation of open banking was still two years away.

Clark noted open banking is required of the Australian parents of NZ's big four banks, and "is a fixture" of the banking system in the United Kingdom being "a common place tool used overseas to increase competition and make it easier for customers to get better deals."

As long ago as 2017 National's Jacqui Dean, one of Clark's predecessors, was making noises about banks enabling open banking. Labour's Kris Faafoi, Dean's immediate successor, did the same. And in 2018 law firm Bell Gully weighed in saying; "strong, even urgent, political focus on open banking in other economies is currently absent in New Zealand."

With the bank owned Payments NZ in charge of the open banking standards and protocols, looking in from the outside it's easy to be cynical about slow movement in areas that could enable other financial service providers to increase competition with banks.

RBNZ tilts playing field in favour of big banks

An noticeable aspect of the Reserve Bank's Covid-19 response was how it tilted the playing field further in favour of NZ's big banks.

Major banks were at the centre of the Reserve Bank's large scale asset purchasing programme (LSAP), or quantitative easing. The QE saw the Reserve Bank buy about $53 billion worth of government and local government bonds from a range of banks including ANZ, BNZ, ASB's parent the Commonwealth Bank of Australia and Westpac.

Increasing the supply of money lowered interest rates further, providing liquidity to the banking system and encouraging banks to lend, which helped drive the explosion in bank mortgage lending and house prices in 2020-2021.

Additionally home lending banks were able to access $19 billion of three-year money priced at the Official Cash Rate through the Reserve Bank's Funding for Lending Programme (FLP). Eligible securities banks could pledge as collateral for FLP money included Residential Mortgage Backed Securities, New Zealand Government Securities, and Kauri debt issues.

Heartland Bank noted it didn't participate in the FLP because its home loan lending book wasn't big enough and the Reserve Bank had declined to include motor vehicle loans as collateral. Building societies and credit unions were excluded from the FLP, despite asking both to be included, and what they would need to do to be included. They were also excluded from the government-Reserve Bank arrangements enabling banks to offer mortgage repayment deferrals but offered them anyway.

Although they are small within the overall financial system, the likes of the Nelson Building Society and Wairarapa Building Society, plus the two biggest credit unions Credit Union Baywide and First Credit Union, are significant players in provincial parts of NZ.

On top of this the Reserve Bank twice delayed the starting date for the phasing in of new bank regulatory capital requirements to the frustration of NZ owned banks. In November 2020 TSB CEO Donna Cooper told interest.co.nz the delay meant NZ owned banks would remain disadvantaged against the Australian-owned ANZ, ASB, BNZ and Westpac from a capital perspective for even longer than expected.

"In residential [housing] lending, we’re required to hold on average 45% more capital than Australian-owned banks, for the same risk," Cooper noted.

Opportunity to tackle credit cards missed

Within the banking sector an obvious area the Government could've taken action on years ago is credit cards. In 2015 when Australian authorities, led by the Reserve Bank of Australia, were moving against high credit card interest rates, interest.co.nz sought to engage NZ authorities on the issue given credit card interest rates were at similar levels to Australia, even topping 20% in some cases.

At that time the Commerce Commission told us it could only act on credit cards if evidence emerged of collusion between banks to set rates at a certain level. The Reserve Bank told us its mandate was to regulate at a systemic level, to make sure the financial system remains sound, not from an individual customer protection perspective. And the then-National Commerce and Consumer Affairs Minister Paul Goldsmith told us it was for the banks themselves to explain the interest rates they charge.

In 2018 we even had then-Co-operative Bank CEO David Cunningham, a former Westpac executive, tell interest.co.nz credit cards were "a real area of customer harm," and ripe for a Commerce Commission market study. The deafening silence from NZ authorities continued.

