Well, everybody else appears to have run off and hidden. But not those doughty first home buyers (FHBs).

They are still out in force, borrowing money to buy houses. But as for everybody else, not so much.

The Reserve Bank's April figures for new mortgages make pretty dire reading and represent a continuation of what's been an incredibly slow start to the year in the mortgage market.

The RBNZ's now been compiling the mortgage lending by borrower type for approaching 10 years and the April figures, with just $4.33 billion advanced, are among the worst recorded.

As far as the month of April goes, the only worse month was the lockdown month in 2020 when just $2.749 billion was advanced, but the April of 2017 runs close with just $4.558 billion advanced then.

More recent comparisons are really not flattering though, as in April 2022 there was $5.664 billion advanced, while in April 2021 - during the heady days of the last housing sugar-rush - there was $8.486 billion advanced.

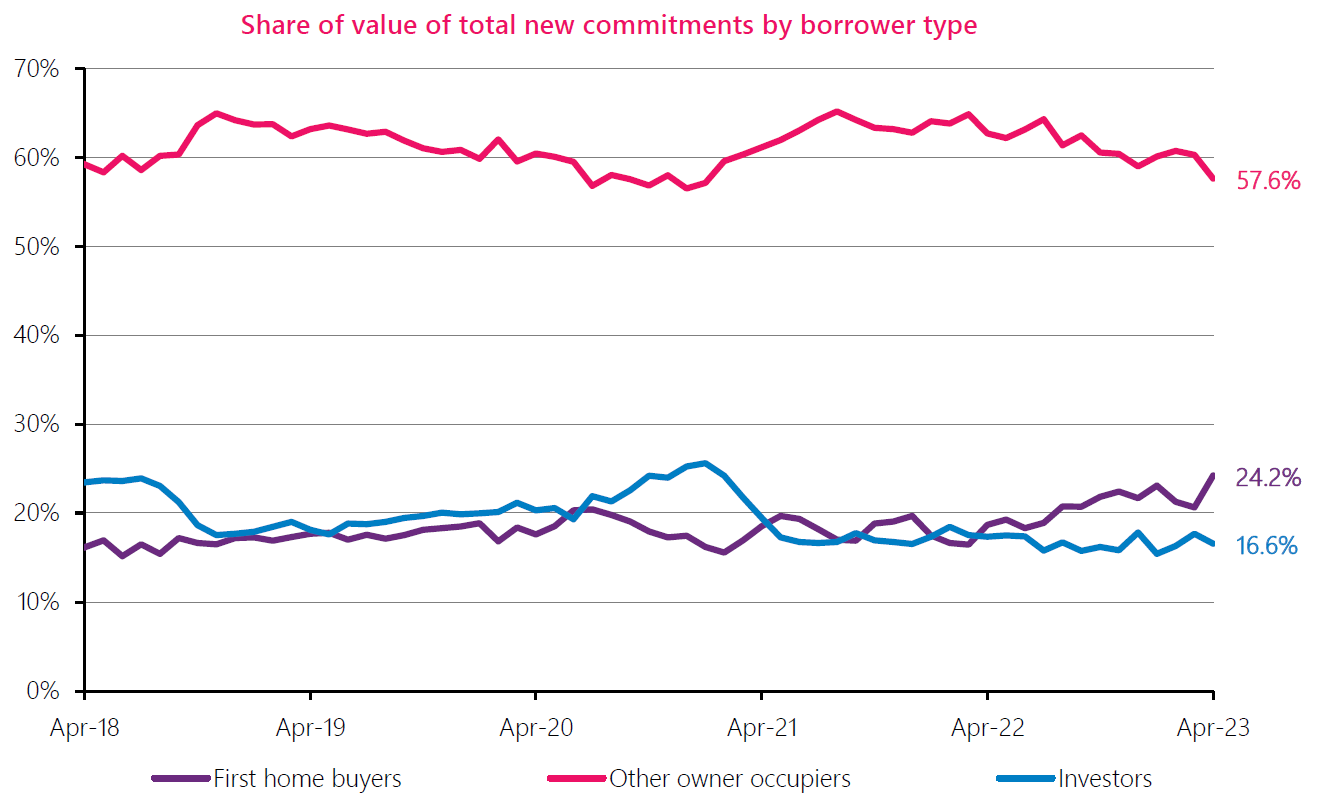

Back, however, to those FHBs. In April 2023 they borrowed $1.049 billion, which represented 24.2% of the total of mortgage money advanced - a new high water mark in terms of overall share of the mortgage money taken by the FHBs in a month.

