Hopeful first home buyers had little to cheer about in December's home loan affordability figures.

According to interest.co.nz's Home Loan Affordability Report, the REINZ's national lower quartile selling price declined by almost $11,000 at the end of last year, dropping from $670,000 in November to $659,000 in December.

However that brought almost no relief to prospective first home buyers because the benefit of slightly lower prices at the bottom of the market was almost entirely eaten up by higher mortgage interest rates.

The average of the two year fixed rates offered by the major banks increased from 4.08% in November to 4.21% in December, marking the seventh successive month of mortgage rate increases since they bottomed out at 2.52% in May last year.

If that pattern persists there may be little relief in sight for first home buyers struggling to afford a home of their own, because although housing prices are expected to soften over the next year or so, mortgage rates are expected to keep rising, which means any benefit of lower prices may be eaten up by rising mortgage interest rates and higher mortgage payments.

Essentially, house prices would have to start falling at a much greater rate than interest rates are rising for first home buyers to receive any substantial benefit.

The situation for first home buyers at the end of last year was compounded by the fact that although the national lower quartile price declined in December compared November, it actually increased in eight of the 12 REINZ sales regions, setting record highs in seven regions (Northland, Waikato, Bay of Plenty, Wellington, Canterbury, Otago and Southland), while the lower quartile price in Auckland was unchanged from November's record high.

Only three regions recorded declines in their lower quartile price in December - Hawke's Bay, Taranaki and Nelson/Marlborough.

The situation of first home buyers was starting to look quite grim for first home buyers on average incomes in most parts of the country at the end of last year, as the unaffordability issues that have plagued Auckland for many years spread to many other parts of the country.