The dominance of the oligopoly

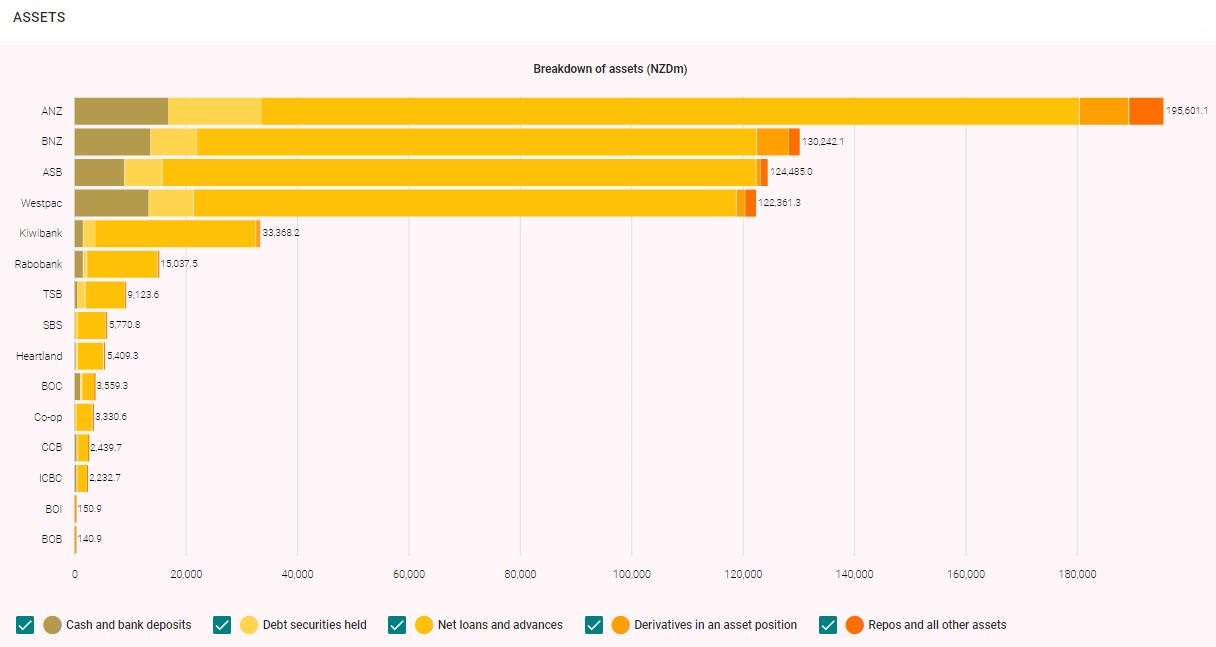

We've known for years that NZ's major banks are right up there among the most profitable in the developed world across a range of measures. The oligopoly dominance of the big four, demonstrated in the Reserve Bank chart below, is a key factor in this.

The most recent Reserve Bank quarterly figures, from the December 2022 quarter, show the big four made combined net profit after tax of $1.646 billion. That's up $145 million, or 10%, year-on-year against the backdrop of a forecast recession. Meanwhile, the average net interest margin across the four rose to 2.4% in the December 2022 quarter from 2.025% in the December 2021 quarter, the average cost to income ratio fell to 35.7% from 37.6%, and the average return on equity was up 10 basis points to 14.1%.

NZ bank assets as of December 31, 2022

Winston's hot air

At times our politicians have failed to back up their rhetoric with action. Notably, going into the 2017 election NZ First's Winston Peters was pledging to "conduct a review of the foreign-owned banks focusing on competition." Peters told interest.co.nz a "bunch of subservient puppetized [NZ] politicians" weren't acting in the national interests of business and private citizens. However NZ First's coalition agreement with Labour didn't include any requirement for a banking inquiry.

Meanwhile, the Reserve Bank hasn't been keen on offering restricted banking registration to new entry digital, challenger banks, which has happened in the UK and Australia. Here the Reserve Bank instead points to the non-bank deposit taker option.

An idea I've floated before, that might help existing smaller banks and non-bank financial institutions better compete with the big banks, is sharing back office functions - potentially including a joint core banking system - as a way to reduce costs. Some discussions did take place on this between some NZ owned banks a few years ago. When I raised the issue with the Reserve Bank at the time I was told the regulator had heard nothing and thus wouldn't comment.

Threats to banks, real or imagined?

Speaking in an episode of interest.co.nz's Of Interest podcast, Reserve Bank Director of Money and Cash Ian Woolford suggested a central bank digital currency (CBDC) could boost competition and innovation in NZ's financial system by enabling more competition in transactions and payments offerings. The Reserve Bank is considering introducing a CBDC.

