The strong profits of New Zealand's banks puts them in a good position to earn their social licence by supporting customers through taking a long-term perspective in times of stress in their lending books, the Reserve Bank (RBNZ) says.

In the RBNZ’s May Financial Stability report, Governor Adrian Orr said the financial system was well placed to handle higher interest rates and global economic disruption.

The banking system’s capital and liquidity positions were strong, with profitability and asset quality remaining high. This will allow financial institutions to take a long-term perspective and support customers through economic challenges, Orr said.

The RBNZ said the benefits of profitable banks were apparent in the current environment, where banks will be able to manage increased stress on their loans as economic conditions deteriorate.

The central bank signaled that retail banks should use their profitability to support customers through the difficult times, as high interest rates start to result in mortgage defaults.

“Therefore, profitability puts banks in a position to earn their social licence by contributing to a sound, efficient, inclusive, and dynamic financial system”.

A social licence to operate refers to the ongoing acceptance of a company or industry's standard business practices and operating procedures.

Strong profitability questioned

Bank profits in the pandemic-era have been controversial. The National Party and the Green Party have both called for a select committee inquiry, while the RBNZ’s chief economist has said a Commerce Commission market study might be appropriate.

The financial stability report, however, said bank profitability was only high in nominal terms, and was about average once adjusted for inflation and economic growth.

Nominal profits grew in 2021 and 2022 as the economy boomed, it said, this was aided by few loan defaults and higher net interest margins.

During the pandemic years, large monetary and fiscal stimulus allowed New Zealanders to park large sums of money in bank deposits which offered very low interest rates.

Deposits are a high quality source of funding for banks and having high levels of cash allowed them to fund lending without relying on more expensive wholesale funding.

Rates on short-duration deposits, such as transaction and on-call savings accounts, have not increased as quickly as the Official Cash Rate and the interest income banks earn on their assets.

“Consequently, these deposits have become increasingly profitable sources of funding relative to term deposits or issuing debt in wholesale markets,” the central bank said.

Customers have been slowly transitioning back into term deposits as interest rates have risen, but competition for deposits has been mild as banks already have lots of cash and demand for loans has softened.

Really profitable

However, measuring profitability in nominal terms hides the impact of inflation and the growing size of a business. Return on assets and return on equity are more useful measures, the Reserve Bank says.

Bank balance sheets have grown since 2020 due to economic growth and lower dividend payouts to shareholders.

“As a result, the return on assets and return on equity are at similar levels to those in the decade prior to the pandemic,” the RBNZ said.

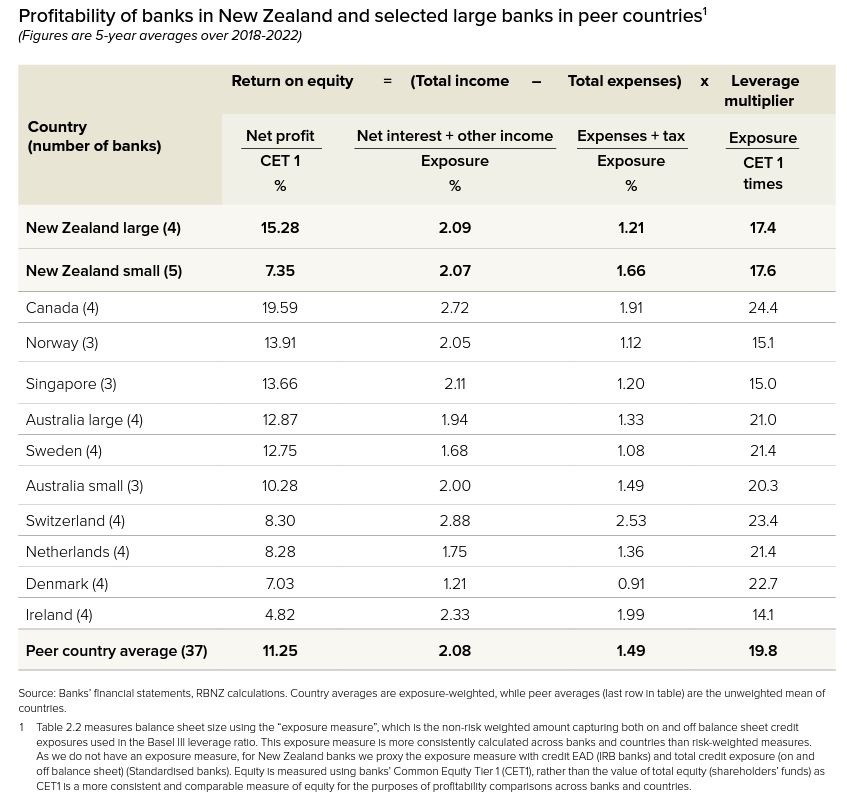

While large NZ banks are not “materially more profitable in 2023” than in the past 30 years, they have long been more profitable than most in comparable economies.