And despite the overall amount of mortgage money in April 2023 being down some 23.6% compared with April 2022, the amount borrowed by by FHBs fell only slightly from $1.058 billion in April 2022.

I honestly make no judgement about whether it is a good thing or bad thing that first time buyers are continuing to get into the market at the moment - but they are certainly showing resilience.

While the RBNZ is now suggesting that the overall decline in house prices won't be as much as it earlier thought, the latest monthly mortgage figures show that activity has most certainly continued to decline.

The RBNZ says in its summary of key points accompanying the latest figures that on a seasonally-adjusted basis the April mortgage figures were down 2.5% on those for March 2023, when the actual figure was $6.036 billion.

The figures of course are one thing, but as everybody will be aware, mortgage sizes got a lot bigger over the last few years - so it takes a lot fewer individual mortgages to make up a large number.

It is therefore instructive to look a the numbers of mortgages taken out each month.

In April 2023 there were 12,084 mortgages taken out, down from 13,939 in April 2022 and positively dwarfed by the 25,261 mortgages taken out in April 2021.

Interestingly, if we look at the figures for April 2017 - which as you would recall from further up the article is the second worst 'normal' April month in terms of the amount of mortgage money advanced, there were that month 20,731 mortgages taken out.

So, okay, April 2023 saw $4.33 billion of mortgages advanced, which was 5% less than the $4.558 billion advanced in April 2017.

However the number of mortgages - at 12,084 - was down a thumping 41.7% compared with the 20,731 mortgages taken out in April 2017.

Of course April has not been a month in isolation in terms of being very slow. Let's have a look at the first four months of the year and run some comparisons.

For the first four months of this year there was $16.977 billion advanced in mortgages. And, yep, that is the lowest figure the RBNZ data has recorded for the first four months of a year, with the next lowest being the first four months of 2017, with $18.455 billion advanced.

Even the pandemic-ruined April of 2020 didn't stop the first four months of that year seeing $19.223 billion being advanced.

And in that super-hot 2021 period, the first four months of that year saw a staggering $32.934 billion advanced.

What about mortgage numbers?

Well the first four months of this year have seen 48,889 mortgages taken out. It is comfortably the lowest figure for the first four months of a year and is down from 59,352 mortgages in the same period in 2022 and a thumping 99,581 mortgages in the first four months of 2021.

The highest figure recorded for the start of a year is 121,453 mortgages taken out in the first four months of 2016.

So, yeah, it's quiet out there at the moment. It's real quiet. But the FHBs appear to be enjoying the space they have been given.

89 Comments

Looking at mortgage data is ignoring a portion of buyers, the cash buyers which will only be seen in sales volumes when correlated with mortgage data. Surely there are people who have sold up at a good price for them, and waiting on buying when things drop further.

I think we are pretty much at the bottom. Things will coast along now until the election and begin to pickup again next year. If inflation keeps rising and the RBNZ refuses to raise rates then build costs will increase while mortgage rates could stay the same and you have another round of FOMO while the market is at the bottom. Honestly anything could happen on the world stage suddenly making NZ the go to country. People think house prices have fallen but not really, all that's happened is almost all the froth has come off that went on in the last 2 years. Anyone that bought before 2021 is still ahead in the game.

I think circa another 5% to fall. It’s not stacking up for investors, and although the figure for FHBs are comparatively not too bad, they aren’t great either. Retail Interest rates may not go up, but they won’t be going down either for a while.

I think too that there might have been a mini FOMO happening over the last 5-6 months for FHBs. I know quite a few who have bought, thinking that the market is low and won’t go much lower. Tolerate high interest rates and manage for a year or two, and then they should come down.