Th development of CBDCs has even led to questions about whether we still need banks. Credit rating agency Fitch is among those to have warned about the potential of disintermediation, or loss of business and relevance, for banks from the introduction of CBDCs.

"We believe the introduction of CBDCs will inevitably involve households and businesses converting some of their commercial bank deposits into CBDCs. All other things being equal, this would require banks to shrink their balance sheets - a process known as disintermediation," Fitch says.

A CBDC is the digital form of a country’s fiat currency, thus the NZ dollar in NZ's case. Woolford acknowledged technically members of the public could have an account directly with the central bank, thus disintermediating banks. However, this isn't on the Reserve Bank's agenda.

"I find it hard to see a world, and certainly the Reserve Bank would not want to have a world, where there were no financial institutions anymore and everything was run through the central bank. That is not what we are aiming to do," said Woolford.

Instead the Reserve Bank sees a CBDC more as a defensive move, to shore up the status quo and protect it and NZ's monetary sovereignty. Banks are front and centre of this status quo.

Big banks are also adept at delaying, embracing and partnering with emerging threats to their business. And they benefit from baked-in thinking in NZ that market solutions will always be the best ones. Hence the glacial moves towards open banking, merchant service fee regulation and failure to even contemplate that anything at all could or should be done about extortionate credit card interest rates.

If the Government does give the Commerce Commission the greenlight to undertake a market study into banking, probing the factors affecting competition, finding out how well competition is working and whether it could be improved, I'll keep a close eye on it. But I'll be surprised if it leads to any dramatic change.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

45 Comments

If she had a formal qualification or work experience in finance/economics, she would understand a short inquiry in the complex world of banking wouldn't surmount to anything.

A bachelor's in English lit, masters in journalism and a career in lobbying wouldn't get you a job as a grad analyst in back-office treasury operations of a bank these days. However, business champ Luxon thinks she's qualified to run the fiscal portfolio of a $375b national economy. Did he even consider Andrew Bayly for this job?

Your mistake is to assume that they intend to achieve anything other than political posturing. Name one inquiry that Labour instigated that resulted in a beneficial outcome for Kiwi's? The petrol one? The supermarket one? The electricity one? The building products one? At least Willis is being honest and effectively saying let's not waste a lot of time and money on this when we know nothing much will result from it. Hopefully a National led inquiry would at least result in consumers not being harmed, unlike the Labour Govt one that decided that 60% of Kiwi's should lose their cheap electricity plan.

So why do they need an inquiry to Tell them what is patently obvious. What we need are meaningful actions.

The commerce commission is a complete waste of tax payers money. Little more than a mechanism to rubber stamp our multitude of monopolies.

We would be better off disbanding them and contracting the Australian Commerce Commission to do the job. They at least seem to know what they are there for.

The mistake that Labour made was trusting the ComCom who are either a bunch of complete morons or are corrupt.

Isn't it completely obvious that the only way to end the supermarket duopoly in any kind of reasonable timeframe is to break the chains up? Instead they are merely allowing more competition in (maybe they should have done that 20 years ago when they allowed the duopoly to form). But it will take decades for enough competition to give the big 2 any kind of scare.

And, Advisor, your friends in Labour lite have done what reviews ( into banking)?...

Still waiting for...

Poverty

Crime

Housing

Health

Education

Roading

Slash

Fuel

Gib board

Dot dot dot....

.. Reviews to be done by Arderns/ Hipkins lot.

Oh, how's the "road to zero" going for you....

And. ...Let's not mention zero suicides from the original health minister the " left dishonourable Clark"

Nor, cheap EVs, better roads, reducing homeless...

I could go on All Day about the KEY UNDELIVERABLES OF THIS BUNCH OF ASSES!

THIER BIGGEST ACHIEVEMENTS TO DATE...

1. MORE HOMELESS

2. MORE DEBT.

3.MORE INFLATION

4. MORE BENEFICIARY'S

5. MORE WAITING LISTS

6. MORE SLASH

7. MORE TAXES.

8. MORE MURDERS

9. NoreCRIME.

10 MORE ROAD DEATHS.

11. More spending in minorities and Maoris

12. Huge RACIAL AND CLASS DIVISION!

Its a "MORE SPENDING FOR WORSE OUTCOMES" junket!...