The RBNZ outlined a number of possible reasons for the higher profitability of NZ banks including: higher levels of risk, a lack of competition, economies of scale, and Australian shareholders requiring higher returns to cover tax costs.

Whatever the reason, large New Zealand banks earn a 15.3% return on equity, compared with an 11.3% average in peer countries. Australia’s average was 12.9%, Canada was 19.6%, and Ireland was 4.8%.

48 Comments

"Therefore, profitability puts banks in a position to earn their social licence by contributing to a sound, efficient, inclusive, and dynamic financial system”

If the RBNZ had restrained from directing banks to "lend courageously to begin with and banks collectively had a "social conscience" we would not be in this mess. Now, the RBNZ in an effort to avert a financial instability issue, is now implying - you ain't seen nothing yet. If we were, interest rates would be coming down already. It looks like its all on a collision course, until one day - thud.

"It's important to point out that our banking system in Ireland is very well capitalised [...] It's coming off a very strong performance over the last 11, 12 years, very strong profits [...] Our governor of our Central Bank in a report this week has confirmed the healthy nature of our banking system, as I say, well capitalised [...] We don't have the exposure, any significant exposure in the sub-prime US sector, which has caused a lot of the problems originally and I think it's important to point that out."

- Ireland's Minister for Finance, Brian Cowen - 2008

History is littered with examples like this. The fact is that even if they are completely up the creek they still have to say things like this, because the second they call it as it is the panic sets in and then they lose their ability to influence anything.

I wonder what shareholders will think of 'carrying' bad debt and losing profitability - just to be seen as being 'nice'.

It wouldn't surprise me if banks get very ruthless at reducing risk if it means their own survival is on the line and shareholders are demanding action.

Or perhaps the RBNZ will just bail them out if it all gets tough enough - see the USA....

Another round of privatising profits and socialising the loses.

Banks dont have social licenses. They are there to generate profit for shareholders. The board wont care what profit they made in the boom - thats yesterday, Their best bankers want their bonuses (or will leave) and their shareholders want their dividends and ever increasing share prices rises (or will fire the board). So all they gonna do is that -> sell stuff and cut losses.

if you default on the mortgage for long - good luck. Orr is dreaming (as usual) with all this... 'be kind' and whatever he is waffling about social licences (sounds rather socialist to me). Really scary that he would think anyone is listening to that tbh.

In a world where all banks can create their product out of thin air and are implicitly guaranteed from failure, it should be expected that banks are profitable and "safe."

But for those who are able to think independently and can see the logical inconsistences in the above, this is also why the banks and their respective economies are not anti-fragile.

On the whole, the sheeple don't really understand the fragility. They don't understand the tradeoffs from the constant manipulation of the money supply (value of labor and savings in currency are destroyed). All they have is people like Orr telling them how wonderful, benevolent, and 'risk free' the framework is. If it weren't so comical, it would be tragic.

Yes modern western society have become debt slaves under this crony form of capitalism - with central banks in bed with/and or bailing out retail banks who privatise their profits and socialise their loses.

And at the same time we like to look down at other nations and systems as being inferior/corrupt - which I always find odd given how far from good the system we live within and accept, really is.

Unless there is legislation driving this "social license" this is meaningless. They are "Banks" after all.

Yes. First of all, there needs to be a definition of this 'social license.' Adrian Orr cannot even do that.

For example, if I want to run a dairy, my social license is that I can make as much profit as I like as long as I don't sell ciggies to kids.

Social license as it applies to banks is ephemeral. What does it actually mean? You can make as much money as you like as long as you don't blow big asset bubbles? Bit too late for that I reckon. So it seems to me that the social license is now if you have to give up a little profit to keep the dream alive for individuals, then you're doing what Orr expects. But what if the banks are just applying death by a thousand cuts? Is that social license?

Social license is just puffery, woke spoke. There is no social license. We need banks for the economy to function ... whether we like it or not. Orr is just an apologist for the banks, presumably because he wants to chair one of them when his tenure as governor comes to an end.

Social license is just puffery, woke spoke.