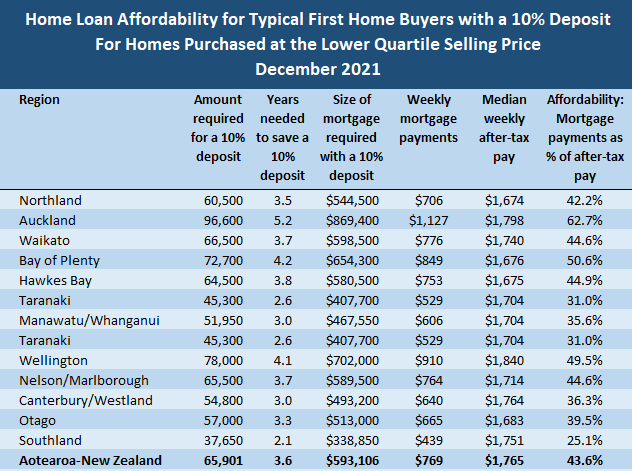

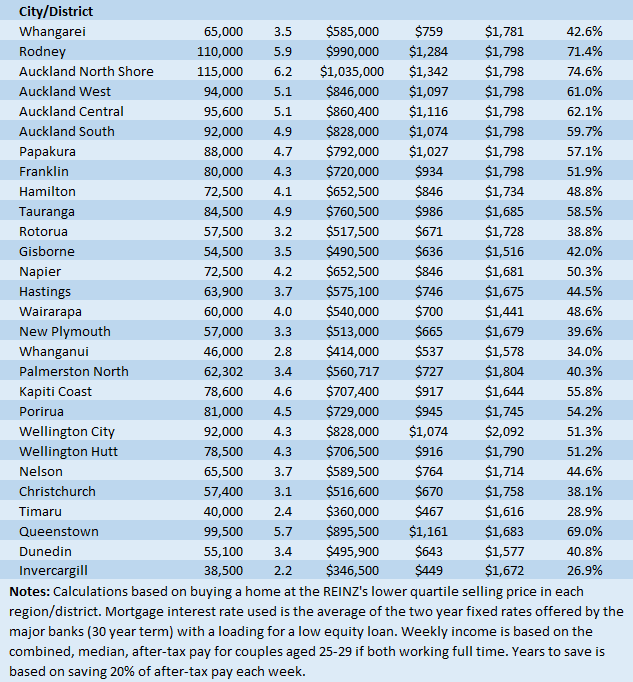

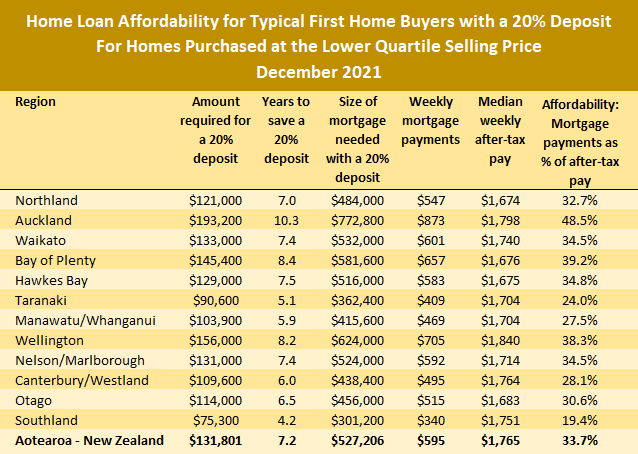

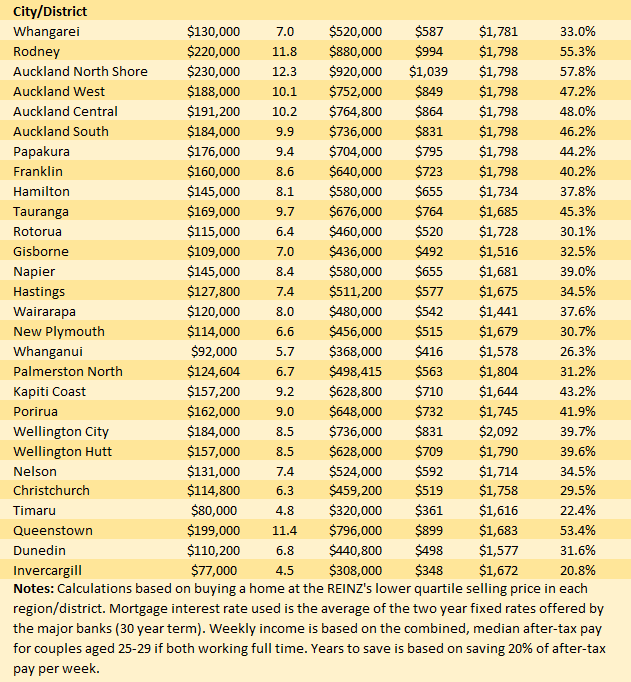

Interest.co.nz's Home Loan Affordability Report calculates how much money would be needed for a 10% or 20% deposit on a home purchased at the lower quartile selling price in all of Aotearoa's main urban areas, and then calculates the amount of the resulting mortgage payments.

That is then compared with the median after-tax pay for couples aged 25-29 in each region, assuming both work full time.

Housing is considered unaffordable when the mortgage payments eat up more than 40% of take home pay (the tables below show the results of those calculations based on 10% and 20% deposits).

This shows that the mortgage payments on lower quartile-priced homes would now be considered unaffordable in the majority of regions around the country for young couples on average rates of pay if they only had a 10% deposit.

The only regions where mortgage payments would considered affordable for couples on average wages with a 10% deposit are Manawatu/Whanganui, Taranaki, Canterbury, Otago and Southland.

All other parts of the country are considered unaffordable for people on average wages.

However, if first home buyers can scrape together a 20% deposit, that reduces the mortgage payments as a percentage of after-tax pay sufficiently for all regions except Auckland to be considered affordable.

But getting together a 20% deposit wouldn't be easy either.

The amount need for a 20% deposit on a lower quartile-priced home would range from $75,300 in Southland to $193,200 in Auckland.

That all but rules out home ownership for young people on average wages in Auckland and it wouldn't be easy in the rest of the country either, with Southland and Taranaki being the only regions where the amount needed for a 20% deposit on a lower-quartile-priced home is less than $100,000 (refer to the tables below for the full regional figures).

Unfortunately home ownership is increasingly becoming the preserve of the highly paid or those who have access to capital from other sources such as obliging parents or winning Lotto.

But for most young people on average wages, saving for a home of their own is increasingly looking like the impossible dream.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

142 Comments

It's impossible!

First-home buyers can't win.

TTP

They can win. It is just the system is designed in a way so they don't win.

Yeah I agree, it's the system. The system doesn't want FHB to get into market easily. Before the system is deflecting housing crisis issues from low interest rate, foreign buyers, lacking of property tax to housing shortage. Now when the regulations finally got loosed a bit for building more houses, now the system starts to complain about allowing too many houses will destroy their beautiful backyard and New Zealand's beautiful environment. Yeah Nah, FHB can not win, if they win, how can ponzi schemes be sustainable? There must be less supply, low interest rate, no tax towards housing Market.

Yes and more stories of FHBs getting shafted by developers and sunset clauses.

The developers need to be very careful though, I suspect many of them don't understand the brave new world. Or maybe they do and they think it's less risk to try and sell again at a much higher price than meeting existing buyers halfway?

We have definitely entered the early stages of a building bust.

Can't be too long before the developers and investor lobby groups push the young generations too far and anger boils over, surely.

They will quietly leave the country, then we'll have labour shortages, then we bring in more immigrants with lower expectations to pay the rents, then repeat.

Ahem. There is already a massive Labour shortage. Everywhere. When the GFC hit the Govt at the time should have undertaken a state house building program, or made property debt tax rinsing subject to only new housing. On the back of that building activity many a young tradesman would have had work and stayed in NZ. Now that generation of apprentices is all in Australia. Well done National...

More houses for you TTP aka "Taking The Proverbial" and your ilk.....I just can not believe how weak kiwis are with this property market ! .....I mean its all geared up for the banks, investors with equity and their immediate hangers on ..... what a ridiculous situation for a so called economically "first world" country, shutting working people out of a home of their own .....surprised there hasn't been protests in the streets !!

