Share

Subscribe

From climate change to land rights - the best stories, the biggest ideas, the arguments that matter.

COVID-19 fallout has left countless Cambodians struggling to repay microfinance loans and fearful of losing their land

From climate change to land rights - the best stories, the biggest ideas, the arguments that matter.

As dark clouds approached her village in northwestern Cambodia one afternoon in July, Set Sreylon prepared for the monsoon that threatened to flood her new family home.

While the rains were a concern, the 37-year-old feared a bigger threat to her property - the daily visits from debt collectors demanding repayments on her microfinance loan and ensuing credit she had taken out to keep up with the repayments.

With the coronavirus pandemic ending Sreylon and her husband's jobs in the tourism industry, the mother-of-two was at a loss as to how she would keep the lenders at bay, and clear a growing debt secured by the title to her family's land.

Her debt - originally a single loan from a microfinance institution (MFI) - had almost doubled in a year to $8,000 and was pursued by various loan sharks charging up to 40% interest.

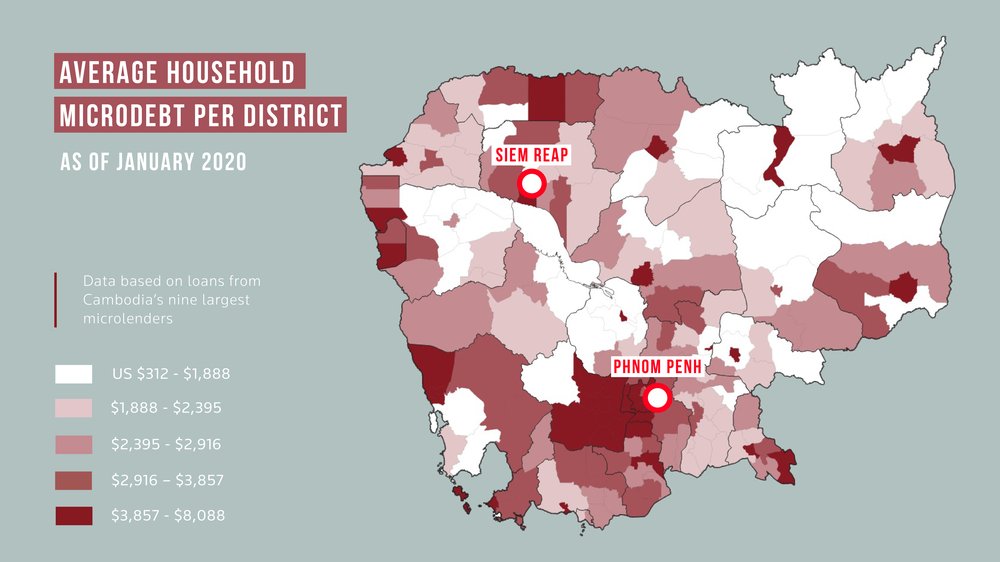

"You borrow from A to pay B, then you borrow from B to pay C," she said outside her home in Pouk district, a few miles from Cambodia's Angkor temples and the tourism hotspot of Siem Reap.

"What's the end result? You run out of letters and you have to sell your land," Sreylon told the Thomson Reuters Foundation.

Microfinance was pioneered in the 1970s by Nobel laureate Muhammad Yunus to give low interest credit to poor or rural people to set up businesses but the fast-growing sector has been invaded by predatory lenders who can strip people of everything.

Dozens of interviews with indebted villagers, charity staff, economists, lenders and officials revealed how the coronavirus fallout has compounded microfinance debts, with fears growing that countless Cambodians could end up destitute and homeless.

"The Cambodian microfinance sector was already headed for a meltdown," said Milford Bateman, a visiting professor of economics at Juraj Dobrila University of Pula in Croatia, and one of the world's leading academics and authors on the issue.

"COVID-19 has accelerated a slow-moving disaster for the poor as they are gradually stripped of their land," he added.