It’s only a theory with no evidence, but maybe a large chunk of the FHBs with the means to buy have bought in the last 6 months, and there will be a bit of a drop away.

Firstly, you are all liars, you would not call him names if you saw him in person, you would probably be too intimidated to even speak to him without the shield of anonymity that this forum provides.

Secondly, I just don't like bullies, calling others names behind anonymity without them being able to reply, is plain bullying.

I nailed him at a Robert Half dog and bone, he was still talking no house price drops 14 months ago.....you guys are average have you ever seen him in person? who cares he like TTP and HW2 and all the BS spruikers here have been wrong since Nov 21.... calling the bottom every month what are you going to try and say you called the bottom ... when it happens, i call BS u been called the bottom for 18 Months now...... none of you sold the top, amateurs

So, maybe 150,000 mortgages this year - if we extrapolate the 4-month to the year.

Average tenure of an owner is 7 years - so that indicates 1.05M households of the 1.9 might be moving during that time.

Numbers are half what they should be (though consistent with 50% of households renting). Except only 1/3 of households rent...

Market is definitely not healthy, and it's going to take a significant up-tick in sales before that happens. But with dropping equity and increasing interest rates, only a dwindling pool of buyers remain - if prices were static.

Which indicates prices will continue to drop.

Part of me thinks well done FHBs for buying and for having 20% less debt than those who purchased 1.5 years ago and having home ownership etc (all the good things of owning your own place).

The other part of me thinks, gee it is possible if you wait another 6-12 months you might have buyers remorse as I think it's more likely that we see more falls in prices than any other outcome (flat or rising market). Have been wrong before, although the data points have never looked like this before either (from macro to micro, from global to local).

Thing is, they may well have seen friends badly burned by this sort of thinking. I was trying (and failing) to buy a house in Feb/Mar 2020. Then Covid happened, and many, many people told be I'd had a lucky break in having offers declined early 2020, as the housing market was bound to crash (and in fact every expert economist, commentator, etc was predicting this), so I should wait 6 months or so. And we all know what happened then...

How many experts in the MSM came out and said during 2020-2021-2022 that now is not the time to buy as house will drop 20% once the reserve bank raises rates again? If there is anyone I would like to see that story. The big problem in NZ is we can't lock in the low rates for longer than 5 years, unlike the US who can lock them in for 30, so we are very exposed. In the US peopel who are on these low rates are unlikely to sell becuase they may have to refix at these higher rates.

Quite puzzled about how this can happen. Anyone shed any light on how these borrowers got into this situation?

A family who bought a house 3 months ago is already in cashflow stress?

Wouldn't lenders have applied mortgage stress test rates of about 8.6-9.0%% when assessing their loan serviceability?

"Most of the couple’s income goes towards the mortgage after buying their house for $805,000 three months ago."

“Even after working as an Uber driver for five days, I am short of $450 every week,” Sunny said.

"The Saharans said their mortgage is unaffordable ... their current interest rate of 6.7 per cent expires next year ..."

https://www.nzherald.co.nz/kahu/peak-ocr-pain-auckland-couple-working-f…

It seems that they fixed their mortgage interest rate at 6.7% for one year when they took out their mortgage.

So in theory, their debt payments haven't even changed from their first mortgage payment. Yet they are now in cashflow stress?

So in the 3 months period either:

1) their other living expenses have risen substantially - nappies, and other baby stuff, groceries, insurance ?

2) their incomes have fallen - perhaps the part time catering business or the Uber income?

and the April figures, with just $4.33 billion advanced, are among the worst recorded.

Is this bad as the word "worst" implies? Or are these simply the lowest?

Much talk of how the housing sector is an essentially non-productive contributor to the economy, so aren't the low figures for housing good?

Does the FHB stats include the parent buying an investment property themselves but recording it as thier child's first home?

FHB are just people who are listed on the mortgage or title transfer documents as buying their first home, but on a title this could be in a joint ownership with mum and dad where m&d own the property.90/10?

On a mortgage this could easily be a m&d purchase via a pay back arrangement with son or daughter?