The time when it makes the most sense for a FHB to buy is when the news is dire, finance is hard and "they" say you'd be mad to buy a property ever again. So people stay away from the market in droves and later comment rationalize their decision making.

Exactly like now. I go to tons open homes and put offers in. There's no buyers around.

Now is the time for punters to buy houses.

Vested interests scream that govt shd not interfere in mortgage lending.

See the almost daily bashing of CCCFA in MSM. A well-oiled campaign ,obviously funded by parties with deep pockets for selfish motives.

Under the guise of charity towards welfare of FHB's they push for lending to be treated as Borrower's problem. Really?

Tell it to those who parked $$$ in the finance companies which keeled over. Geneva, Hanover, Capital & Merchant etc. Whose hard-earned monies went up in flames????

A collapse largely triggered by imprudent ( & sometimes dodgy) lending.

Poor Mom & Pop depositors saw their nest eggs evaporate. Many had to emerge from retirement & re-join the work force to survive.

What's the source of $1.6 billion to bail out South Canterbury Finance??? Taxpayers' money, not from Borrowers.

The then -Govt quietly removed the Deposit Guarantee for banks.

Reckless lending has potential for OBR. History can repeat itself , for banks this time. Just Borrower's problem?????

Bizarre, the ranting against the CCCFA.

All it asks is whether the banks' leadership mortgage brokers are prepared to put their money where their mouth is regarding the appropriateness and the riskiness of their lending. Yet suddenly, when asked to do so they pull back on lending amounts?

Were they not being honest and robust in their lending practices prior to this? Why is the addition of some personal responsibility affecting them so? And all this time folk have insisted personal responsibility is important...

The open letter they wrote, their only practical complaint was that they now had to verify a borrowers expenses, and couldn’t just take the borrowers word for what their expenses are.

amazing

@Miguel, that's not quite right. The CCCFA Regulations now require that banks take into account discretionary expenses - all regular or frequently recurring outgoings (for example, savings, investments YES THAT IS NOT A TYPO- SAVINGS + INVESTMENTS MUST BE TAKEN INTO ACCOUNT AS AN EXPENSE, gym memberships etc) that are material and the borrower is not willing to change. Taking discretionary expenses into account can have a huge effect on the required affordability calculation that the lenders are now required to carry out. The government, and Select Committee (which David Seymour himself sat on!) were warned multiple times of the implications the new laws would have but they chose to ignore and go ahead with the changes anyway.

So...lenders must factor in their regular outgoings the borrower is not willing to change, and what income they have. And then stand behind the robustness and riskiness of their lending with a bit of personal responsibility.

Sounds reasonable.

Should have always been this way. I wonder if the same level of scrutiny applies to property investors?

Surely a broker would advise a borrower that affordability was tight and tell them they would have to cut discretionary savings and investment to get a mortgage. I would assume 99% of people would then do that.

The broker complaints just scream out of self-interest and that they all just got caught out by applications that in the past would have got through and now aren't. Particularly for legitimate reasons like the above where they have discretionary expenses they aren't willing to give up on.

It may be hard now but when house prices come back 60% the loan will be smaller, mortgage repayments will be smaller and the deposit will be smaller.

>when house prices come back 60%

Lol, $400k houses in Auckland? There a line from that movie "The Castle" that is appropriate here.

Yes very very unlikely. A 25- 30% drop is quite possible though.

And will only bring us back to beginning of 2021 prices.

If prices drop by 60% it's almost game over NZ.

You're right, a 25-30% drop is quite possible, its just not probable.

I agree. But I would rate it at least a 20- 25% possibility.

I still think a 5-10% drop is most likely.

Gen-X, just wait till the prices come back 100%, you won't need any loan at all !

Why stop there... Why not wait till they pay you to take a house off them?

So... like Auckland CBD apartments?

Only the two L's of Doom, Leakers and Leasehold, they arent giving you a property, they are giving you their liability.

Would certainly be a change from only current owners being the welfare beneficiaries.

You finally understand, horray! We should be celebrating house prices and the cost of living going down, not up.

2022 has started th a Warning.

Many who made heaps in stock market in 2020 and saw profit dipping in 2021 are now in deep red just 22 days in 2022.. If lucky portfolio will be down by 20% to 30% and for many is much much more. If the current stock market bloodbath continues, investors will lose millions and many who have never witnessed a crash will be in a shock as many entered in last two years and was a game for them.

Now on top of that if ever growing housing price stop growing, many will be caught in passing the parcel and whoever ends up last with the parcel is out and IF Housing market falls ( for many it is a one way street cannot go wrong, so over streched) even by 10% it will blood on the streets.

Hopefully the mess created by reserve banks is sorted out soon or their generous help in last two years will turn fatal.

I was imploring my 81 year old father to sell his stocks mid-late last year. He didn't listen to me. That's his prerogative I guess.

Your Dad still has his stocks. He possibly didn't get where he is by selling much. Diamond hands. Don't discount a lifetime of experience!