AND 40% OF DUMB KIWIS ARE STILL SUPPORTING BEING TURKEYS @ THANKS LABOURS GIVING

One point: More people out of work given the increased rates of disablement by disease and recession should not be a surprise given the global pandemic that crashed world finances. Just saying that is one thing that you can claim they did not affect directly.

However more people disabled by disease given we know 10% infected would have severe long term effects in countries with better medical support and less comorbidity than NZ, much of those 10% infected leading to disablement, should also not be a surprise. The government could have reduced the number disabled or dead with a better targeted vaccination campaigns and medical education for the populace but hey we still have people in this country who believe raw water is a cure and that 5G spreads viruses. Perhaps without sufficient adult education support Labour truly could do nothing to prevent increased spread of the virus. Besides we already know we have a lack of support for retraining & employment support leading to more long term unemployment and less health staff.

Did John Key approve this request of National for a sharp inquiry ?

Another political posture during the election year. Sensational, no doubt. I don't see Bank Bosses shaking in their trousers/skirts about this.

If they want competition, then National should support massively capitalising KiwiBank which is now state owned and opening of branches in all those places where the 4 Majors closed them in the last 10 years.

Game, National ?

"Members of the public could have an account directly with the central bank, thus disintermediating banks. However, this isn't on the Reserve Bank's agenda." It should be.

Commercial Banks don't have to get disintermediated. All the RBNZ has to do is offer a Call Account facility to anyone with an IRD number. Nothing more, nothing less.

Leave the commercial stuff, mortgages, credit cards, term deposits etc to the registered banks. But allowing us all the option of moving to the RBNZ, CBDC or not, would be the best first step we could take and instil that sense of competition for retail deposits that's missing today. 9/10 of us might open an account and have minimal balance in it to keep it active. But just the knowledge by the commercial banks that there is an alternative will be enough.

Said it before but ComCom gave the majors permission to buy Postbank, TrustBank and National Bank/Countrywide in the 1990's/early 2000's. They were real competitors for retail and some in business/agri and institutional. The competitors these days are niche or just too small.

And sadly, apathy is probably also barrier to effective competition.

ComCom also greenlit Z's acquisition of Caltex in 2016, which saw Z Energy take control of roughly 49% of NZ's fuel retail market. Less than 3 years later, ComCom kicked off a detailed study to address its concerns over competition within NZ's fuel sector.

Perhaps we should start with a study into NZ's dysfunctional market regulatory agency.

Another problem with getting the small banks/credit society's competitive is their inability to attract depositors. The shadow of Sth Canterbury Finance and the BNZ hangs long over New Zealanders' collective memory. With no Govt deposit guarantee in NZ, people have to ask themselves "is my money safe in this bank?" And the answer is invariably, "it is safest in the big 4 so that's where I will put my money".

The lack of a mortgage securitisation industry here is also an issue, which if one existed, would allow smaller banks to recycle funds and grow, in the way Macquarie Bank has in Australia.

As for record profits, the banks are not all that profitable when compared to other companies on other industries, their return on capital (14%) is half that of Woolworths (29%).

Yes which is why an NZ version of Fannie and Freddy would help consumers plan long term and help smaller banks fund....

The MBS could be sold to NZ Kiwisaver funds (and internationally) which would also help these funds deliver better returns to NZers...

Let me see, who would loose from this.... wait a minute....

ITS A NO BRAINER

There is a deposit guarantee coming - https://www.interest.co.nz/personal-finance/117092/what-nzs-deposit-insurance-regime-will-look-and-what-itll-mean-depositors

"people whose deposits are with higher-risk institutions such as finance companies will pay more for their guarantees."

Yeah, that's really going to encourage competition! Now people will just stick with the Big 4 because it will be cheaper and they lose less of their own money paying for other banks bad lending decisions.

The big 4 banks are very profitable. Therefore they pay a lot of tax. Governments like tax.

Interchangeable for super markets, fuel retailers, gentailers, building product suppliers.

Its like the Mob. As long as you a kicking up a slice to the big guy. No one cares about the people who get screwed over by the corruption.

Lol - if you earn a lot as a result of government assitance to limit competition and offer poor regulation etc it seems fair you would pay a LOT more tax.