If the title is compared to the mortgage that might be interesting reading.

My thoughts go out to the naive FHB's who, since Nov 21, have been out there buying. If they listened to TTP and HW2 for example, the former has been saying buy counter cyclical since Nov21, the latter - buy, no matter what's happening. No wonder they're confused watching as their equity evaporates.

Start lowballing at the start of 2024 people!

edit

Why not wait until the full effect of fixed interest rollovers and higher unemployment to to set in? I suggest buy when sentiment is at its worst. I think its a little premature in timing for a recovery to be imminent justifying a "buy now" recommendation.

Each to their own :)

If the residents of NZ want to encourage more residential ownership by residential owner occupiers then it comes down to government priorities and government policies.

Singapore focuses on encouraging resident owner occupiers and less on multiple owners, non resident owners with their tax policies.

1) Property taxes (which we call rates)

i) note that they differentiate between owner occupied and non owner occupied,

ii) and they are on progressive rates - the higher the inputed rent, the higher the rate to determine property taxes (which we call them rates in NZ)

https://www.gov.sg/article/property-tax-on-residential-property

https://www.iras.gov.sg/taxes/property-tax/property-owners/property-tax-rates

Imagine bringing in a progressive rate system in NZ to calculate rates.

2) Stamp duty is differentiated between

1) citizens vs residents vs non resident buyers

2) first, or any property beyond their first property

https://www.propertyguru.com.sg/mortgage/calculators/stamp-duty

https://twitter.com/GRomePow/status/1643083095376285698?s=20

FYI,

Census data shows that homeownership peaked in the 1990s at 74 percent and by 2018 had fallen to 65 percent of households, the lowest rate since 1951. However, homeownership rates appear to have been more stable between 2013 and 2018

https://www.stats.govt.nz/news/homeownership-rate-lowest-in-almost-70-y…

Post sharemarket crash where house prices were rock bottom, the majority of boomers having children or already had them, houses were on the market for years, and the average family could buy one at 3x a single income. Those who didn't play with shares could buy up and do up for a nice family home, then load up on property via equity to get us into the pickle we are in today. I remember my parents saying they bought the house I grew up in for $130k (1850's house that had been extended in 1915), which went for over $1m when sold, pre-COVID. Kauri flooring, Matai kitchen put in. They don't build them like they used to

Either way you look at it, some will overpay, some will underpay, and in the end we will have more young NZ'ers in homes, starting families to fund all of our retirement if we are lucky enough to get there. More happy families = better communities = better NZ socially and culturally no matter what part of Narnia Mr Orr takes us down the rabbit hole into.

Bit of lunchtime number crunching.

12,084 mortgages at $4.33b gives an average mortgage size of $358,325 for the month of April. But if you separate out the FHBs, there were 1,883 of them in April borrowing a total of $1.049b, for an average of $557,089 (546 of these, or about 29%, with less than 20% deposit).

At 6.52% over 30 years, the average FHB mortgage taken during April will be costing $42,348 per year in repayments.

The good news for those FHBs is that they bought at a lower price and at what Mr Orr alledgedly hinted is maybe close to or marginally at the top of the cycle (the possibly peak of the ocr for now).

If Orr is right and prices go up soon... then if those buyers can easily afford their mortgage at the current rate.. then they have done well as over time their mortgage repayments will simply fall as the economy bounces back, plus they have less principal to pay off than those who bought in the last few years

Personally i think they are crazy and should wait til post the election.. when rates will rise and the economy will bomb.. but hey ho.

On all the positive noise i would buy soon .. if interest rates fall next year and we have substantial immigration and less houses then therr would be a big boom in 24/25 that would offset the loss over the coming months.

However I dont believe it. I think in the main immigration isnt quality wealthy skilled people, i think interest rates will rise and the economy will worsen.

I dont see it as an issue as some aspects of the tech industry are booming here and overseas .. which suits me perfectly financially. I pick major falls in house prices whìch will thrn plateau to about 2026 and then a slow pick up ...as only a few will be ready to buy.

Nz has some pain to deal with for a while... downward cycle isnt done.