Nah he's a novice, he bought 3 years ago and has done reasonably well. I think he should get out now while he's still ahead. His gain over the past 3 years could start disappearing quite quickly. Last year wasn't great.

Anyway it's his moolah and he's got his wits about him so fair game.

many kiwisaver balances will be taking a big hit

Take a moment and look at your portfolio guaranteed the “blood in the streets” has its stain on you!

Just hope that housing market does not take the same route.

In any pyramid ponzi, bubble should keep moving up, Up and UP, the moment it stops it ........as their is no room for plateauing.

This week's auction result should give an indication, where we are heading into 2022. Auction result has been more than 60% to 75% since last two years and will be interesting to see how it pansout in coming weeks. Even if success rate is 50% plus, will be positive.

In difficult times stock market is still more liquid than housing market.

a little?

And what happened last couple of times when stocks tanked? Investors took their money out of stocks and poured it into housing, will be interesting to see this time around

Probably. I'm paranoid so moved to Conservative fund a few years ago. So I've missed out on money pumping, govt/RBNZ sponsored windfall gains, but at least I'm not wondering what to do if the share market slide continues.

If interest rates are so high that they couldn't afford such large mortgage to get into the market, then maybe they shouldn't get into the market now? It doesn't mean they won't in future. Maybe our loving and caring government and RBNZ can help / support them to save up a good deposit while they are waiting like by reducing the tax towards a saving account and curbing the inflation?

Best time to buy a house is yesterday.

Second best time is today.

Disregard today’s conditions - interest rates, prices, finance regulations, etc.

This time 35 years ago we were paying 21% mortgage interest. Was 100% of my salary!

Yes but in time you were saved by both rising house prices and dropping interest rates.

These days it's the opposite, with rising interest rates and falling prices coming up.

Or should we disregard today's conditions and just trust you?

Today? You gotta be joking.

Did you live in shoe box in middle of the road and work 24 hours a day.

Yes and no the house was around about a 10th or less of if current price. Its all relative.

At the end of this debt super cycle where interest rates really need to end up a bit higher than inflation now is the time to wait especially if your stretching yourself to the moon. Likely hood is banks wont fund the money anyway. Some people wont be able to wait and will have to pull the trigger. Just make sure your income is solid and you plan to be there for some time so any declines will inflate away in the future.

Main issue is the industry around selling houses will have way less turnover than the speculative nature of the last ten years. Just like the GFC it will need to adjust and cut costs.

Buy today? At your own risk! That's all I can say.

Had to take out a mortgage at 21% because you couldn't save 40% of your pay for 5 years and buy the house outright? Remember, term deposit rates were double digit too.

These days first home buyers must save for 5 - 10 years just for a deposit, with TD rates at 2%.

100k for a new build. Wages 25-28k.

Repayments were most of one wage.

No promise of falling interest rates and prices were flat for years.

Yes - There was a Muldoon Home ownership account scheme with tax refunds, but saving 20k was still a challenge.

Ok, but if you look at the graph above, that is still a much better deal than what people are getting now. You would need to save significantly more than one year's wages for one person to have even a 10% deposit, and then repayments will be most of one wage.

A new build at 4 x wages. Not a bad deal at all, imagine if you just saved up for an entry level home instead.

That was entry level. With only gib & bare floors etc ie a shell. That era allowed you to build with no minimum covenants on many sections, and people could move into kit set shells without onerous council inspections.

I dont buy that. In the early 90s I paid 123k for a 3 beddy in Onehunga. No kids, 60k a year coming into the household, mid 20s. By the time I was 29, kids and making it work on 1 wage, we werent on the bones of our collective arse even at that level. That is absolutely impossible now in ak.

That same house is now valued at over 1.5m, roughly 10x what comes into my house hold now. Young people today have absolutely no chance.

According to this, the median NZ house price 35 years ago was 83,337. So it's hard to believe that 'entry level' prices anywhere were 100k, especially if you are talking about kit set shells.

I have mentioned this before, but new builds were always more expensive (I trained as a QS way back when), the belief these days that an old crappy bungalow has the same value as a new house is all about spruiker folklore, like the millions coming home, best place to live in the WORLD etc etc etc... dont let the truth get in the way of a good sales pitch.

This is actually good news for landlords.

For many aspiring FHBs, this may be the last chance in life to own their own homes.

For those who are holding on to their expiring pre-approvals, thinking alone won't change your lives for the better; it's the action you choose (and for many, time isn't a luxury).

Choose the path of least regrets.

Act soon.

Professional house scalper getting desperate to offload.

Time isn't a luxury in his quest to be the richest slumlord in the cemetary.

Nobody is ever going to be able afford a house ever again... apparently.

Nobody is ever going to be able afford a house ever again... apparently.

The story is that these houses with king's ransom price tags will be passed to the kids of the boomers who will live happily ever after.

Spoken like a true property spruiker CWBW .....bet your waiting in the wings with "dry powder" when these prices drop ...not all of us were born yesterday.