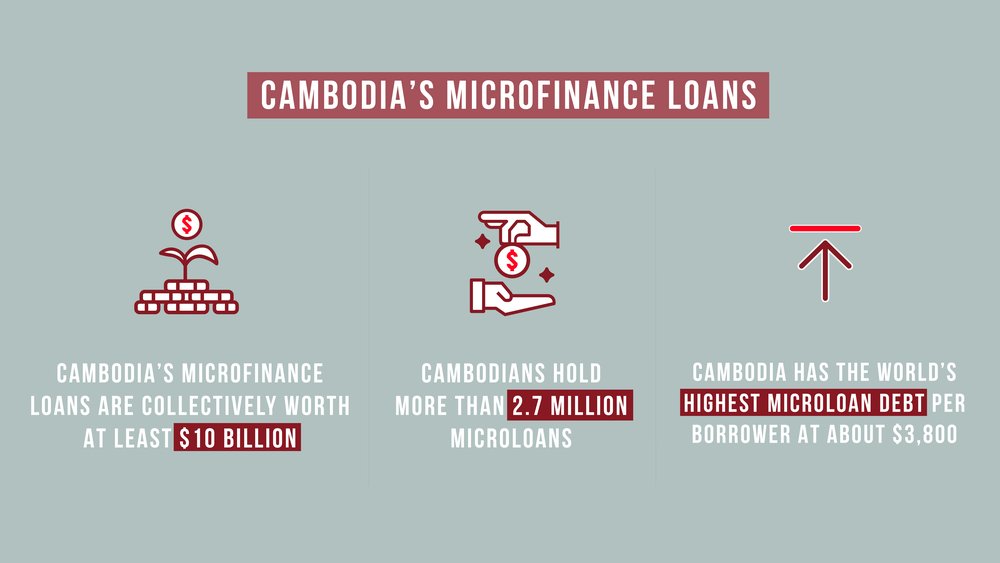

Sreylon is far from alone. She holds one of 2.7 million microloans in a country of 3.3 million households, where the average debt per borrower is the world's highest at $3,800 - more than twice Cambodia's gross domestic product per capita.

Since the Southeast Asian nation emerged from decades of war in the 1990s, microfinance has evolved into a $10 billion sector profiting international financial institutions.

The model has been credited with helping drag millions out of poverty by funding farming equipment or small businesses, but activists and academics said it has driven a rising number of borrowers to sell land, migrate or put their children to work.

About one in two Cambodians were landless in 2016, up from a third in 2009, the latest state data shows. It is unknown to what extent this rise was fuelled by the microfinance industry.

Organisations including the United Nations and the International Monetary Fund have in recent years warned that microfinance poses a risk to the Cambodian economy and ever-bigger loans would only push borrowers deeper into poverty.

The World Bank said in 2019 that "deteriorating lending practices and low financial literacy" in Cambodia had helped drive a tenfold increase in average loan size over five years.

High interest rates, the use of land titles as collateral, and pressure to repay have led to a "predatory form of lending", said human rights groups Licadho and Sahmakum Teang Tnaut (STT).

A spokesman for the finance ministry said Cambodia had a contingency plan for a potential microfinance crash, but did not give details and referred further questions to the central bank.

The central bank said it was working to crack down on informal lenders while also running numerous campaigns to boost people's financial literacy.

"Education is the most sustainable and impactful solution, but takes time to bear fruits," said Chea Serey, the National Bank of Cambodia's director general.

She also urged caution over recent reports about more borrowers falling further into debt.

"As policymakers, we need to be cautious of 'studies' and 'research' that could lead to misleading conclusions," she told the Thomson Reuters Foundation by email.

The chairman of the Cambodian Microfinance Association (CMA), Kea Borann, rejected claims of predatory lending and said that no land had been seized by any of its 90 members during the coronavirus pandemic.

The government in 2017 imposed an annual interest-rate cap of 18% on MFIs in a bid to help borrowers.

But activists said lenders responded by imposing new loan fees, covering their losses as debts continued to soar.

Borrowers who are unable to make repayments often double down on MFI loans, or turn to unregulated loan sharks who fly under the radar and offer instant cash at rates as high as 50%.

About 45% of Cambodians fell deeper into debt from January to April, while one in eight had to sell assets, from livestock and machinery to land, according to a survey of 54 village chiefs and 1,000 households by consultancy firm Angkor Research.

A third of new loans were taken to pay off existing loans or cover living costs, while the proportion of households that borrowed from informal lenders rose to 18% from 8.6% in that period, showed the data, which covered five of 25 provinces.

Dorm Diem, a village chief in Siem Reap whose residents have combined debt worth over $250,000, said this had led to community tensions and people threatening each other.

"Families are losing everything. Parents are being locked up in Thailand and children are left behind ... All villages around here are the same," he said.

"Microfinance has done more harm than good. The problem is only getting worse and I don't see how it can be solved."

One of the villagers, 38-year-old Pherl Pheap, said several of his neighbours had sold their homes this year to clear their debts and headed to Thailand, willing to risk possible arrest at closed borders in the hope of finding work.

Official data is lacking but media reports have detailed the arrests of hundreds of Cambodians trying to cross the border since it was closed in March. About 2 million are estimated to work in Thailand in sectors ranging from fishing to farming.

"It's a fire sale: sell your house, pay your debts, go to Thailand and start again," Pheap said. "I am one of the lucky ones. I managed to stay ahead of my debt, but there are others who have borrowed so much that they will never come back."

While Cambodia has recorded zero deaths and fewer than 300 cases of COVID-19, the pandemic has pummelled the tourism, construction and garment export industries that prop up its economy, wiping out hundreds of thousands of jobs.

At least 1.76 million jobs in the nation of about 16 million people are at risk due to COVID-19, while the poverty rate could double, to about one-in-four people, the World Bank said in May.

Cambodian human rights groups have this year called for a freeze on loan repayments due to the virus and for lenders to return more than one million land titles held as collateral.

Nine major lenders hold 90% of Cambodia's $10 billion in registered microdebt, including two former MFIs that have since become banks.