Sounds like ' hey banks just help yourselves to massive amounts of our citizens money ($2k per year per person/household) and be sure to make sure you reduce your costs and customer service and improve profits. Dont worry about helping our peasants save more via term d rates and so on either... you need it more than they! If you dont mind to drop a few dollars back in the tax pot before you take the rest overseas it would be really nice.. we are getting a bit behind on our health, infrastracture and so on.

PS - definitely appreciate if you could to sponsor the pmarties and offer some lucrative jobs to our leaders too!

PPS - we cant believe the peasants dont revolt over all this stuff ither.. too busy on facebook lol.

The big banks send a lot of money overseas as non taxable fees to their parent companies. Then they send more profit overseas than they pay in wages. When I shut my BNZ accounts to consolidate at NZ owned banks the staff member from BNZ organizing it said, "I don't know why anyone banks with us!" So why do people still do so? Is it the same people who buy off foreign owned grocery firms, grocery deliverers, takeaway firms, taxi firms, hardware firms, cheap junk shops, when they could get the same service off a Kiwi firm? These people deserve all the bad things that happen to them for their stupidity. Maybe a commenter who does buy off the above can enlighten me.

I thought you raised a good question & as no one else responded I'll share my experience - cant speak for everyone.

I've been with BNZ a long time (~20+years), also HSBC until a few years ago because of their excellent global multicurrency banking setup & Fx rates for Premium customers. Am a BNZ Visa Platinum card holder all that time which used to be much more worthwhile than currently.

Have had a handful of issues with BNZ over the years however always easily & quickly addressed - even used to have a private banker early on which was much better personal service but apparently stopped qualifying when we moved half our money to HSBC - & likely they've since raised the bar.

I joined Kiwibank when they started because "NZ" however gave them away after a few years because their transaction, TD & Fx systems were hopelessly inefficient & communication was poor, contact people seemed untrained.

Wife also had Westpac accounts in Oz & NZ untilabout 5 years ago, TDs were a hopeless paper based phone call nightmare.

Bottom line is that I need my banking to be seamless, easy online/app & hassle free with competitive interest & transaction rates. I'd also like to be considered a valuable customer not a problem.

Yeah. We banked with Kiwibank from near on it's start. Had issues with most of the other banks - not the bank's fault [ahem, greed] - but if you're employer doesn't pay you when they were meant to, paying BNZ $175 for the privilege of having my APs that night fail .. hurt.

But Kiwibank were fairly rubbish - they were mostly post staff with some additional training, and getting anything done was a pain. Plus they doubled their fees one year for the sole reason that their fees were lower than other banks, so they should charge higher to be more profitable. That didn't last long, but we'd already switched to Co-operative by the time they fixed that little snafu.

Had a few years with Co-op, pretty much had their tech support on speed dial because we ran our business with them too - which apparently was fairly uncommon - and we'd often find bugs in their business banking system that needed fairly urgent fixing. Their annual payout was a pittance, however - I suspect they spent more advertising that they made it than they actually paid out. When we closed the business during Covid, we reverted back to Kiwibank, where we now run dozens of 'Free Up' accounts, and it just works. Though, we don't run any credit facilities or a mortgage, so our needs are fairly light. Just waiting to see where TD rates head...

The banks make most of their profits from mortgage interest don't they? Why not tackle that area first because it is by far the easiest. If the banks weren't allowed to bundle mortgages with general banking then it would be a lot easier to shift your mortgage and keep all your accounts, payments, credit cards, etc as they are. Probably doesn't even need regulation, just the threat of regulation should be enough for the banks to comply.

You are just showing your lack of understanding of NZ Bank funding. NZ Banks keep mortgages on balance sheet rather then package and sell MBS. They do a bit of MBS for repo security but dont sell them, and as you say, why sell such a cash cow.

Smaller banks can't fund as cheap... enter NZ fannie or freedy who could fund lower then the big four could...........

Aussie has the four pillars, the social license seems to be on a choke collar or shorter leash over there.

NZ is like diary farming for the big four, say Mooooooo NZ mortgage holders.

Well at least you could move your mortgage between the big 5 (incl Kiwibank) easily enough, that would provide a lot more competition between them.

I haven't changed bank in 20 years as it would be too much hassle. Every time I refixed over the years I could have get a better rate or cash back at another bank, so it has probably cost me 20k or more in total.