Over 10 years to save for 20% deposit in Auckland . Then 48.5% of wages just to pay mortgage how can anyone say this living.this is with two people what happens if one get ill or has a baby. In 10 years time if you have managed to save deposit which i seriously doubt unless you are not paying rent and living with mum and dad, in that 10 years the price of deposit needed would double at start again. The only way to stop this sole destroying process is if house price to fall to a place where average wage earners can afford to purchase a home and still live.I think this is about to happen over next year or so with interest rate raising and inflation up it will need to drop around 50% I know this would cause huge problems to people and investors who have purchase in last three years but it’s the only way to get back a balanced society.

Would love to see the numbers you have used here.

Look at top of article in chart. This is also for starter house in Auckland at 772 k not much around for that price let alone in 10 years time when you have saved money for deposit.

A few glaring assumptions made.

That is assuming no Kiwisaver and that the money saved is put under the mattress.

It is also assuming that the couple buys a "lower quartile home" for $966,000 which is mad.

But if we don't do this we can't enrich older asset owners. Prices are not allowed to fall. We are pulling forward consumption from the future.

A lot of ifs there and dangerous risks which ever way you go. The only safe sure thing to do is leave NZ for an higher paying country with affordable houses. Either that or Invercargill or similar.

The big hurdle for me has been saving for a deposit. Now that the ever constant house price rises have stopped, I now have a clear goal towards reaching 20%, especially if prices drop to meet my deposit.

And if lucky, maybe your 20% deposit will become 30% or 40% or you may reach your goal of 20% much faster than expected, IF the ponzi falls apart.

Good luck Solid Granite, be persistent, you'll get there!

Good luck, fingers crossed for you. It is about time there was a correction in this market.

The new CCCFA rules are having an even worse effect on FHB's being able to get a loan, extremely difficult for a couple on average income to get finance to buy a house with these new strict rules.

remember 2007 when the rules weren't quite so strict?

Maybe sellers might have to meet the market? Or is you theory fhb’s are gone for ever?

You don't understand rastus, the CCCFA pretty much ends the FHB's dream of borrowing money, so it doesn't matter about vendors.

Surely if they can't buy then the market will correct until they can?

Or do you expect investors to step in and fill the void? If that happens, I'd expect Labour will find another way to turn the screws on investors.

Or what?

Yvil - can you explain why CCCFA would end a FHBs dream of borrowing money? Another statement that makes no sense...

There seem to be a lot rules that are very simple to understand which don't make sense to you. I can't be bothered explaining what the CCCFA is to you Nifty, google it and you will (hopefully) understand why it makes borrowing more difficult

You seem to make statements which are inaccurate/misleading quite frequently... I'm across CCCFA - I don't see how it stops a FHB's dream of borrowing? Have you got a real life scenario of this? Has someone you know gone from being able to borrow to not being able to borrow at all because of CCCFA...?

Nifty, there are plenty of brokers who cannot get finance for their customers which qualified before CCCFA, this is very well documented. Please read some articles before making ignorant comments

It's not well documented at all. The majority of articles coming out have little to no detail and are skewed to paint CCCFA in a bad light. Of course brokers aren't happy, it's making their job harder, they can't simply ignore what they did before in an application (expenses/outgoings/liabilities). It's slowing down business for them & as a result less commission. If someone can't borrow at all now due to CCCFA there's likely something seriously wrong with the way they're operating their finances, and most likely good reason to decline. Please get some real world feedback and don't focus on what you see in NZ Herald/Oneroof that is real estate bias.

Yes it is very well documented, get your head out of the sand: here is T Alexanders survey of many, many mortgage brokers:

The monthly survey of mortgage advisers which I run with mortgages.co.nz shows that the CCCFA-induced credit crunch continues to depress mortgage activity and therefore the property purchase aspirations of first home buyers as well as investors and owner-occupiers more generally. The results and comments from advisors illustrating the extreme difficulties loan applicants now face can be accessed here.

Tony Alexander, yeah he's an unbiased commentator... seen all the sponsors he's got over his newsletters, he works for One Roof too right LOL.

The quote you attached states all home buyers & investors are affected. As explained in my comment, brokers aren't happy as a result.

I haven't seen anything about FHBs dreams of borrowing gone? Where's a real world case?

If anything, borrowers in general may not be able to borrow as much given their evidenced expenditure & outgoings... it doesn't mean they can no longer borrow.

You get your data from friends, Facebook, your local butcher and maybe some guys at the pub, I'll get mine form professionals involved in the field at hand.

Maybe re-read the comments from Nifty1 again and take another try, maybe also take a look at the thumbs up they have got vs your zero for all your comments - probably tells you something. You are just spouting back brokers biased views on the impact of CCCFA no real world examples. In fact most of the articles i've seen with the examples brokers are providing it seems completely reasonable that banks have declined the applications.

Thumbs up are indeed a good indicator of the pack upvoting each other, for the majority are ignorant, poor and unsuccessful.

Of course it's reasonable that banks decline applications, which was an admission by you that they do indeed decline more applications, which is exactly my point, since the CCCFA it's getting harder to get finance.