I really hope they will be ok, I’m not a financial analyst ( but I am an analyst), I have always thought that a home loan rate of 7% was the neutral/normal rate, not 5% and certainly never 2.5% ( my father used to tell us amazed listeners of stories of 3% home loans back in the 1960s). Interest rates hitting 7% would have usually triggered us to moving from a floating rate and fixing our mortgage ( floating rates used to be cheaper than fixed rates). It seems strange to me now that there is an idea of interest rates getting back to “normal”, meaning dropping back to around 5%. What do you financial folks think about what a “ normal” interest rate is.

I look overseas for what 'normal' is. (NZ's economy is seriously unbalanced - and full of sacred cows - mainly due to scared politicians and the unenlightened (Ignorant?) nature of the swing voter block.)

7% is way too high. Between 3% and 6% but with long durations at the lower end, say 4.5%

Massive swings - as we've seen recently - are good for no-one and actually seriously upset the economy and people's mental health. Economic growth thrives on predictability and slow'ish movements core measures like the OCR. NZ's housing market is not managed well with most politicians taking a hands-off approach and consequently there is little regulation and little protection. In this regard, NZ's housing market is even more lassaize fair than the US market! Now that's saying something!

Sure, because the more than one billion dollars the Govt has spent on emergency housing is money well spent. Pretty sure it would have been cheaper to just give landlords their "tax break". But yay for all the middle class yuppies who can afford to buy $800k houses while the rest of the renters rot in meth contaminated motels alongside gang members and paroled sex offenders.

"The cost of emergency motels has risen from just $6 million in the final quarter of 2017 to $19 million in 2018. That grew again to $48 million the next year and $82 million in 2020. Then, in the past three months of last year, costs rose to $109 million - an increase of about $27 million in just a year. Overall in 2021, the cost was in excess of $350 million."

https://www.nzherald.co.nz/nz/politics/govt-has-spent-1b-on-emergency-h…

Just an observation. There are fewer buyers in the market than 2021 …… full stop. This data shows that the proportion of FHB’s has grown. It’s more realistic to observe that there has been a flight of buyers from the market. Speculators and investors have left in much greater numbers than FHB. The small number of FHB buyers that are active now represent proportionately more as a result but in absolute terms not so much.

$50k/year is the repayments on a $610k mortgage @ current FHB interest rates.

And 50% of a couple without student loan payments each on $75k. That's before rates, the compulsory insurances, maintenance, etc -> then living costs on top of that.

It gets much worse if they have student loans or children. And you're talking a salary $20k higher than the national median (but just below Auckland's) for people who are probably younger, less experienced, and less well-paid. For a $670k house (or $110k below the current median - and well below most of what's available in Auckland, for example).

And I'm ignoring the up-to $10k/year extra tax they'll pay if their incomes are not balanced, either.

Likely to be a similar decision making framework used by most owner occupier buyers.

When house price risks are at high levels, that is how owner occupier buyers become collateral damage.

Similar outcomes in other countries - US in 2006, Ireland in 2006, Japan 1990's, etc.

In our antenatal group had a 44-yo neonatal nurse who was somewhat taken aback at all the precautions the midwifes were giving her - which was really weird given she was telling us what could go wrong with 40+ pregnancies.

We didn't let renting stop us having kids - they'll [hopefully] be out of home in my wife's mid-40s. But kids did stop us having flatmates ... probably hit our ability to save a bit too ... so there's a significant financial cost to recoup in the future somehow (maybe their taxes will pay for our super, perhaps? - who cares, they're amazing little people who don't worry about financial matters pretty much at all!).

Mortgage rollovers might smash the glass floor many are standing on...Many will be hoping for an election carrot...it could get messy ... I suspect theres more sag coming ...yesterdays OCR was a bump higher not lower and a few words but not a miracle... wages and inflation out of whack... infrastructure lacking... Health system under the pump (covid hasnt left the building its just not as broadcast as it used to be) weather patterns /winter ahead... Election pending... Is now the optimum time to buy a house? "Nice work chippy" ...'You cannot be serious'.....(McEnroe)

We welcome your comments below. If you are not already registered, please register to comment.

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.