But if you had a 15/20/25 fixed rate mortgage you would not care about moving, refinacing to a lower rate yes......

Easy to see how it could become subprime central though if a majority gummint decided everybody deserved to be able to buy a house, looking at you Bill Clinton / Nanaia Mahuta. Would need collusion from rating agencies, nah it could never happen....

Man I can so see this happening in NZ at the bottom of the market as who ever is in power needs an asset bubble to blow back up.

In the US world at any time if your 25 year loan could be refinanced at a lower rate you can take out a new loan at the lower rate and retire the old one... not sure what the refinance cost is, let me check that out.....

Refinancing your mortgage (freddiemac.com)

so you effectively take out a completely new laon with associated costs , but possibly way way less interest for the rest of the period.

I guess you’d also have to ask what capital is required to be held against assets of $571bn. Then what is the acceptable return on that. Is RoE of ~12% excessive?

Also you’d need to understand how the regulatory burden placed on banks today acts as a barrier to entry and a moat for scale players. BS11, CCCFA, FSLAA, DTA, Cofi, etc all have to complied with. How does that impact the current competitive context?

Not to mention the raft of treasury compliance in international markets, All of which would be removed in many ways if we had a Fanny Freddy system.... just saying.

If you want competition in Mortgage writing you need to level the playing field re funding.

Fannie Mae and Freddie Mac: Overview

In 1938, the government created Fannie Mae, or the Federal National Mortgage Association, amid the struggles of the Great Depression. The goal of Fannie Mae was to create a more reliable source of funding for homebuyers, opening doors for more Americans, figuratively and literally.

Freddie Mac, short for the Federal Home Loan Mortgage Corporation, came on the scene through an act of Congress in 1970, with a similar purpose. Both Fannie Mae and Freddie Mac now operate under the conservatorship of the Federal Housing Finance Agency (FHFA).

Fannie Mae and Freddie Mac help facilitate access to long-term, fixed-rate mortgages with installment payments. They do this by buying mortgages from banks and other lenders, giving the lenders more capital to continue creating loans for more borrowers. Fannie Mae and Freddie Mac typically package the loans they buy into mortgage-backed securities in the secondary mortgage market.

Both GSEs played a role in the Great Recession. In the years leading up to the housing market collapse, they backed or owned numerous subprime mortgages. When the housing bubble burst, economic pressures and large losses led to the need for the government to step in with bail-out funding. As a result, Fannie Mae and Freddie Mac were able to help usher the housing market toward recovery.

Fast-forward to the COVID-19 pandemic, and Fannie Mae and Freddie Mac have helped offer mortgage relief and protections to homeowners, including forbearance and loan modification programs.

Differences between Fannie Mae and Freddie Mac

Beyond the age difference, what sets Fannie Mae and Freddie Mac apart? Although both buy mortgages, they purchase the loans from different sources. In general, Fannie Mae tends to buy loans from larger commercial banks and lenders, whereas Freddie Mac often buys loans from smaller banks.

In addition, Fannie Mae and Freddie Mac have slightly different requirements of the mortgages they purchase. The mortgage has to be a conforming loan, or adhere to these standards, for it to be eligible for purchase. The requirements cover the amount of the loan, the borrower’s credit score and debt-to-income (DTI) ratio, loan-to-value (LTV) ratio and other factors.

Fannie Mae and Freddie Mac mortgages

Neither Fannie Mae nor Freddie Mac directly provide mortgages to homebuyers. Instead, you’ll get your loan from a mortgage lender, such as a bank, credit union or online lender, which can then choose to sell the loan to one of these GSEs, assuming the loan’s eligible. As of 2020, Fannie Mae and Freddie Mac owned 62 percent of conforming loans.

Successive governments have been gutless.

They are not for the people by the people.

1) Legislate to make ComCom take competition fully into account as a key objective and that it’s recommendations must address the objective. Especially the HHI index.

2) Direct ComCom to investigate all market areas where there is less than perfect competition (6 or 7 market players with equal market share) in priority order (market size and degree of lack of competition)

3) Let ComCom go and do its work.

if these rules had been in place ANZ would never have bought The National Bank and we wouldn’t have supermarket duopoly along with many others.

We welcome your comments below. If you are not already registered, please register to comment.

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.