Wow, it's incredible you know the majority of the commenters well enough to make a statement like that.

I wonder what meets your definition of not ignorant, not poor, and not unsuccessful.

Either way I suspect you're wrong.

@ Solve_it ....regarding that comment of our learned commentator Yvil, that "most of the upticks on this site are from ignorant, poor and unsuccessful people", Yvil has shown his "true colours" here, as I have always thought and said - I can tolerate ignorant people, as maybe they just don't genuinely know, while I don't take much notice of arrogant people - probably picked it up from their parents.

As far as "poor & unsuccessful" how would Yvil know ?.... is he hacking our PC's ? .....and that is where one of the most dangerous character flaws makes its play - to be ignorant and arrogant AT THE SAME TIME

These people will not listen or reason ....while if you have any point of view that does not align with theirs, you are "as above".....just be glad we don't have to go through life with such biases.

All it asks is whether the banks' leadership mortgage brokers are prepared to put their money where their mouth is regarding the appropriateness and the riskiness of their lending. Yet suddenly, when asked to do so they pull back on lending amounts?

Were they not being honest and robust in their lending practices prior to this? Why is the addition of some personal responsibility affecting them so?

It may be just, unjust, right or wrong but there is no denying the CCCFA has made it much harder for many, especially FHB's, to be able to get a loan.

Isn’t it the ridiculous prices that have made it hard for people to get a loan? The CCCFA could be the best thing that’s ever happened to the NZ property market. Time will tell, but servicing a million+ dollar mortgage on a median salary in Auckland doesn’t seem like much fun anyway

It's not stopping them from getting a loan in most instances, it's only stopping them from getting loans matching current asking prices. The question should be whether we should always be looking first to how we can enable young people to pay more for houses, or how we can make house prices lower.

We should probably stop milking the younger generations for our own benefit.

"should" "should" "should".

If you don't like the rules and want to change them, get into politics. Whinging on this forum will not change anything

Shouldn't you be running for public office rather than criticising the CCCFA, then?

Actually, criticising policy and swaying public opinion on forums and social media has proven to be incredibly effective in recent years.

I got my free money from Reserve Bank and govt welfare for property over the last years just as you have, but there's no reason not to push for a better deal for NZ's younger generations. Better that than merely staying silent and enriching ourselves.

It's useful for people to realise that affordable house prices are entirely achievable by policy and that's been done in NZ before, and that policy in recent years has been directly responsible for transferring billions in wealth from wages and savings into property and other assets. I'm happy to stop criticising intergenerational wealth theft when we stop perpetuating it.

Not sure why you'd object to folk voicing support for younger non-asset-owners in a comments forum. It's a comments forum.

@RickStrauss Why is the addition of some personal responsibility affecting them so?

Because the new CCCFA requirements prescribe in detail the types of expenses that must be taken into account, which wasn't the case before. This includes discretionary expenses (which may include payments made towards savings and investments!) which are now required to be analysed and included in the affordability calculation. If you had the choice, would you be prepared to put yourself personally at risk by choosing not to follow the new requirements prescribed by the Labour government?

If I were asked to personally vouch for the robustness of my borrower's income vs. the expenses they incur each month, I'm sure I'd lend more carefully than if I could merely bank on outsourcing all risk in a tits-up scenario to the taxpayer, indeed.

It'd be concerning if my lending levels were significantly lower than before because people might be led to wonder if I'd been completely realistic in previous lending.

@RickStrauss - You seem to be missing the point that the new CCCFA requirements are preventing people from getting credit that they otherwise could have got. Its not that the banks are no longer willing to lend - they are not allowed to lend to the level that they would be happy to do so anymore given the new prescribed requirements. So, I agree that it is concerning that lending levels are significantly lower than before, but not for the reason that you imply, being that the banks have not been realistic with previous lending. Rather, it is concerning because the CCCFA has gone too far and has limited lenders (not just banks) by imposing requirements that are too prescriptive.

Your previous posts seem to suggest that lending must now factor in discretionary expenses that the buyer is not willing to stop spending, though. Which seems to suggest lenders are accurately factoring in actual regular and likely ongoing spend with actual income, and coming to lending levels they deem reasonable and are happy to put their personal vouchsafe behind.

Not factoring in regular ongoing expenses seems unreasonably risky.

We should be looking at how to bring house prices lower, not how to constantly extract more money out of younger generations.

Would you be happy with a compromise - allow banks to not factor in discretionary expenses but retain personal responsibility in bank's leadership? That seems fair and in line with our ideals of personal responsibility, yes?

I recently applied for a mortgage approval and was still offered the same absurd amounts of credit.

The CCCFA is restricting sub-prime lending and that's a good thing.

DTI ratios are going to come in and restrict things even more.

The extreme house prices are caused by extremely loose credit.

Gee, you can complain all you want if the CCCFA is a good thing or not use all the "shoulds" in the world", my original statement that it makes borrowing more difficult still stands true. (even if Nifty didn't understand it)

Why complain about it here then object to others commenting on it?