Yet the real figure is likely to be far higher as it does not include microloans given out by dozens of other banks or the growing number of informal lenders, activists and experts said.

CMA Chairman Borann said repayments had been frozen for 25,000 people among about 250,000 loans restructured to ease pressure on borrowers since March when the outbreak began.

He said reports of MFI staff pressuring borrowers or facilitating land sales were overblown. He pointed to various industry standards - which members are encouraged but not bound to follow - and a helpline set up to respond to complaints.

Criticism of the sector was unfair, he said, as it was based on outdated perceptions of a model that had evolved massively.

While some lenders still offer loans in the traditional development-focused mould - small, non-collateralised sums to kickstart informal businesses - others now approve credit for buying cars, building homes or investments, according to Borann.

"People say microfinance is responsible for lifting people out of poverty, but we are not responsible alone. They need to change the way they look at microfinance in Cambodia."

The government's messaging on microfinance has been mixed since the effects of the pandemic provoked widespread alarm.

Prime Minister Hun Sen in March called upon lenders to restructure loans for people affected by the virus, but later said banks should seize property from those who failed to repay.

Serey, of the National Bank of Cambodia, said the number of borrowers falling behind on repayments had fallen in July, after almost doubling to 2.72% from January to June.

But advocates said this did not account for a pattern of struggling borrowers taking new loans, often from unregulated loan sharks, to avoid defaulting on official ones where land is collateral.

Cambodian human rights groups have criticised a lack of government oversight and the role of Western development agencies and foreign investors, including European state development banks, for failing to address concerns.

From their roots in poverty alleviation, the nine major lenders are all now almost completely owned by international financial institutions and driven by profits, Licadho said.

"Development actors ... have failed to ensure programmes they fund do no harm, and Cambodian borrowers are currently paying the price for that failure," said Licadho director Naly Pilorge.

"Money that goes to further loans, without reforming the sector, will just compound the over-indebtedness crisis."

In June, the International Finance Corporation (IFC) - which focuses on the private sector in developing countries - approved $75 million in COVID-19 relief funds to be disbursed as loans by two Cambodian MFIs.

Another major MFI, LOLC Cambodia - formerly known as Thaneakea Phum or Village Bank - posted net profits exceeding $21 million in the first half of 2020, up from $17.6 million a year earlier.

In 2019, LOLC's parent company - The LOLC Group, Sri Lanka's most profitable listed business - agreed to sell its 70% share in Cambodia's biggest microlender, Prasac Microfinance Institution, for $603 million, marking a large profit.

"The main beneficiaries of microcredit in Cambodia are quite clear," said Bateman. "They are the CEOs and senior managers of the leading MFIs and their core shareholders and wealthy foreign investors, who ... have been making out like bandits."

LOLC and other shareholders in Cambodian MFIs - such as PhillipCapital Group, Shanghai Commercial & Savings Bank, Bank of Ayudhya, Netherlands Development Finance and European Investment Bank - largely did not reply to requests for comment.

A spokeswoman for German state-owned development bank KfW, Charis Pothig, said it planned to look into reports of improper MFI lending and forced land sales in Cambodia.

Loan officer Chea Chantha spends his days door-knocking, chasing repayments and convincing people to take out new loans from his employer, a registered lender. He said that clients defaulting and losing their land was a routine part of the job.

"When you get a loan, you know the conditions," said Chantha, explaining how he often read aloud the fine print of loan contracts to illiterate clients.

"If you sign, you agree. If you can't afford repayments, of course you will lose your property."

The CMA said about 60% of microloans in Cambodia are collateralised, the majority by land titles. Yet the association said its members rarely took land held as collateral from defaulting borrowers and had not done so at all since March.

Activists, however, detailed an off-the-books tactic whereby borrowers were persuaded to sell their land before it was taken.

Formal land seizures go through the courts so lenders tell clients to sell privately and use the money to avoid defaulting, shielding both parties from legal fees, said Lichado and STT.

This process, often accompanied by the promise of a new loan, allows the borrower to retain a good credit rating and saves the lender from bad publicity, found a 2019 report by the groups that anonymously quoted two MFI industry executives.

Local officials are often a party to loan contracts and lenders working together with authorities to increase pressure on borrowers is "widespread", according to the research.

Village chief Diem said brokering agreements between lenders and borrowers was now an unwanted but regular part of his role.

"First, it's $5,000, then $10,000, then $20,000 - then you say goodbye," he said, adding that about a third of 134 homes in his village were up for sale or had been sold to repay debts.

One of the villagers, 35-year-old Nan Sarin - who fell into debt with a $3,000 loan taken to hold a religious ceremony for her ailing parents - described having to sell off the family's farmland piece by piece as their debt diversified and soared.

"The stress of it all could kill me," she said, nursing one child as two others listened to her describe her financial woes.

"We don't see any progress in society from these loans - only misery and debt."

(Editing by Kieran Guilbert and Belinda Goldsmith)

From climate change to land rights - the best stories, the biggest ideas, the arguments that matter.

Just 1 email a week - every Monday with our best long reads of the past week!