I stopped referring to Orr as 'Kaumatua' because I thought it was somewhat disrespectful to Maoridom. Nevertheless, it concerns that you don't hear a squeak from Maori leadership or the woke warriors about the cultural appropriation by the RBNZ, let alone the wanton destruction they wreak on the socio-economic fabric of Aotearoa NZ. Anyone with any semblance of understanding should understand that the RBNZ undermines Maori economic sovereignty.

"The Reserve Bank (RBNZ) says the country’s houses are still “somewhat overvalued” and prices risk falling “significantly” below a level it deems sustainable"

https://www.nzherald.co.nz/business/reserve-bank-house-prices-remain-ov…

Distressed sales are next...

Yes. And look. His foot soldiers have been stealing my ideas and adapting them for his media releases. I know these RBNZ comments are added as a 'Get Out of Jail' card.

“However, there remains the risk of house prices declining significantly below our assessment of their sustainable level, particularly if the number of distressed sales picks up, generating self-reinforcing negative feedback effects.”

The strong profits of New Zealand's banks puts them in a good position to earn their social licence by supporting customers

What absolute balderdash, is ORR actually a resident of this planet.?

Whatever profits the banks take are immediately distributed to their shareholders and never to be seen again.

It is ORR that gives them the license to take those funds and disappear. And it is ORR that has maximised that position for them.

This is funny.... basically admittance we havent seen nothing yet. lol.

“Current prices are within the range of fundamental values suggested by some of the metrics we monitor, but the overall balance across indicators suggests prices remain somewhat overvalued,” the RBNZ said.

“In the near term prices may continue to soften, given the level of interest rates, the ongoing completion of houses currently under construction, and weak market activity and sentiment.

“However, there remains the risk of house prices declining significantly below our assessment of their sustainable level, particularly if the number of distressed sales picks up, generating self-reinforcing negative feedback effects.”

They are nuts - they are saying they want to increase unemployment. Do they think its not thus a 100% probability that distressed sales will pick up? And thus house prices WILL fall below their whatever price guess.

Honestly - who hired these people

Translating RBNZ speak into real implications:

"You are well positioned to support customers in tougher times" = "If you don't support customers in these tough times there is going to be a compounding run on mortgagee sales, further crashing the housing market big time, and the banks, and RBNZ will be in the pooh even bigger time."

He's telling banks they will need to come to the party when things start to come unstuck in next 6 - 18 months. If the public perceives that the banks are acting unfairly (maybe foreclosing, maybe increasing net interest margins while people are suffering, whatever the case may be), he is telling the banks that government and the RBNZ wield a stick and public opinion may force them to use it.

huttman

Re: "I wonder what RBNZ wanting big banks to do? "

It will depend on the individual bank and customer's circumstances (equity etc) and is likely to include a couple of obvious ones:

- Changing the loan temporarily from P&I to interest only

- Increasing the term of the mortgage

- Providing a mortgage holiday or partial-holiday as during the COVID pandemic, and

- With falling house prices, looking past any possible loss of borrower's equity if the borrower is most likely meet repayments in the longer term . . . . .

I doubt that the normal practice of banks is to offer a discounted interest rate. Whatever the action, it is likely to be some sort of deferment or restructuring arrangement where the customer eventually pays with the banks not be foregoing anything.

Just a note on mortgage holiday: This lets you temporarily stop making repayments on your mortgage if you’re under financial pressure. However, there is no holiday from interest charges. Your debt continues to accrue interest - and possibly interest on interest - during a mortgage holiday. The “holiday” only lets you defer repayments – and it means that it will eventually cost more to repay one's mortgage and most likely take longer.

"Reserve Bank says the high level of NZ bank profitability means they're well positioned to support customers in tougher times"

Let me fix the title:

Reserve Bank says the high level of Australian bank profitability means they're well positioned to support customers in tougher times

Mr Orr you are right the banks need to give something back in the hard times!

The reality is that's just you dreaming .. They will be ruthless unless legislated, after all they are loyal to shareholders not the RBNZ!

After all your team gave them these huge profits by providing lending facilities for up the 3 years at OCR rates and below.

At the same time you depressed deposit rates for investors and continued to provide super cheep money after the crisis was well over ..Shame on the RBNZ for providing these facilities for so long.

This transferred wealth from the public sector and investors to the banks as they gorged on cheep debt and raised their margins.

So front up and say the RBNZ had some responsibility for allowing this to occur and admit you were responsible for it due to letting the cheep funding go on for a year longer than it should have.

We welcome your comments below. If you are not already registered, please register to comment.

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.