Making borrowing more difficult is a good thing, especially if people are borrowing 7 times income. Houses and borrowing need to fall in line with incomes. Doesn't sound like rocket science. Can you afford, yes, you can borrow, Can you afford, no, you can't borrow.

I agree, but I would say it was extremely difficult even without CCCFA.

You heard it here first

I'm taking you back to the late 1950s and 1960s when I was a teenager and my father decided to try and drag us out of poverty as a school-teacher by becoming a real estate agent. He became quite successful.

Some major practices in those times were as follows:

Nearly every house sale to a FHB entailed the necessity of acquiring a smaller second mortgage left in by the vendor, another family member (e.g. parents), or some other provider. This second mortgage was for a period of usually 3 or 5 years, was interest only, and carried a slightly higher interest rate than the first mortgage supplied by the bank. The FHBs first priority was to pay off the principal of the second mortgage while keeping up the payments on the first mortgage. Once they had paid off the second mortgage life became a lot easier and only then, in most cases, did they consider having a family and the mother was able to stop work.

Investors usually used their solicitors' trust fund to supply just the one mortgage (a first mortgage) to finance a purchase. This persisted until solicitors' stealing from their trust funds became endemic and their clients realized that there were so many cases of solicitors caught with their fingers in the till that the trust fund eventually couldn't cover all the theft and the honest solicitors baulked at paying higher trust fund levies and so their clients started losing money that the trust fund couldn't cover. This method of finance then became dead in the water.

How does this information apply today:

Well, if a buyer can't get finance from the bank then a vendor could always supply a second mortgage, interest only, or he could supply the whole (first) mortgage, interest only, and avoid banks altogether at least for 5 or so years. The interest rate would be slightly lower than the banks' but still give the vendor a return higher than he could obtain from a bank deposit. He could also obtain a higher price for his property.

This would only work if the vendor didn't need all the sale price to fund another property purchase ( eg an investor getting out of the market), or a down-sizing vendor.

The bank that is 1st mortgagee needs to approve the second mortgage, and they usually won't do that.

The market is made up of people taking on stupidly large amounts of debt to buy what are likely for them to be financial liabilities.

All that is needed is for either:

• first home buyers to en masse adopt some financial sense and refuse to pay

• someone to force them to adopt financial sense.

We tried the first and it didn’t work, now we are trying the later.

The answer to high house prices can’t be to continue to bury young couples in increasingly large piles of debt.

I'm just trying to imagine the scenario where a family can afford for the mother to stop work to look after any kids while there is still a mortgage. Nope too far gone for anyone under the age of 45.

So the medium, after tax pay is based on couples working full time. That in itself raises questions. Plus the fact that over half of marriges end in divorce, and women generally want babies before 30, and 5 years from now, interest rates could well be over 5%.. Hoo-hum

However..

https://markets.businessinsider.com/news/stocks/stock-market-outlook-je…

Auckland property has been overvalued for a long time. Can it correct more than 20%? Yes. Will it correct more than 20%? No.

If that happens, the banks will be in serious trouble, possibly needing a tax payer funded bail out. The govt simply can't afford for that to happen.

Its going to get messy that is for sure, but the government (which ever one is power when it hits the fan) will do what it can to save the banks, not the people.

Auckland's value proposition is fading fast. Bloated and indebted council, sky high property, social problems, traffic nightmare etc etc. I'll be leaving as soon as my kids finish college.

The only certainty is, council will keep bleeding us dry. Voting with feet is the only solution.

It's like there's Dark Matter in the system : nothing adds up but yet it still holds together ...well until now

What a great way of putting it.

Thanks for clarifying those %. I wasn’t sure myself, nice of you to bring some certainty to the table.

Why would banks lose if prices go down over 20% most places have gone up around 40% in last year and buyers would have put down 20% deposit so a 50% drop would not trouble the banks. Would cause huge problem for investors but they take this chance and have been on winning side for years.

Banks should be fine - the RBNZ stress tests them based on a 39% fall in house prices accompanied by 11.8% unemployment rates, an OCR of -0.5% and a prolonged North Island drought.

"The scenario is assessed as a one-in-50 to one-in-75 year event"

Expect to see something like that at least once in your life time.

https://www.rbnz.govt.nz/-/media/ReserveBank/Files/Publications/Bulleti…

Yeah but do they stress test them with an ocr of 7.5% due to imported inflation.?

this testing looks hopelessly inadequate but hey they ran a few scenarios....good luck with that I say

Stocks market crash is expected to be worse than 2008.

Can housing sector be immune !

Investor behaviour is completely different but time will tell

Bitcoin and Ponzi used in the same sentence, who would have guessed ?

You cut down interest rates, people complain FHB's are losing. You add interest rates, people complain FHB's are losing. So what now? People will never stop complaining.

It almost seems like if you want "true parity", then maybe we should adopt ideology like China's, and push something similar like their "common prosperity" agenda. That sound good for you NZ? You want to follow the same ideology?

