BNZ's interim profit rose 14% to $805 million as net interest income, the difference between the revenue generated from a bank's interest-bearing assets such as loans and the expenses associated with paying its interest-bearing liabilities such as deposits, rose 26%.

BNZ says net profit after tax for the six months to March rose $96 million to $805 million from $709 million in the six months to March 2022.

Net interest income increased $300 million to $1.464 billion, with total operating income up $277 million, or 19%, to $1.775 billion. BNZ says its net interest margin jumped 41 basis points to 2.45%.

Meanwhile, operating expenses rose $88 million, or 18%, to $577 million. And BNZ's credit impairment charge swelled to $79 million from $21 million. The bank reported a 14 basis points drop in its cost-to-income ratio to 32.5%.

BNZ says total loans rose $3.2 billion, or 3%, to $101 billion, as deposits increased $1 billion to $75 billion.

CEO Dan Huggins says BNZ is well positioned to support customers finding it tough in the current economic climate.

"We know our customers well and understand that many New Zealand households are feeling the pressure of cost of living increases, particularly those with home loans. While we're confident that our home loan customers are able to manage the current higher interest rate environment, for some, it will be challenging," Huggins says.

"As always, our message to customers is get in touch - we're here to help."

In its bi-annual Financial Stability Report on Wednesday, the Reserve Bank said for households that borrowed during the period of very low interest rates between late 2020 and late 2021, current interest rates exceed some of the test rates used by banks during this period.

"Therefore, some of these borrowers and other borrowers with high debt-to-income levels may begin to struggle to meet their repayment obligations as they reprice onto the higher rates. Around 25% of the current stock of mortgage lending was originated during 2021, with about a fifth of this being to first home buyers," the Reserve Bank said.

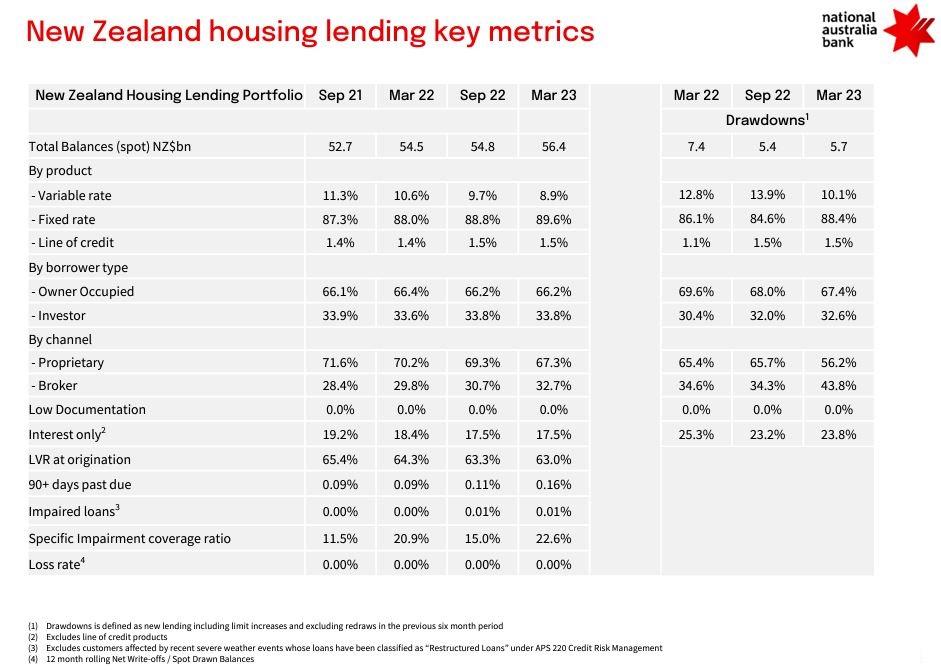

Parent National Australia Bank's investor presentation is here.

31 Comments

Lol - they are there to make as much money as possible for themselves and their shareholders. To be fair they never really admit other wise.

So as long as people can make payments all is good. if not give them a call so they can help by telling you whether they will give you two months or three .. before they sell your place from under you and bankrupt you or whatever.

These outsized margins will be being generated by depositors, not mortgage holders - mortgage rates relative to swap are like the lowest they've ever been. Because most commentary about margins make people think about mortgage rates, all the depo customers miss out.

That isn't what Dan Huggins said. He essentially "blamed" the increase in margins on the RBNZ raising OCR rates so quickly, such that the difference in the interest rate charged on the mortgage compared to the cost of that money to the bank had increased.

As I've said before, banks will increase mortgage rates quickly but deposit rates slowly when the OCR is rising, and the reverse when it is falling. No-one can look at a bank and say that their main goal is not to profit.

Considering banks just borrow from other banks, including the central bank, and loan that out at higher rates, I've always wondered why we can't borrow from those source banks directly, at the lower rates, instead of paying a middleman a significant margin to connect Lender A with Borrower B.

No doubt there are regulatory requirements in there some where, but if the central bank thinks it's riskier to lend to the consumer than a commercial bank, they didn't learn much from the GFC or the more recent SVB failure. Surely it's better to have a few smaller debts default than one massive one?

Crony capitalism - central and retail banks working together to maximise profits and providing bailouts when they take on too much risk (socialising losses)

The only social license in this industry is the one where the taxpayer bailouts the bank! And the bankers are abusing that side of the social contract.

No doubt a nice kicker there courtesy of the Funding for Lending program. The BNZ have taken advantage of rising rates by increasing mortgage rates much faster than deposits.

They have lost their social license in my estimation. There is no alpha in these numbers, they take no risk what so ever. They simply leach their customers. To paraphrase Matt Taibi, the BNZ are a vampire squid jamming their blood funnel into our society and sucking the soul out of the nation.

Yup, sound about right... it is THEIR profit.

Then when people start defaulting on their mortgages and the banks need a bailout suddenly it's OUR problem and the tax payer must front the bailout.

There should be a rule that some of these record profits are allocated to a "when s#%t goes bad" fund.

haha.... no chance ever. if there was such a fund - it would be funded from increased fees to us, not from their bonuses and profits.

No - the world is now set up of bankers/elite and everyone else. They always win and we always use. If you have kids.. a degree in economics or finance is the way for them to go. If banking wasnt such a dull, entitled and arrogant career... i would have done it..

If you're lucky - you'll get a repayment holiday or interest only period for 3 to 6 months and you'll probably pay a fee for this 'service' ... But only if they judge there is light at the end of the tunnel. Of course, that 'holiday' gets capitalised and you're in even more debt.

If you've gone for a shorter term mortgage, 20 or 25 years, they may let you re-finance for 30 years to lower the weekly/monthly repayments and you'll probably pay a fee for this 'service'. ... But only if they judge there is light at the end of the tunnel. Of course, the longer the term the more interest they can collect from you.

Anyone else get's their 'help' in a mortgagee sale with any shortfall being turned into a loan they'll graciously provide for you and and you'll probably pay a fee for this 'service'.

Never, ever, for a single moment, think the bank is doing you a favour. They're not. And as soon as you can - change banks - it costs them heaps to get new customers.

A far better bet is to visit a budget advisory service and explore all the options with them before relying on a 'bank' to come to your rescue. If they can't outright fix the problem they can get you into a much better position for when you do need to go cap in hand to the bank. (Case in point - they suggested selling a share of a friend's home to a relative. This worked out extremely well for my friend and the relative.)

We welcome your comments below. If you are not already registered, please register to comment.

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.