How about we just simply strip away everyone's ability to buy more than 1 house. That should solve the supply problem and the pricing problem. 1 house per citizen of New Zealand. Anything after that, it's illegal and you can be jailed for life. Is this what everyone wants to push for affordable housing?

Sounds good to me

It's mostly crocodile tears for FHB. If folk were truly concerned for FHB there'd be more discussion of the need to make housing affordable, not the need to extract more debt out of FHB.

This is right. When special interests (landlords, banks, mortgage brokers, etc) find a policy that hurts them they immediately reach for a first home buyer sob story for the media. The only way housing gets more affordable for FHBs is for prices to come down.

One thing I’ve learned in my old age - the importance of cashflow. You know what capital gains doesn’t deliver? Cashflow. Your house can go up 50%, you still owe the same amount of money, have to make the same payments. You can’t sell and realise the gain because it’s your home and you can’t climb the ‘ladder’ because the house you want has gone up 50% (and in absolute terms that 50% is greater).

No need for anything so dramatic - just impose a tax based on a 5% deemed return on all homes other than the primary residence. Similar to treatment of foreign shareholdings. On higher tax bands this means an annual tax of 1.65-1.95% of the rated value of any investment properties, second homes etc.

Same thing was imposed on foreign shares a couple of decades ago to try to encourage local investment, I think the argument to discourage investment in housing is far stronger.

Would be very easy to do. Have each and every dwelling tied to an IRD number.

If the IRD number has personal income tax lodged against it each year (wages, salary, benefits/superannuation etc) then exempt the property from the tax.

Would work a treat for a 76-unit tower block with a body Corp.....oh, wait.....

I love it. The sooner we realise the holy trinity of 'the home, the batch (on air BNB) and the IP' is a tax lurk first and foremost, the better.

If anyone expected a 1% reduction in prices to make it affordable would have a screw loose... I guess some boomers would be thinking this way.

The idea that a 30-50% decline in house prices would destroy our financial system, is a myth designed to perpetuate the housing ponzi.

There would be some disruption but society would cope.

Society would, in fact, thrive.

I haven't seen a society that's has a dramatic fall in house prices that's ended up being a good, thriving place to live.

Care to share some examples? Detroit? Rural Italy? Beirut?

Closest I can think of is Japan, and their post bubble experience is at best super mediocre.

Ireland prices went down about 50% quite recently.

https://tradingeconomics.com/ireland/housing-index

The UK has had a couple of big busts, ~35% and 25%, in the last few decades.

https://www.allagents.co.uk/house-prices-adjusted/

These things are actually quite common, despite what New Zealanders think.

Prices can and do go down, I'm just not aware that's happened only to be followed by a situation that somehow benefits society more. They usually either eventually return to where they were, flatline, or turn to shit.

Ireland has become a tax haven for large multinationals to avoid billions in taxes elsewhere, maybe that's where we should be going.

This housing market is out of control and only reason it is so high is because of emergency interest rates now rates are going up people who have jumped in are going to get burnt if you don’t understand this Pa1nter think about it we have high inflation interest rate raising NZD tanking a couple on average wages not able to by the cheapest house in Auckland of course society is going to be better once bubble bursts houses are for living in not for speculators and investors to make money.

There are elements of truism in much of what you say, but I would also be super amazed if a 40% drop didn't accompany more hurt on average for non-asset owners, from the commensurate economic turmoil.

The interest rates no doubt are fuel, but there's also various other demand and supply side factors related to the pandemic. Until that situation reaches a better level of equilibrium (probably still another 12-24 months), you are going to see fairly unorthodox pricing going on - assuming there's no massive economic unravelling beforehand.

If I'm not mistaken, Detroit's issues were not caused by a housing market crash. They had issues with deindustrialization and population declines.

And decades of dopey Democrat government ....

Spain, Ireland, USA, UK for starters...

Property bubbles burst. The world doesn't end...

The world doesn't end but it causes a massive amount of hurt to everyone. House prices dropping by 50% means that FHB's will have enough for a deposit but that isn't the only impact. Massive job losses mean that they can buy a house and then have no income to repay the mortgage.

Lets take Spain as an example.

House prices drop from 150,000 to 100,000 between 2008 and 2013.

Unemployment rises from 11% to 26%

Did house prices drop due to unemployment rises, or did unemployment rise due to house price drops?

30% - 50% in NZ, I doubt but 10% - 20% very much on the card.

yep and 20% of the average house price is still over $200k!! that's a whole lot of smashed avocado!

People who are over leveraged would be in trouble and a lot of investors would probably go under this is the gamble they take and investors have made a killing for years. With house price this high it is beyond average wage earners to own a house in Auckland and I think the party was over November December 2021, this year the everything bubble has burst housing will take a little longer than financial markets and crypto but down it will fall time frame just depends on interest rates and inflation our sad government will not be able to stop it.In the end NZ society will better.

Auckland stopped being affordable for average income earners more than a decade ago.

We welcome your comments below. If you are not already registered, please register to comment.

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.